Yes, non-current assets are also known as fixed assets. These are long-term assets that are not intended for sale but are used by a company in its business operations. Examples of non-current assets include property, plant, and equipment, as well as intangible assets like patents and trademarks. TheRead more

Yes, non-current assets are also known as fixed assets. These are long-term assets that are not intended for sale but are used by a company in its business operations.

Examples of non-current assets include property, plant, and equipment, as well as intangible assets like patents and trademarks. These assets are recorded on a company’s balance sheet and are reported at their historical cost or at their fair market value, depending on the type of asset.

See less

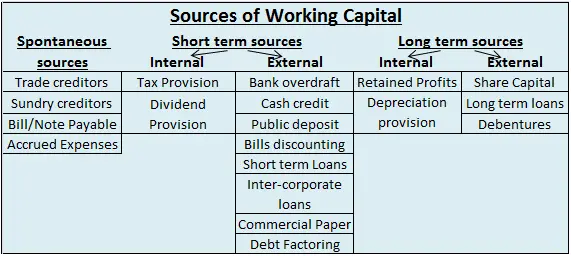

Fixed Working Capital Permanent working capital is also known as fixed working capital. Working capital is the excess of the current assets over the current liability and further, it is classified on the basis of periodicity, into two categories, permanent working capital, and variable working capitRead more

Fixed Working Capital

Permanent working capital is also known as fixed working capital.

Working capital is the excess of the current assets over the current liability and further, it is classified on the basis of periodicity, into two categories, permanent working capital, and variable working capital.

Permanent working capital means the part of working capital that is permanently locked up in current assets to carry business smoothly and effortlessly. Thus, it’s also known as fixed working capital.

The minimum amount of current assets which is required to conduct a business smoothly during the year is called permanent working capital. The amount of permanent working capital depends upon the nature, growth, and size of the business.

Fixed working capital can further be divided into two categories:

Whereas, on the other hand, variable working capital, also known as temporary working capital refers to the level of working capital that is temporary and keeps fluctuating.

See less