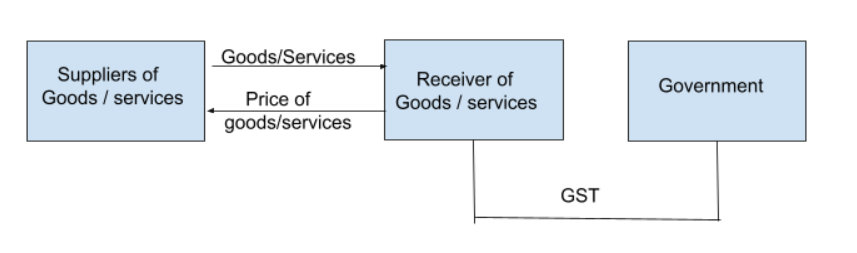

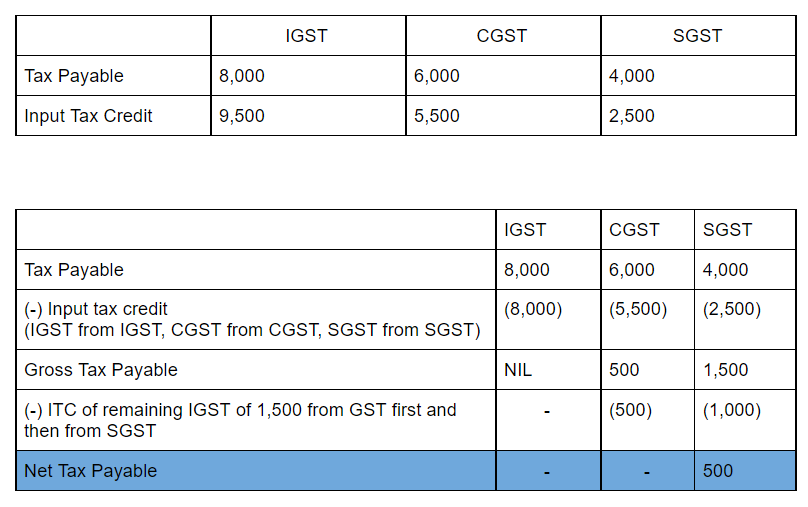

Goods and services tax (GST) is an indirect tax that was introduced in place of other indirect taxes like value-added tax, service tax, purchase tax, etc. It was introduced to ensure that only one tax would be applicable all over India. Reverse Charge is a mechanism where the liability to pay tax onRead more

Goods and services tax (GST) is an indirect tax that was introduced in place of other indirect taxes like value-added tax, service tax, purchase tax, etc. It was introduced to ensure that only one tax would be applicable all over India. Reverse Charge is a mechanism where the liability to pay tax on goods and services lies on the recipient instead of the supplier.

APPLICABILITY

Reverse charge is applicable when:

- It is specified by the CBIC for the supply of certain goods and services.

- Goods are supplied by an unregistered dealer to a registered dealer.

- There is a supply of services through an E-commerce operator.

TIME OF SUPPLY

As per reverse charge in the case of goods, the time of supply is the earliest of the three:

- Date of receipt of goods

- Date of payment

- The date is immediately after 30 days from the date of issue of invoice from the supplier.

For example, If goods were received by the supplier on 15th June, and the date of the invoice was on 3rd July but the date of entry in the books of the receiver was 25th June, then the time of supply of goods would be on 15th June.

As per reverse charge in the case of services, the time of supply is the earliest of the two:

- Date of payment.

- Date immediately after 60 days from the date of issue of invoice by the supplier.

For example, if the date of payment of services provided was on 16th July, and the date of issue of the invoice was on 15th May ( 60 days from 15th May is 14th July), then the time of supply of services would be 14th July.

See less

Introduction Income tax means the tax charged on the income of a person which the person has earned during a financial year. As per the Income-tax act, 1961, the income tax on income earned during a financial year is assessed in the following financial year and tax is to be paid on the assessed incoRead more

Introduction

Income tax means the tax charged on the income of a person which the person has earned during a financial year. As per the Income-tax act, 1961, the income tax on income earned during a financial year is assessed in the following financial year and tax is to be paid on the assessed income if payable.

The year in which the income is earned is called the Previous Year and the following year in which the previous year’s income is assessed is known as the Assessment Year

Steps involved in the computation of Income-tax of a person:

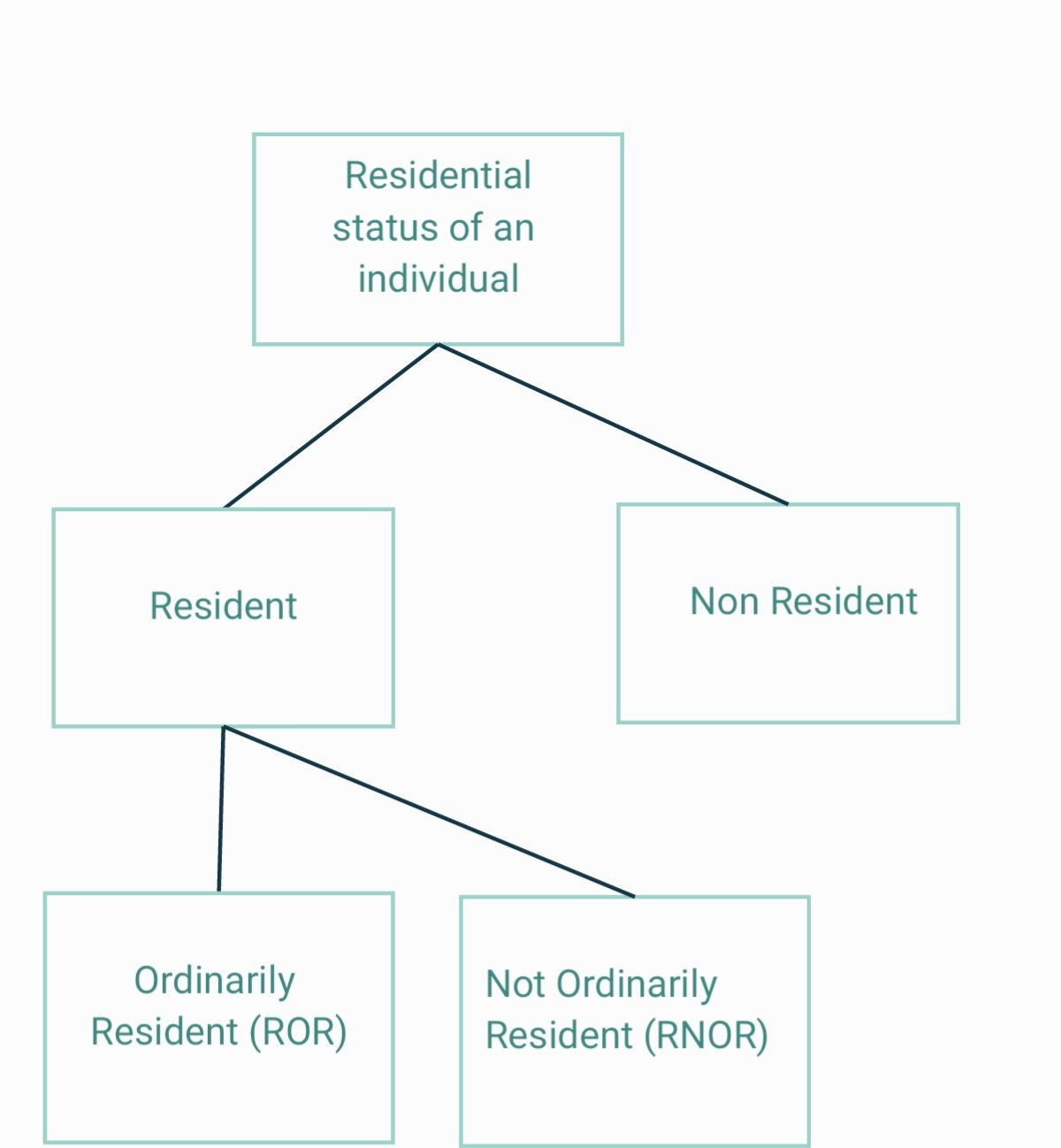

Determination of residential status of the person

The residential status of a person is of great significance for ascertaining the taxability of a person’s income as per the Income-tax act, 1961. As per the act, a person can fall into one of the following criteria:-

Classification and computation of income under the five heads of income

Now, a person’s income can be from various sources. As per section 14 of the Income-tax act, there are five main heads of income for computation of income tax:

Income under each head is to be computed as per provisions of the Income-tax Act, 1961.

Clubbing of income of spouse, minor child etc

Some individual taxpayers divert some portion of their income to their spouses and minor child in order to reduce their tax liability as the slab rate of income tax for individuals is progressive.

Such diverted income is to be clubbed with the income of the assessee as per the provisions of the Income-tax act.

Set-off and carry forward of losses

Losses suffered under the heads of the income like ‘Profit and Gains from Business and Profession’, ‘Income from House property’ can be set off against the income earned under other heads as per provision of the act.

If set off is not possible in the current assessment year then the loss can be carried forward to the next assessment year.

Computation of Gross Total Income

Gross Total Income is arrived at by computing the total of income under all five heads of income after giving necessary deductions as applicable under each head of income.

Deductions from Gross Total Income to arrive at Total Income

Income tax act, 1961 allows specific deduction from the Gross Total Income under sections 80C to 80U. These deductions are provided to encourage certain kinds of investments like life insurance premiums etc and provide relief on certain spending like medical expenses, interest expenses on home loans etc which leads to the overall welfare of the people.

After allowing the deductions from Gross Total Income, we arrive at Total Income.

Application of the rates of taxes on total income

Tax is calculated at a rate on the total income. The rate and calculation of income tax depend on the type of assessees.

Individuals and HUFs

For individuals who are below the age of 60 years and HUFs:

For individuals over 60 years and 80 years of age, the basic exemption limit is ₹3,00,000 and ₹5,00,000 respectively.

Also, as per section 115BAC, individuals and HUFs have the option to choose an alternative slab rate of tax as per which the income tax is charged at concessional rates. But, the various exemptions and deductions like housing rent allowance, leave travel concession, standard deduction on salary income cannot be availed. This slab rate system was introduced recently to reduce the complexity of filling IT returns by small taxpayers.

Rates of tax related to other types of assessees is not provided for sake of simplicity.

Advance tax and tax deducted at source

After calculating the tax on total income as per specified rates, the income tax amount is to be reduced by the advance tax and tax deducted at the source.

Tax payable/ Tax refundable

After performing all the steps above, we arrive at Income tax payable or tax refundable.

See less