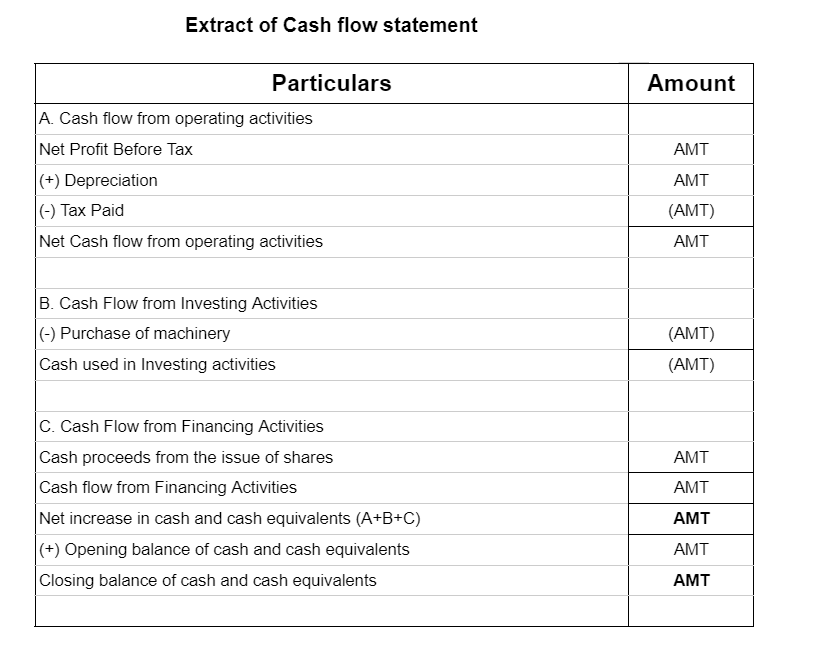

A cash flow statement presents the changes in the cash and cash equivalents of a business. It classifies the cash flow items into either operating, investing, or financing activities. Unlike a balance sheet that provides information about the company on a particular date, a cash flow statement proviRead more

A cash flow statement presents the changes in the cash and cash equivalents of a business. It classifies the cash flow items into either operating, investing, or financing activities. Unlike a balance sheet that provides information about the company on a particular date, a cash flow statement provides information about the flow of cash over a period of time.

OBJECTIVE

Information obtained through cash flow statements is aimed to assess the ability of a business to generate cash and at the same time, maintain liquidity. Therefore, important economic decisions can be made by evaluating these cash flow statements.

Cash Flow statements are categorized into

- Operating Activities: These activities refer to the main activities of the business during an accounting period. They involve revenue-generating activities. As per the indirect method, profit before tax is taken as the starting point and all non-cash expenses are added while non-cash incomes are deducted. Whereas in direct method, cash receipts and cash expenses are added and subtracted respectively. Eg: sale of goods.

- Investing Activities: These activities involve the sale and purchase of non-current assets and investments. Eg: cash payment for machinery.

- Financing Activities: These activities result in a change in capital or borrowings. Eg: cash proceeds from the issue of equity shares.

Importance of Cash Flow

A cash flow statement gives us knowledge about the liquidity and solvency of the company. These are necessary for the survival and expansion of the company. It also helps in predicting future cash flows by using information from previous cash flows. It also helps in comparison between companies which shows the actual cash profits.

Shareholders are the entities that hold some amount or number of shares of a company. As we know that ownership of a company is divided into its shares, a shareholder is actually a part-owner of a company. By entity, it means a shareholder may be: An individual Any other company Any other incorporatRead more

Shareholders are the entities that hold some amount or number of shares of a company. As we know that ownership of a company is divided into its shares, a shareholder is actually a part-owner of a company.

By entity, it means a shareholder may be:

The rights of shareholders depend on the type of shareholder one is.

Types of shareholders

1. Equity Shareholders: By the term ‘shareholders’ we usually mean equity shareholders. They are permanent in nature i.e. they are not repaid the money they have invested into the company until the company is liquidated or wound up. Equity shareholders have the following rights:

2. Preference Shareholders: They are shareholders who are given preference regarding:

Unlike equity shareholders, they are not of permanent nature. Preference shares are redeemable i.e. they are to be repaid after a period which cannot be more than 20 years from the date of allotment of such shares (as the Companies Act, 2013). Also, a company cannot issue irredeemable preference shares. The rights of preference shareholders are as follows:-

3. Differential Voting Rights Shareholders: These shareholders hold equity shares but with differential, right as to voting i.e. they may either have less voting rights or more voting right as compared to ordinary equity shares. Generally, DVR shares carry less voting power.

For example, a DVR shareholder gets 1 vote for 10 shares whereas an ordinary equity shareholder gets 10 votes for 10 shares i.e. one vote for every share. DVR shares issued to raise not only permanent capital but also prevent dilution of voting rights.

The rest of the right remains the same as the equity shareholders.

See less