A revaluation Account is an account created to record the changes in the value of assets and liabilities during: Change in profit sharing ratio Admission of a partner Retirement of a partner Death of a partner The realization Account is prepared to sell assets and pay liabilities in the event of theRead more

A revaluation Account is an account created to record the changes in the value of assets and liabilities during:

- Change in profit sharing ratio

- Admission of a partner

- Retirement of a partner

- Death of a partner

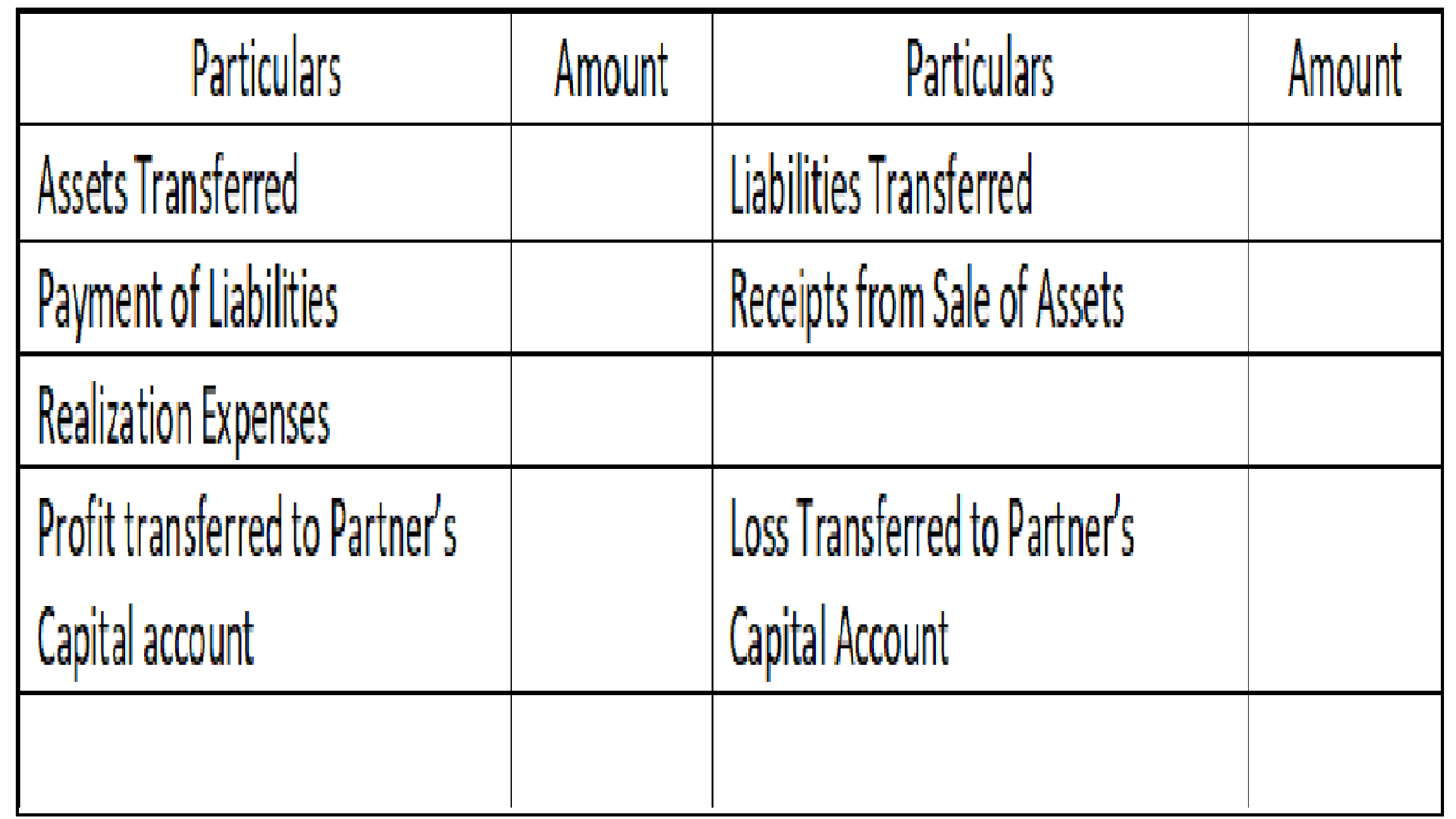

The realization Account is prepared to sell assets and pay liabilities in the event of the dissolution of the firm.

Revaluation Account is prepared for dissolution of the partnership while Realization Account is prepared for dissolution of the partnership firm.

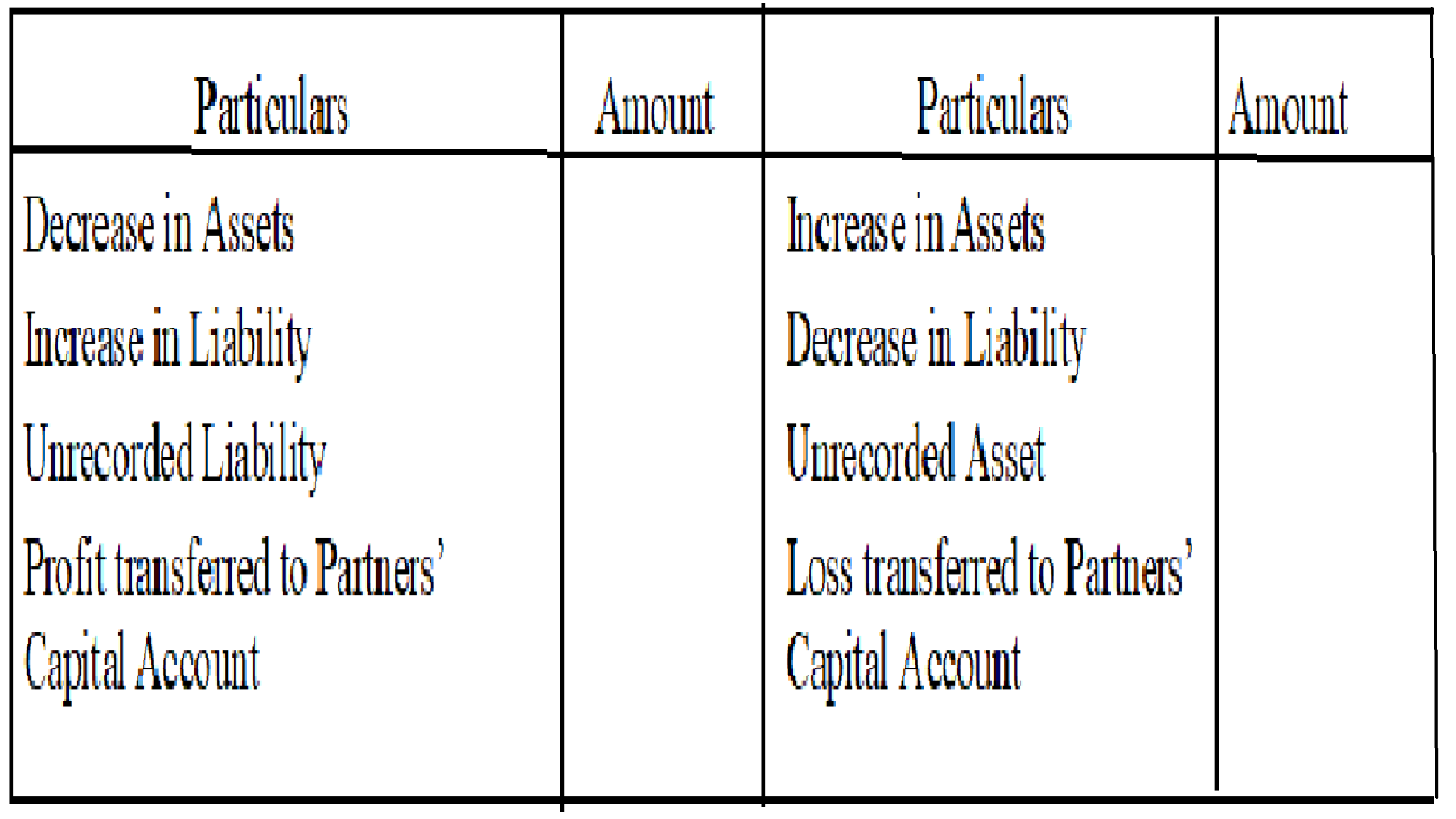

The increase or decrease in the value of assets and liabilities is transferred to the Realisation Account and the gain or loss thereof is transferred to the old partner’s capital account.

- A decrease in Assets and an Increase in Liabilities is debited since it is a loss for the firm and all the losses are debited.

- An increase in Assets and a Decrease in Liabilities is credited since it is gained for the firm and all the profits are credited.

Format of Revaluation Account will be:

Format of Realization Account will be:

The difference between Realisation and Revaluation Account is:

| Revaluation Account | Realization Account |

| Prepared to record changes in assets and liabilities | Prepared to record sale of assets and payment of liabilities |

| Prepared at the time of dissolution of the partnership | Prepared at the time of dissolution of partnership firm |

| Assets and liabilities still exist in the books only their values change | Assets and liabilities do not exist in the books of the firm |

| This account contains only those assets and liabilities that are to be revalued. | This account contains all the assets and liabilities of the firm. |

| A revaluation Account can be prepared any number of times during the lifetime of the firm. | The realization Account is only made once during the dissolution of the firm. |

| The gain or loss during revaluation is transferred to the old partner’s capital accounts. | The gain or loss during realization is transferred to the capital account of all the partners. |

See less

Order of Liquidity Under this method, a company organizes current and fixed assets in the balance sheet in the order of liquidity and the degree of ease by which it is converts converted into cash.On the asset side, we will write most liquid assets at first i.e. cash in hand, cash at bank and so onRead more

Order of Liquidity

Under this method, a company organizes current and fixed assets in the balance sheet in the order of liquidity and the degree of ease by which it is converts converted into cash.On the asset side, we will write most liquid assets at first i.e. cash in hand, cash at bank and so on and further. In the end, we will write goodwill.

Liabilities are presented based on the order of urgency of payment. On the liabilities side, we start from short-term liabilities for example outstanding expenses, creditors and bill payable, and so on. In the end, we write capital adjusted with net profit and drawings if any.

This approach is generally used by sole traders and partnerships firms. The following is the format of Balance sheet in order of liquidity:

Order of Permanence

Under this method, while preparing a balance sheet by a company assets are listed according to their permanency. Permanent assets are shown at first and then less permanent assets are shown afterward. On the assets side of the balance sheet starts with more fixed and permanent assets i.e. it begins with goodwill, building, machinery, furniture, then investments and ends with cash in hand as the last item.

The fixed or long-term liabilities are shown first under the order of permanence method, and the current liabilities are listed afterward. On the liabilities side, we start from capital, Reserve and surplus, Long term loans and end with outstanding expenses.

The following is the format of the Balance sheet in order of permanence:

Such order or arrangement of balance sheet items are refer as ‘Marshalling of Balance Sheet’.

See less