Meaning of Opening Stock Opening stock is the inventory or stock of goods that are available at the beginning of the new accounting year carried down from the previous year's closing stock which is recorded in the books of accounts. In simple words, Opening stock is the goods/quantity/products thatRead more

Meaning of Opening Stock

Opening stock is the inventory or stock of goods that are available at the beginning of the new accounting year carried down from the previous year’s closing stock which is recorded in the books of accounts.

- In simple words, Opening stock is the goods/quantity/products that are held by a business at the beginning of a new accounting period and it is the closing stock of the preceding year carried down.

- Similarly, the closing stock is the number of unsold goods that remain with the business at the end of an accounting year and is further carried down to the next year as Opening Stock.

Formula

There are 3 main formulas used for Opening Stock’s calculation. They are-

- For manufacturing companies

Opening Stock = Raw Material Cost + Work in Progress + Finished Goods Cost

- When only Sales, GP, COGS, and Closing Stock are given

Opening Stock = Sales – Gross Profit – Cost of Goods Sold + Closing Stock

- You can use this one when only limited information is provided

Opening Stock = COGS + Closing Inventory – Purchases

Types of Opening Stock

There are three types of Opening Stock or we may also say that Opening Stock consists of these 3 elements. They are-

- Raw Materials- These are the unprocessed goods held by a business that is yet to be converted into finished goods.

- Work in Progress- These include the goods that are in process but not converted into finished goods.

- Finished Goods- These are the goods/products that have completed the manufacturing process but have not yet been sold.

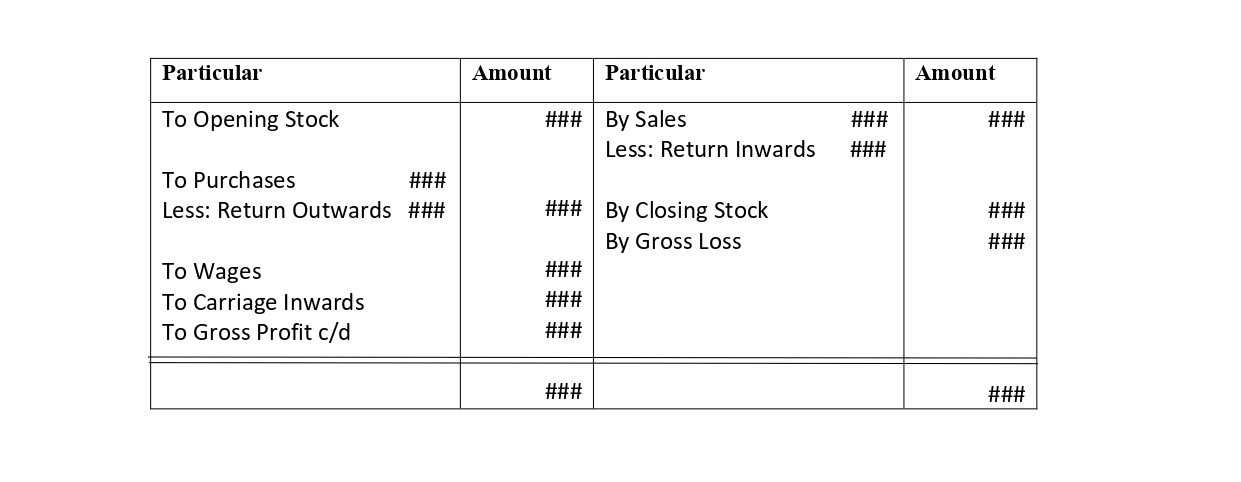

Opening Stock in Final Accounts

Opening stock is a part of the Trading Account while preparing the Final Accounts. And this is how it is posted in the Trading A/c.

Trading A/c (for the year ending…)

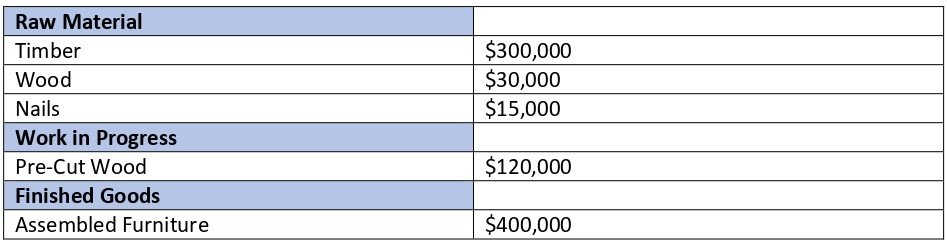

Example of Opening Stock

Example

IKEA, the biggest Furniture manufacturer collected this data on April 1, 2021,

Timber – $300,000

Wood – $30,000

Nails – $15,000

Pre-cut Wood – $120,000

Assembled Furniture – $400,000

Now, adding them (as said earlier, Opening stock is a combination of these three.)

Opening Stock (Raw Material + Work in Progress + Finished Goods) = $865,000

Therefore, that’s how one can calculate Opening Stock.

See less

A profit and loss account is a financial statement which shows the net profit or net loss of an enterprise for an accounting period. It reports all the indirect expenses and indirect income including gross profit or loss derived from trading accounts for an accounting period. When the total revenueRead more

A profit and loss account is a financial statement which shows the net profit or net loss of an enterprise for an accounting period. It reports all the indirect expenses and indirect income including gross profit or loss derived from trading accounts for an accounting period.

When the total revenue i.e. credit side of profit and loss a/c is more than the total of expenses i.e. the debit side of profit and loss a/c, it results in net profit whereas when the total revenue is less than the total of expenses, it results in a net loss.

The debit balance of the profit and loss account is the net loss incurred during the accounting period by an enterprise. It is transferred to a capital account thereby reducing the capital or can be shown as a debit balance on the asset side.

Accounting entry for loss transferred is as follows :

Capital A/c …Dr.

To Profit & Loss A/c

(being net loss transferred to capital account)

Example

A Business has a total income of $50,000 in an accounting year and has expenses amounting to $60,000 in that particular year. The profit and loss account will show a net loss of $10,000 ($60,000-50,000). Net loss will be transferred to capital A/c. Capital of the business will be reduced by $10,000. This loss can also be shown on the asset side of the balance sheet.

Extract of a Profit and loss a/c showing net loss is as under:

Profit and loss A/c for the year ended …..

The debit balance for a non-corporate entity is shown as a reduction from the capital account

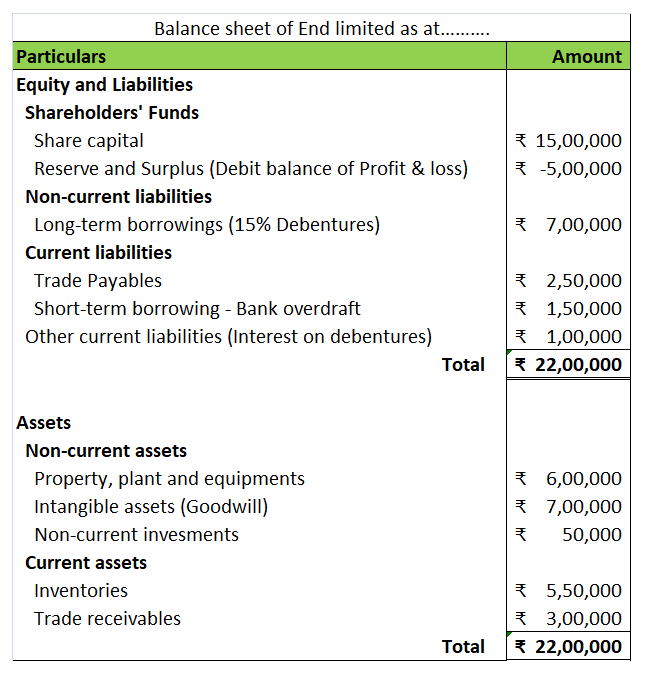

Extract of the Balance sheet showing the debit balance of Profit & Loss A/c is as under :

Balance Sheet as on…

Less: Profit & Loss A/c

While the Debit balance of profit and Loss A/c of a corporate entity is shown as a reduction in Reserves and surplus. If the business doesn’t have reserves then the debit balance is shown on the asset side.

Extract of the Balance sheet showing the debit balance of Profit & Loss A/c is as under :

Balance Sheet as on..

Less: Profit & Loss A/c

Conclusion: Debit balance of profit and loss a/c represents that expenses are more than the income of a business in an accounting period. Debit balance of profit and loss a/c indicates that company need to increase its income or cut down on unnecessary expenses.

The business needs to find out the reason of excessive expenses because accumulated losses are not good for the health of the company.

See less