Depreciation on Tools and Equipment Tools and Equipment are the instruments that are used for producing any product, machine, or service. Also, tools and equipment are a part of plants and machinery, making them a major fixed asset. Therefore, a certain percentage of depreciation is charged on ToolsRead more

Depreciation on Tools and Equipment

Tools and Equipment are the instruments that are used for producing any product, machine, or service. Also, tools and equipment are a part of plants and machinery, making them a major fixed asset. Therefore, a certain percentage of depreciation is charged on Tools and Equipment.

As we’re aware, depreciation refers to a process in which assets lose their value over time until it becomes obsolete or zero. It is chargeable on the fixed assets and it ultimately results in depreciation of the value of fixed assets except, land. The land is an exception in fixed assets as where all the fixed assets are depreciated, the land’s value is appreciated over time.

The rate of depreciation as per the Income Tax Act on tools and equipment (plant and machinery) is 15%.

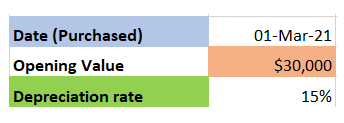

Example

Suppose given below are the details regarding the tools and equipment:

And, we’re required to calculate the value of the tools and equipment as on 1-Mar-22

In this, as we can see the business’ accounting period starts in March and ends in April. Therefore, we can easily deduct the depreciation amount and get the desired result.

Solution: Opening Value = $30,000

Depreciation = 15% of $30,000 = $4,500

Value of tools and equipment as on 1-Mar-22 = $30,000 – $4500 = $25,500

See less

Simply explaining the meaning of the useful life of an asset, it is nothing but the number of years the asset would remain in the business for purpose of revenue generation, making it more simple, the amount of time an asset is expected to be functional and fit for use. It is also called economic lRead more

Simply explaining the meaning of the useful life of an asset, it is nothing but the number of years the asset would remain in the business for purpose of revenue generation, making it more simple, the amount of time an asset is expected to be functional and fit for use. It is also called economic life or service life

It is a useful concept in accounting as it is used to work out depreciation. By knowing this useful life of an asset an entity can easily analyze how to allot the initial cost of an asset across the relevant accounting period rather than doing it unfairly manner.

How do we calculate the useful life of an asset?

The useful life of an asset is not an accounting policy, but an accounting estimate. calculating useful life is not an exact phenomenon but an estimate that is done because it directly impacts how much an asset is to expense every year.

Factors affecting “how long an asset is expected to be useful” depends on some stated points as below:

As per the companies act 2013, some of the useful life of assets are stated below

To know more about the different categories of assets you can follow the given link useful life of assets.

POINT TO BE NOTED:- There lies a huge difference in the useful life v/s the physical life of an asset. It is very important to note that amount of time an asset is used in a business is not always be same as an asset’s entire life span.

See less