I mean to ask is it real, nominal, or personal and why?

One of the main purposes of accounting is to provide financial data to its users so that decisions are taken at an appropriate time. These users of accounting information are broadly classified into (a) internal users and (b) external users. Since the question concentrates on internal users I’ll beRead more

One of the main purposes of accounting is to provide financial data to its users so that decisions are taken at an appropriate time. These users of accounting information are broadly classified into (a) internal users and (b) external users. Since the question concentrates on internal users I’ll be explaining internal users of accounting information in detail.

Internal users are people within an organization/business who need accounting information to make day-to-day decisions.

The various internal users of accounting information include:

- Owners/Promoters/Directors:

Owners are the people who contribute capital to the business and therefore they are interested to know the profit earned or loss incurred by the business as well as the safety of their capital. In the case of a Sole Proprietorship, the proprietor is the owner of the business. In the case of a Partnership, the partners are considered as the owners of the firm.

The use for them: To know how the business is doing financially, owners need to know the profit and loss reflected in the financial statements.

- Management:

Management is responsible for setting objectives, formulating plans, taking informed decisions, and ensuring that pre-planned objectives are met within the stipulated time period.

The use for them: To achieve objectives, management needs accounting information to make decisions related to determining the selling price, budgeting, cost control and reduction, investing in new projects, trend analysis, forecasting, etc.

- Employees/Workers:

Employees and workers are the ones who implement the plans set by the management. Their well-being is dependent on the profitability of the business.

The use for them: They are interested to check the financial statements so that they can get a better knowledge of the business. Some organizations also give their employees a share in their profits in the form of a bonus at the year-end. This also creates an interest in the employees to check the financial statements.

See less

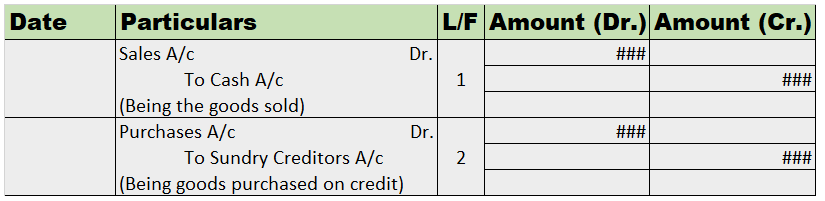

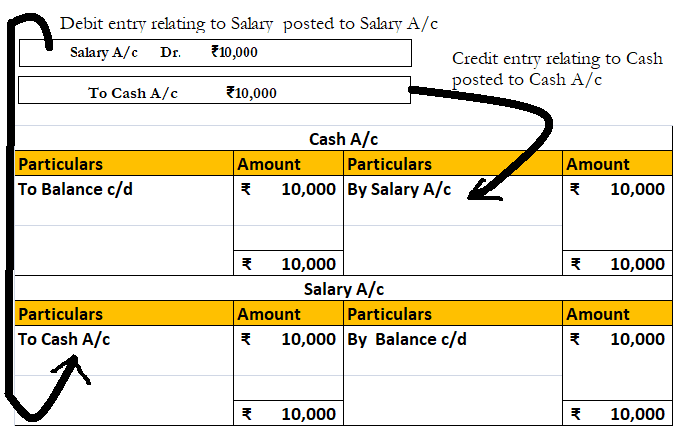

The correct option is option A. Journal is the book of original entry. It is from the journal, the postings in the ledgers are made. As it is the journal first to record the transactions, it is called the book of original entry. It is from the journal, the postings in the ledgers are made. Ledgers aRead more

The correct option is option A.

Journal is the book of original entry. It is from the journal, the postings in the ledgers are made. As it is the journal first to record the transactions, it is called the book of original entry.

It is from the journal, the postings in the ledgers are made. Ledgers are called the books of principal book of entry.

Option B Duplicate is wrong as there is no such thing as the book of duplicate entry in financial accounting. Journal entries are the first-hand record of business transactions. Hence, it cannot be the book of duplicate entries.

Option C Personal is wrong. This classification of ‘personal’ is a type of account as per traditional rules of accounting, not books of accounts

Option D Nominal is wrong. It is also a type of account as per the traditional rules of accounting.

See less