Introduction Income tax means the tax charged on the income of a person which the person has earned during a financial year. As per the Income-tax act, 1961, the income tax on income earned during a financial year is assessed in the following financial year and tax is to be paid on the assessed incoRead more

Introduction

Income tax means the tax charged on the income of a person which the person has earned during a financial year. As per the Income-tax act, 1961, the income tax on income earned during a financial year is assessed in the following financial year and tax is to be paid on the assessed income if payable.

The year in which the income is earned is called the Previous Year and the following year in which the previous year’s income is assessed is known as the Assessment Year

Steps involved in the computation of Income-tax of a person:

- Determination of residential status of the person

- Classification and computation of income under the five heads of income

- Clubbing of income of spouse, minor child etc

- Set-off or carry forward of losses

- Computation of Gross Total Income

- Deductions from Gross Total Income to arrive at Total Income

- Application of the rates of taxes on total income

- Advance tax and tax deducted at source

- Arrival at Tax payable/ Tax refundable

- Determination of residential status of the person

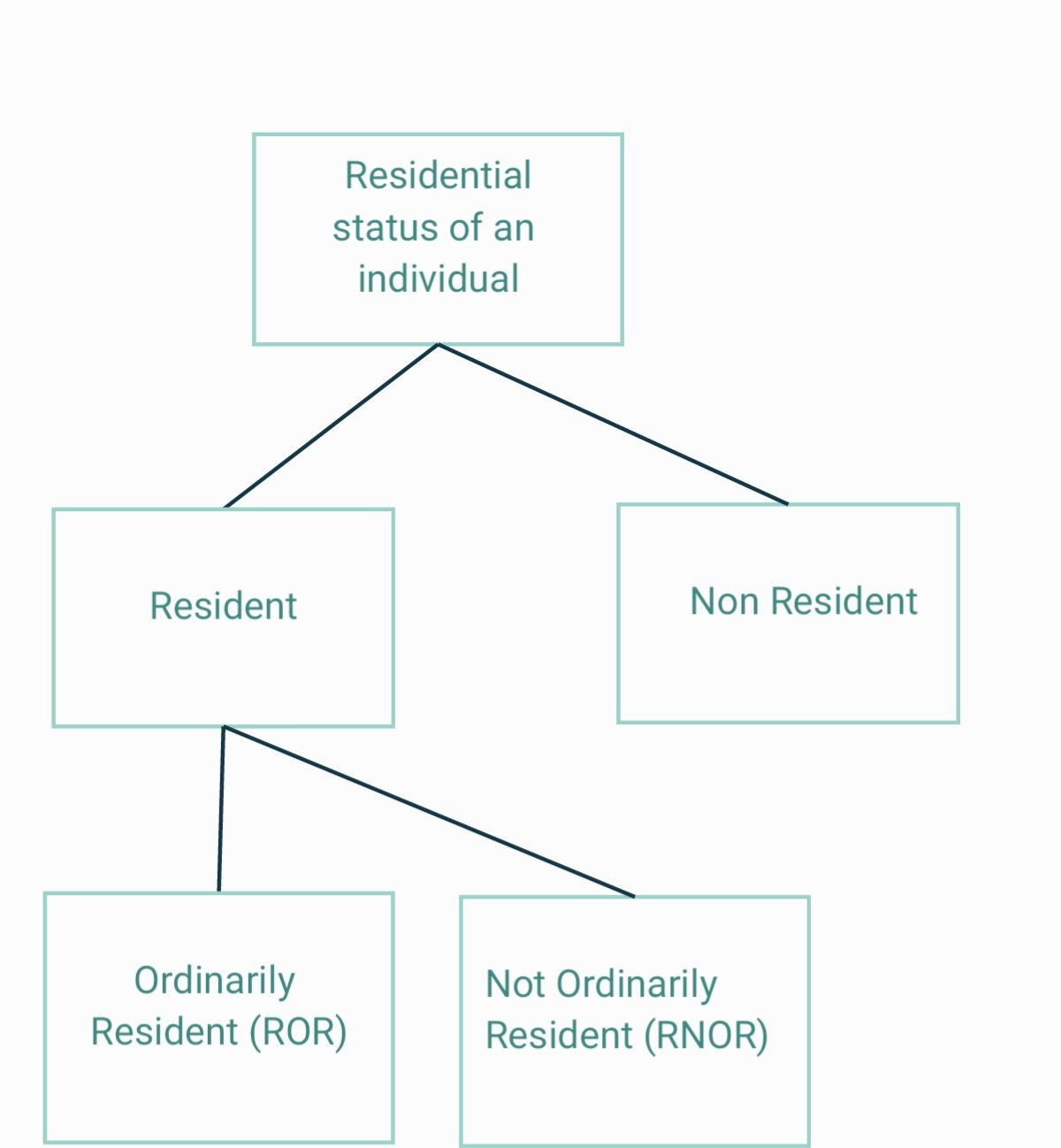

Determination of residential status of the person

The residential status of a person is of great significance for ascertaining the taxability of a person’s income as per the Income-tax act, 1961. As per the act, a person can fall into one of the following criteria:-

- Resident and Ordinarily Resident in India

- Resident but Not Ordinarily Resident in India

- Non-Resident

Classification and computation of income under the five heads of income

Now, a person’s income can be from various sources. As per section 14 of the Income-tax act, there are five main heads of income for computation of income tax:

- Income from Salary

- Income from House Property

- Profits and Gains from Business or Profession

- Capital Gains

- Income from other sources

Income under each head is to be computed as per provisions of the Income-tax Act, 1961.

Clubbing of income of spouse, minor child etc

Some individual taxpayers divert some portion of their income to their spouses and minor child in order to reduce their tax liability as the slab rate of income tax for individuals is progressive.

Such diverted income is to be clubbed with the income of the assessee as per the provisions of the Income-tax act.

Set-off and carry forward of losses

Losses suffered under the heads of the income like ‘Profit and Gains from Business and Profession’, ‘Income from House property’ can be set off against the income earned under other heads as per provision of the act.

If set off is not possible in the current assessment year then the loss can be carried forward to the next assessment year.

Computation of Gross Total Income

Gross Total Income is arrived at by computing the total of income under all five heads of income after giving necessary deductions as applicable under each head of income.

Deductions from Gross Total Income to arrive at Total Income

Income tax act, 1961 allows specific deduction from the Gross Total Income under sections 80C to 80U. These deductions are provided to encourage certain kinds of investments like life insurance premiums etc and provide relief on certain spending like medical expenses, interest expenses on home loans etc which leads to the overall welfare of the people.

After allowing the deductions from Gross Total Income, we arrive at Total Income.

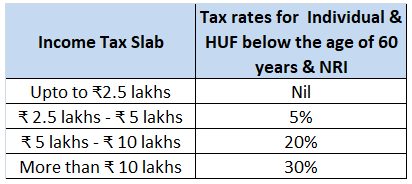

Application of the rates of taxes on total income

Tax is calculated at a rate on the total income. The rate and calculation of income tax depend on the type of assessees.

Individuals and HUFs

For individuals who are below the age of 60 years and HUFs:

For individuals over 60 years and 80 years of age, the basic exemption limit is ₹3,00,000 and ₹5,00,000 respectively.

Also, as per section 115BAC, individuals and HUFs have the option to choose an alternative slab rate of tax as per which the income tax is charged at concessional rates. But, the various exemptions and deductions like housing rent allowance, leave travel concession, standard deduction on salary income cannot be availed. This slab rate system was introduced recently to reduce the complexity of filling IT returns by small taxpayers.

Rates of tax related to other types of assessees is not provided for sake of simplicity.

Advance tax and tax deducted at source

After calculating the tax on total income as per specified rates, the income tax amount is to be reduced by the advance tax and tax deducted at the source.

Tax payable/ Tax refundable

After performing all the steps above, we arrive at Income tax payable or tax refundable.

See less

Brief Introduction Alternate Minimum Tax or AMT as the name suggests, is an alternate tax that an assessee has to pay, subject to certain conditions, instead of the income tax liability which is computed as per normal provisions of the Income-tax law. Alternate Minimum Tax is levied to impose higherRead more

Brief Introduction

Alternate Minimum Tax or AMT as the name suggests, is an alternate tax that an assessee has to pay, subject to certain conditions, instead of the income tax liability which is computed as per normal provisions of the Income-tax law.

Alternate Minimum Tax is levied to impose higher tax liability on non-corporate assessees who have claimed various profit-link deductions or investment-linked deductions in the relevant previous year.

My answer is based on the Indian Income law i.e. Income Tax Act, 1961.

The concept behind Alternate Minimum Tax

Let’s start our discussion with MAT i.e. Minimum Alternative Tax. It applies to corporate entities or companies.

Before MAT, it was seen that companies used to declare huge dividends to their shareholders. But when it came to filing income tax returns, they used to claim various profit linked and investment-linked deductions to report very low profits and even losses to arrive at negligible tax or nil tax whereas their financial statements would report huge profits.

It is true that the government provides such profit linked or investment linked deductions to encourage business and investments, but it also needs a sufficient and regular flow of revenue in the form of tax to fund its expenditure.

Hence, to prevent misuse of deductions to evade taxes by corporates, government introduce Minimum Alternate Tax to charge such assessees a minimum rate of tax.

Alternate Minimum Tax is the same as Minimum Alternate Tax in terms of concept. The provisions related to AMT are given under section 115JC of the Income Tax Act, 1961.

Scope of AMT as per section 115JC

Alternate Minimum Tax applies to all non-corporate assessees who claimed have claimed

However, there is a threshold limit for certain non-corporates.

By non-corporate assessees we mean:

AMT is applicable to all except

If their total adjusted income does not exceed Rs 20,00,000 in the previous year.

Therefore, AMT is applicable to all other non-corporate assessees like LLP, firms and cooperative societies irrespective of their total adjusted income.

Calculation of Alternate Minimum Tax

The rate of AMT is 18.5% of the adjusted total income. This adjusted total income and the AMT on it is calculated in the following manner:

The higher of the following becomes the tax liability of the assessee:

Numerical example

Mr X is a businessman who has earned the following income and expenditure in P.Y 2020-2021: (Amount in Rupees)

Income from manufacturing business 25,00,000

Interest on saving bank account 8,000

Dividend from ABC ltd 10,000

Insurance premium paid 1,00,000

Capital expenditure made as per section 35AD 5,00,000

Mr X is eligible to claim a profit linked deduction of Rs 6,00,000.

Also, the depreciation allowed (other than under 35AD) as per Income-tax Act,1961 amounts to Rs. 3,00,000.

Following is his computation of both AMT and Income tax liability as per normal provisions.

See less