Similarly, someone asked Are loose tools current assets

Similarly, someone asked Are loose tools current assets

See lessPlease briefly explain why you feel this question should be reported.

Please briefly explain why you feel this answer should be reported.

Please briefly explain why you feel this user should be reported.

Similarly, someone asked Are loose tools current assets

Similarly, someone asked Are loose tools current assets

See lessA Realisation account is prepared at the time of dissolution of the Partnership firm to ascertain profit or loss from the sale of assets and payment of liabilities of the firm. All assets that can be converted into cash (i.e. from which any value can be realised) and all external liabilities to be pRead more

A Realisation account is prepared at the time of dissolution of the Partnership firm to ascertain profit or loss from the sale of assets and payment of liabilities of the firm. All assets that can be converted into cash (i.e. from which any value can be realised) and all external liabilities to be paid are transferred to the Realisation A/c.

So, Cash and Bank (already in liquid form), fictitious assets (doesn’t have any value to be realised), Partner’s Loan (internal liability) and Undistributed profits (not something that can be realised) are not included in the Realisation account.

DISSOLUTION OF PARTNERSHIP FIRM

It means the firm closes down its business and comes to an end. Simply, it means the firm will cease to exist in the future. As the firm is closing down, its assets are sold, liabilities are paid off, and the remaining amount (if any) is distributed among the partners.

REALISATION ACCOUNT

This account is prepared only once, at the time of dissolution of the Partnership firm. It is opened to dispose of all the assets of the firm and make payments to all the external creditors of the firm.

It ascertains the profit earned or loss incurred on the realisation of assets and payment of liabilities.

1. ASSETS

CASH AND BANK BALANCES are not included in the Realisation account as the purpose of the Realisation account is to sell assets to realise cash, but cash and bank are already in liquid form and thus, not included.

These are directly used for the payment of liabilities and if there is any remaining amount, then that amount is distributed among the partners.

FICTITIOUS ASSETS are huge expenses or losses that are written off over the years by writing off a portion of it every year for the next few years like accumulated losses, balance of Advertisement expenses, Preliminary expenses, Loss on the issue of Debentures, etc. They don’t have any physical existence or realisable value.

Since nothing can be realised from these assets they are not included in the Realisation account. These are transferred to the Partner’s Capital A/c.

2. LIABILITIES

PARTNER’S LOAN refers to the loan given to the firm by any partner of the firm.

Suppose, there are three Partners A, B and C. ‘C’ gave the firm a loan of $5,000. This $5,000 will be recorded as a Partner’s Loan and not just as a normal loan taken from an external party.

Since, Partner’s Loans are the internal obligation of the firm, they are not included in the realisation account instead a separate account is prepared to settle Partner’s Loan after all external liabilities are settled.

So, we can say in the Realisation account only external liabilities are included and paid.

UNDISTRIBUTED PROFITS are the Profits that are not distributed among the Partners like General Reserve, Reserve Fund, and Credit balance of P&L A/c.

They are not included in the realisation account as they can’t be sold as an asset neither they are any liabilities that should be paid. Undistributed profits belong to the Partners of the firm and thus, are transferred to Partner’s capital A/c.

See lessUnrecorded Assets are the assets that are completely written off but still physically available in the company or assets that are not shown in the books of the company. Unrecorded assets are generally recorded or recognized at the event of admission, retirement, death of a partner when all the assetRead more

Unrecorded Assets are the assets that are completely written off but still physically available in the company or assets that are not shown in the books of the company.

Unrecorded assets are generally recorded or recognized at the event of admission, retirement, death of a partner when all the assets and liabilities are revalued or dissolution of the firm.

Since Accounting Standards require firms to record all the assets and liabilities in their books, it is therefore mandatory to record such unrecorded assets.

There can be two cases for treatment of such unrecorded assets:

| Unrecorded Asset A/c (Dr.) | Amt | |

| To Revaluation A/c | Amt |

The unrecorded asset is now debited since it has to be recorded in the books now and Revaluation Account is credited since it is again for the business which will eventually be transferred to Partners’ Capital Account.

| Cash A/c (Dr.) | Amt | |

| To Partners’ Capital A/c | Amt |

If a partner decides to take over an unrecorded asset then his account is credited with that amount and since cash paid by the partner comes into business Cash Account is debited.

| Cash/ A/c (Dr) | Amt | |

| To Realization A/c | Amt |

When an unrecorded asset is discovered during the dissolution of the firm, such an asset is sold directly to the outsider and as a result, cash A/c is debited since the cash is entering the business. The entry is made through the Revaluation A/c and it is hence credited.

Example:

At the time of revaluation, firms find a typewriter that has not been recorded in the books and is valued at Rs 10,000. The journal entry to record that typewriter will be:

| Typewriter A/c (Dr.) | 10,000 | |

| To Revaluation A/c | 10,000 |

See less

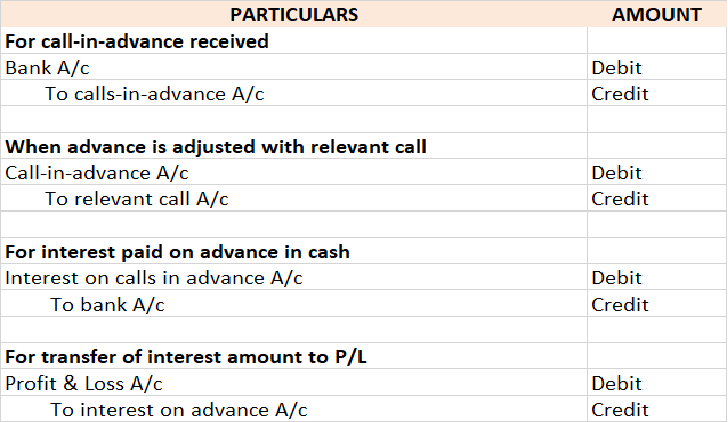

To begin with, lets us understand what the Companies Act 2013 tells about calls-in-advance, so basically as per section 50 of the companies act 2013 "A company may if so authorized by its articles, accepts from any members the whole or part of amount remaining unpaid on any share held by him, even iRead more

To begin with, lets us understand what the Companies Act 2013 tells about calls-in-advance, so basically as per section 50 of the companies act 2013 “A company may if so authorized by its articles, accepts from any members the whole or part of amount remaining unpaid on any share held by him, even if no amount has been called up”.

To be more precise whenever excess money is received by the company than, what has been called up is known as calls-in-advance.

Accounting Treatment

Well, it is to be noted that calls-in-advance is never a part of share capital. A company when authorized by its article can accept those advance amounts and directly credit the amount received to the calls-in-advance account.

As these advance amounts are a liability for the company these are shown under the head current liability of the balance sheet until calls are made and are paid to the shareholders.

Since this is the liability of the company, it is liable to pay the interest amount on such call money from the date of receipt until the payment is done to the shareholders. The rate of interest is mentioned in the articles of association. If the article is silent regarding the rate on which interest is paid then it is assumed to be @6%.

Accounting Entry

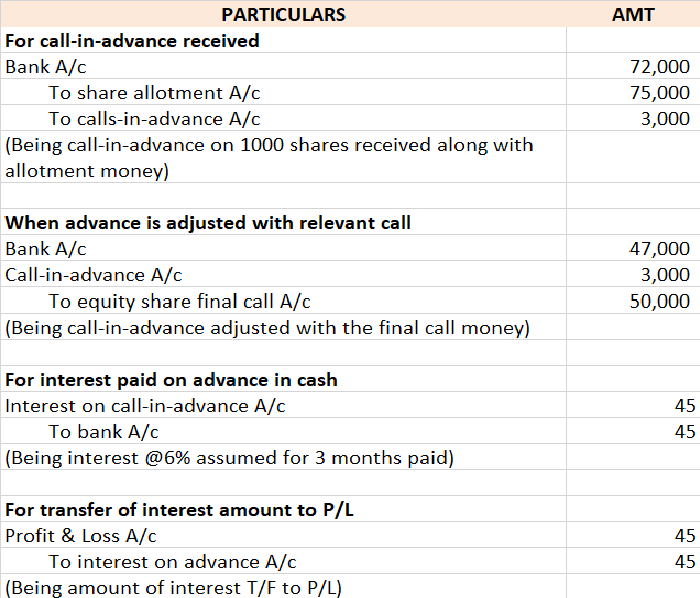

Bonnie let us understand the entries with help of an example

ADIDAS LTD issued 25,000 equity shares of Rs 10 each payable as follows:

ON APPLICATION Rs 5

ON ALLOTMENT Rs 3

ON FINAL CALL Rs 2

Application on 30,000 shares was received. excess money received on the application was refunded immediately. Mr. X who was allotted 1,000 shares paid the call money at the time of allotment and all amounts were duly received assume interest rate @6% for 3 months, so the relevant accounting entry goes as follows:

Important Points to be noted under calls-in-advance as per the companies act 2013

Introduction Furniture is treated as a fixed asset of an enterprise unless it deals in the manufacturing or the trade of furniture. As stock in trade, it will be treated as current assets. In both cases, they are real accounts. Hence, the golden rule of accounting will be the same. But, when it coRead more

Furniture is treated as a fixed asset of an enterprise unless it deals in the manufacturing or the trade of furniture. As stock in trade, it will be treated as current assets.

In both cases, they are real accounts. Hence, the golden rule of accounting will be the same.

But, when it comes to journal entries, Furniture A/c will appear only when it is treated as a fixed asset.

No journal entries are passed in the stock-in-trade account except for some balance transferring entries.

Taking furniture as a fixed asset, we can pass various entries related to it. Since furniture is an asset, any increase is debited and the decrease is credited.

Also, furniture is a real account which means the golden rule of accounting applicable is, “Debit what comes in and credit what goes out”.

Following are the basic entries related to furniture.

The most common entry related to furniture is the purchase of furniture:

| Furniture A/c Dr. | Amt | |

| To Cash / Bank A/c | Amt |

Here Furniture A/c is increased, hence debited.

Cash or Bank being reduced is credited.

| Cash / Bank A/c Dr. | Amt | |

| Profit and Loss A/c * Dr. | Amt | |

| To Furniture A/c | Amt | |

| To Profit and Loss A/c ** | Amt |

*In case of loss

**In case of profit

On the sale of furniture, its balance gets reduced, hence credited.

Cash or Bank is debited as cash comes in hand or into the bank.

Also, profit or loss may arise due to the difference in sale value and the carrying amount of the furniture A/c.

The difference is debited to Profit and Loss A/c in case of loss and credited in case of profit.

| Depreciation A/c Dr. | Amt | |

| To Furniture A/c | Amt |

Here, furniture is credited as it is decreased by the amount of depreciation.

Depreciation being a non-cash expense, is debited.

When furniture is stock of trade of a business, the journal entries will be like normal purchase and sales entries as below:

| Purchase A/c Dr. | Amt | |

| To Cash / Bank A/c | Amt |

| Cash / Bank A/c Dr. | Amt | |

| To Sales A/c | Amt |

There will be no furniture account.

See lessDefinition Journal Entry is an entry made in the journal is called journal entry. And the process of recording a transaction in a journal is called journalizing. Broadly journal entries are of two types : 1. Simple entry 2. Compound entry Otherwise, they are categorized into seven types which are asRead more

Journal Entry is an entry made in the journal is called journal entry. And the process of recording a transaction in a journal is called journalizing.

1. Simple entry

2. Compound entry

Otherwise, they are categorized into seven types which are as follows :

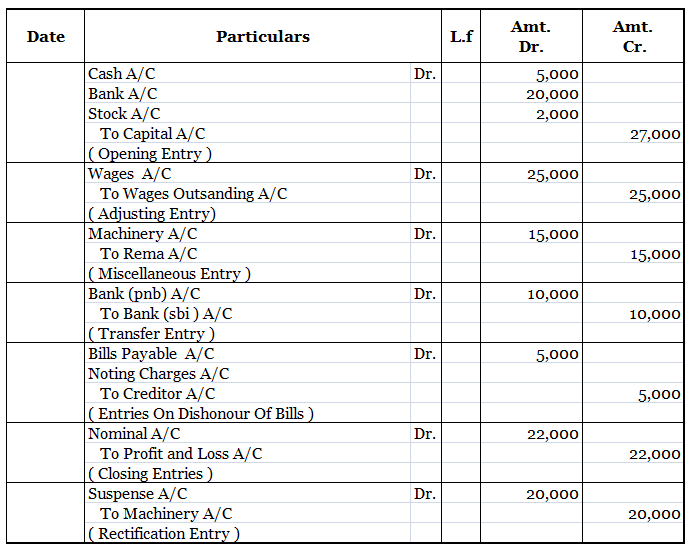

1. Opening entries

2. Closing entries

3. Rectification entries

4. Transfer entries

5. Adjusting entries

6. Entries on dishonor of bills

7. Miscellaneous entries

Now let me explain to you the above types of entries mentioned which are as follows ;

Simple entry

• Is a journal entry in which one account is debited and another account is credited with an equal amount.

• For example, the purchase of goods of Rs 5000 cash. It will affect two accounts,i.e., purchase A/C and cash A/C with the amount of Rs 5000.

Compound entry

• Is a journal entry in which one or more accounts are debited and/or one or more accounts credited or vice versa.

• For example the sale of goods to Sati for Rs 5000, Rs 2000 is received in cash, and the balance is to be received later.

• This transaction of the sale has an effect on three accounts i.e cash or bank A/C, Sati A/C, and sales A/C.

Opening entries

• Are defined as when books are started for the new year, the opening balance of assets and liabilities are journalized. For example bills payable, short-term loans, etc.

Closing entries

• At the end of the year, the profit and loss account has to be prepared. For this purpose, the nominal accounts are transferred to this account. This is done through journal entries called closing entries.

Rectification entries

• If an error has been committed, it is rectification through a journal entry.

Transfer entries

• If some amount is to be transferred from one account to another, the transfer will be made through a journal entry.

Adjusting entries

• At the end of the year, the number of expenses or income may have to be adjusted for amounts received in advance or for amounts not yet settled in cash.

• Such an adjustment is also made through journal entries. Usually, the entries pertain to the following :

Outstanding expenses,i.e., expenses incurred but not yet paid;

Prepared expenses,i.e., expenses paid in advance for some period in the future ;

Interest on capital is the interest proprietor’s investment in the business entity investment; and

Depreciation fall in the value of assets used on account of wear and tear. For all these, journal entries are necessary.

Entries on dishonor of bills

• If someone who accepts a promissory note ( or bill) is not able to pay in on the due date, a journal entry will be necessary to record the non–payment or dishonor.

Miscellaneous entries

The following entries will also require journalizing

• Credit purchase of things other than goods dealt in or materials required for the production of goods e.g. Credit purchase of furniture or machinery will be journalized.

• An allowance to be given to the customers or a charge to be made to them after the issue of the invoice.

• Receipt of promissory notes or issue to them if separate bills books have not been maintained.

• On an amount becoming irrecoverable, say, because, of the customer becoming insolvent.

• Effects of accidents such as loss of property by fire.

• Transfer of net profit to capital account.

Here are some examples of journal entries showing the above types :

There are three types of businesses that can be commenced, they are sole proprietorship, partnership, and joint-stock company. As we all know, to start any business a certain sum of money has to be invested by the owner which is known as the capital of the business in terms of accounting. In companiRead more

There are three types of businesses that can be commenced, they are sole proprietorship, partnership, and joint-stock company. As we all know, to start any business a certain sum of money has to be invested by the owner which is known as the capital of the business in terms of accounting.

In companies, commencement is a declaration issued by the company’s directors with the registrar stating that the subscribers of the company have paid the amount agreed. In a sole proprietorship, the business can be commenced with the introduction of any asset such as cash, stock, furniture, etc.

Journal entry

In the journal entry, “Started business with Cash”

As per the golden rules of accounting, the cash a/c is debited because we bring in cash to the business, and as the rule says “debit what comes in, credit what goes out.” Whereas the capital a/c is credited because “debit all expenses and losses, credit all incomes and gains”

As per modern rules of accounting, cash a/c is debited as cash is a current asset, and assets are debited when they increase. Whereas, on the increment on liabilities, they are credited, therefore, capital a/c is credited.

Therefore, the entry we’ll be passing is-

See less