When a manager provides services to a company, he is expected to receive some kind of compensation. This is given in the form of managerial remuneration. Section 197 of the Companies Act allows a maximum remuneration of 11% of the net profit of the company to the directors, managing directors and whRead more

When a manager provides services to a company, he is expected to receive some kind of compensation. This is given in the form of managerial remuneration. Section 197 of the Companies Act allows a maximum remuneration of 11% of the net profit of the company to the directors, managing directors and whole-time directors etc. This section is applicable for public companies and not private companies

Yes, a company can pay managerial remuneration in case of inadequacy of profits or losses, provided they follow the condition in Schedule V of the Companies Act 2013.

Conditions

In order to pay remuneration while the company is at a loss, it has to comply with the following:

- Pass a resolution at the board meeting

- The company has not defaulted in payments to any Banks, non-convertible debenture holders or any secured creditors. But in case of default, the company has obtained prior approval from such creditors or banks before obtaining approval from their general meeting.

- Ordinary resolution or special resolution (if the limit is exceeded)

The limit mentioned above refers to the maximum limit of Rs 60 lakhs when the effective capital is negative or less than Rs 5 Crore. Such remuneration can also only be paid if such a manager does not have any interest in the company and also possesses special knowledge and expertise along with a graduate-level qualification.

Effective capital is the aggregate of paid-up share capital, share premium, reserves and surplus, long term loans and deposits and after subtracting Investments, accumulated losses and preliminary expenses not written off.

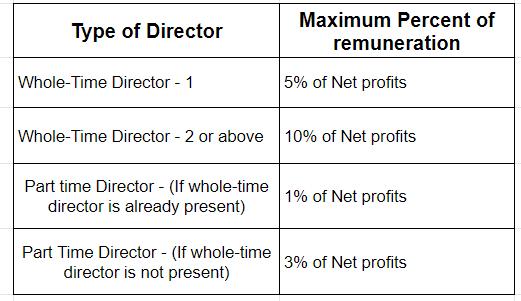

Percentage of Remuneration

When the Company earns adequate profits, they are allowed to provide remuneration up to a certain per cent. The percentage of remuneration depends on whether the directors are working whole-time or part-time according to the Companies Act.

As the name suggests, unrecorded liabilities means the liabilities that a firm fails to record in its book of accounts. Usually, a firm gets to know about its unrecorded liabilities when it is about to get dissolved. What happens is that upon hearing that a firm is going to dissolve in near future,Read more

As the name suggests, unrecorded liabilities means the liabilities that a firm fails to record in its book of accounts.

Usually, a firm gets to know about its unrecorded liabilities when it is about to get dissolved. What happens is that upon hearing that a firm is going to dissolve in near future, its creditors and lenders report to the firm about their dues.

At that time, a firm may get to know that it had failed to record some liabilities in its books and it has settled them now.

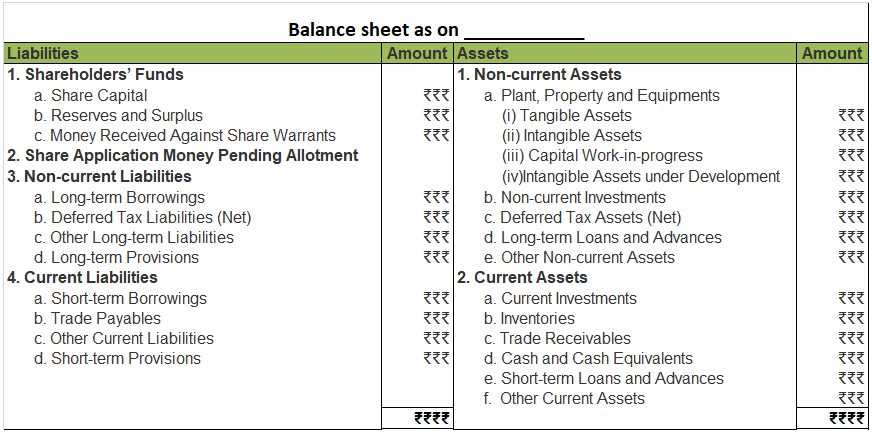

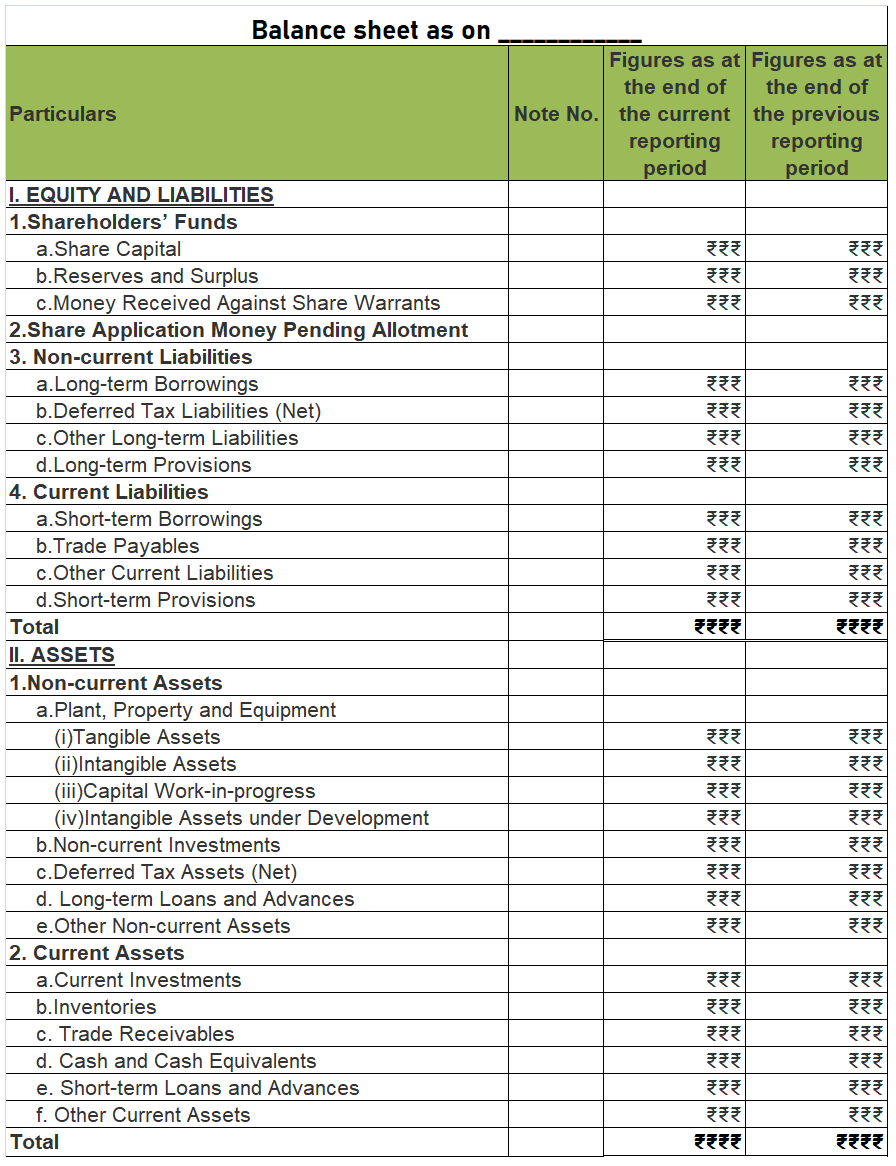

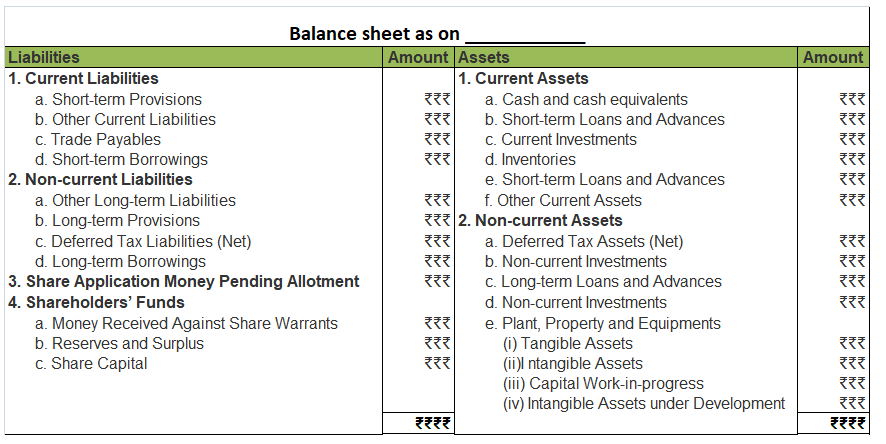

We know that when a partnership firm is dissolved, a realisation account is created to which all the assets and liabilities of the firm are transferred. Entries are as given below:

Realisation A/c Dr. ₹ Amt

To Assets A/c ₹ Amt

( Asset transferred to realisation account)

Liabilities A/c Dr. ₹ Amt

To Realisation A/c ₹ Amt

(Liabilities transferred to realisation account)

Hence, for transferring unrecorded liabilities, the procedure is the same for the recorded liabilities:

Unrecorded Liabilities A/c Dr. ₹ Amt

To Realisation A/c ₹ Amt

( Unrecorded liabilities transferred to realisation account)

Then to pay off the unrecorded liability the entry is:

Realisation A/c Dr. ₹ Amt

To Cash / Bank A/c ₹ Amt

(Unrecorded liabilities paid off)

That’s it, I hope I was able to make you understand.

See less