Yes, accounting is necessary even for not-for-profit organizations. NPOs or not-for-profit organizations are those that are created for the welfare of the society. They intend to advance some social cause. For example charities, orphanages etc Accounting for NPOs becomes necessary as the trustees ofRead more

Yes, accounting is necessary even for not-for-profit organizations.

NPOs or not-for-profit organizations are those that are created for the welfare of the society. They intend to advance some social cause. For example charities, orphanages etc

Accounting for NPOs becomes necessary as the trustees of these institutions are liable to their members, the donors and the government. They discharge this function with documenting activities of the institution.

What is a not-for-profit organization?

A not-for-profit organization is an entity that undertakes charitable activities. These institutions do not have earning profit as their primary motive. Their focus is on extending social welfare.

Every not-for-profit organization usually has a group of trustees that are responsible for handling all its operations. These trustees are accountable to the members of the NPO.

A not-for-profit organization usually relies on donations and grants as its primary source of revenue. They do not charge the stakeholders to whom they extend their services or goods.

What does accounting for Not-for-profit organizations entail

The professionals undertaking accounting of not-for-profit organizations must have a significant knowledge of statutory provisions and accounting principles. Here is a brief overview of what accounting for a not-for-profit organizations entails

- Ensuring that the institution fulfills all the legal compliances necessary for it to continue functioning as a NPO.

- Documenting all the activities of the institution and ensuring that the NPO has the necessary permits to carry out those activities.

- Accounting for all the revenue receipts and expenses of the institution. The professional must keep in mind that the interests of the members and other stakeholders are not being subjected to any prejudice.

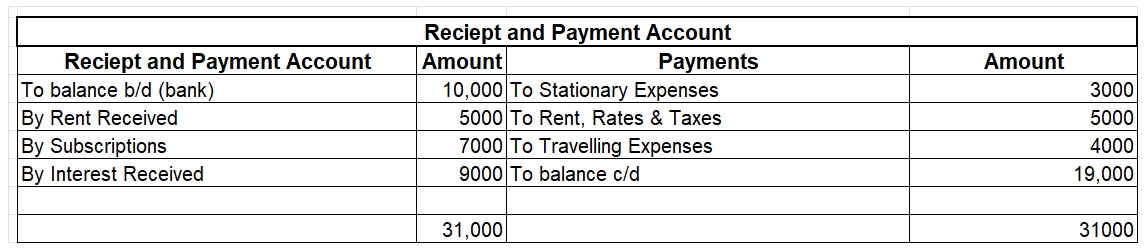

- In India, every NPO has to compulsorily prepare a receipt and payment account, income and expenditure account and a balance sheet. These have to be submitted to the Registrar of Societies before the due dates.

- Every professional undertaking the accounting of a not-for-profit organization must keep in mind that a single non-compliance or partial-compliance can result in the NPO losing out on its tax-exempt status.

- In the past there have been many instances when NPOs have been used for the purpose of money laundering or tax evasion.

- This has resulted in the government making the compliances for these institutions more stringent. The institutions are now required to be more transparent regarding their operations.

We can conclude that accounting is an indispensable requirements for not-for-profit organizations to be able to continue their operations and claim the statutory benefits that the government has extended to them.

See less

Bills Payable Book Bills payable book, also known as a B/P book is a subsidiary or secondary book of account in which transactions relating to bills of exchange are recorded. It includes the recording of bills that are payable by a business. In a business where the number of bills exchanging hands iRead more

Bills Payable Book

Bills payable book, also known as a B/P book is a subsidiary or secondary book of account in which transactions relating to bills of exchange are recorded. It includes the recording of bills that are payable by a business.

In a business where the number of bills exchanging hands is large in number, it is very useful, as it is tough to journalize all the bills drawn. A bills payable account generally has a credit balance as it is supposed to be paid at maturity and be a liability.

Format for B/P book

Bills Payable A/c

See less