Bills Payable Book Bills payable book, also known as a B/P book is a subsidiary or secondary book of account in which transactions relating to bills of exchange are recorded. It includes the recording of bills that are payable by a business. In a business where the number of bills exchanging hands iRead more

Bills Payable Book

Bills payable book, also known as a B/P book is a subsidiary or secondary book of account in which transactions relating to bills of exchange are recorded. It includes the recording of bills that are payable by a business.

In a business where the number of bills exchanging hands is large in number, it is very useful, as it is tough to journalize all the bills drawn. A bills payable account generally has a credit balance as it is supposed to be paid at maturity and be a liability.

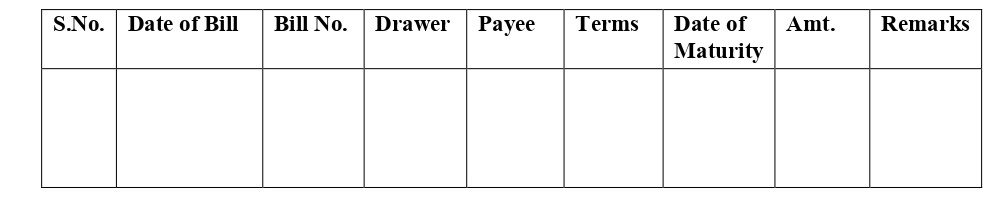

Format for B/P book

- The person, who draws the bill of exchange, is called a “drawer”.

- The customer, on whom it is drawn, is called a “drawee” or an “acceptor”.

Bills Payable A/c

Let’s understand what a cashbook is: A petty cash book is a cash book maintained to record petty expenses. By petty expenses, we mean small or minute expenses for which the payment is made in coins or a few notes like tea or coffee expense, bus or taxi fare, stationery expense etc. Such expenses areRead more

Let’s understand what a cashbook is:

The manner in which entries are made

When cash is given to the petty cashier, entry is made on the debit side and in the petty cashbook and credit entry in the general cashbook.

Entries for all the expenses are made on the credit side.

Generally, the petty cashbook is prepared as per the Imprest system. As per the Imprest system, the petty expenses for a period (month or week) are estimated and a fixed amount is given to the petty cashier to spend for that period.

At the end of the period, the petty cashier sends the details to the chief cashier and he is reimbursed the amount spent. In this way, the debit balance of the petty cashbook always remains the same.

Format and items which appear in the petty cashbook

The format of the petty cashbook depends upon the type of petty cash book is prepared and the items appearing in it are nothing but petty expenses. Let’s see an example:-

A business incurred the following petty expenses for the month of April:-

Now we will prepare two types of cashbooks:

Here, the Petty cash book is of the same format as the general cash book.

The cash allocated for petty expenses is recorded on the debit side of the petty cash book and on the credit side of the general cash book.

Here, there are separate amount columns for each type of expense. As the name suggests, this type of petty cashbook helps to analyse the petty cash spending on basis of the type of expense.

See less