A. Trading Account B. Trial Balance C. Profit and Loss Statements D. Balance Sheet

Discount received is the reduction in the price of the goods and services which is received by the buyer from the seller. It is an income for the buyer and is credited to the discount received account and credited to the seller/supplier’s account. Journal entry for discount received as per modern ruRead more

Discount received is the reduction in the price of the goods and services which is received by the buyer from the seller. It is an income for the buyer and is credited to the discount received account and credited to the seller/supplier’s account.

Journal entry for discount received as per modern rules:

| Creditor’s A/c | Debit | Decrease in liability |

| To Cash A/c | Credit | Decrease in asset |

| To Discount Received A/c | Credit | Increase in income |

| (Being goods purchased and discount received) |

Discount allowed is the reduction in the price of the goods which is granted by the seller to the buyer on prompt payment of their account. It is an expense for the seller and is debited to the discount allowed account and credited to the buyer’s account.

Journal entry for discount allowed as per modern rules:

| Cash A/c | Debit | Increase in asset |

| Discount Allowed A/c | Debit | Increase in expense |

| To Debtor’s A/c | Credit | Decrease in asset |

| (Being goods sold and discount allowed) |

For example, A Ltd. offers a 10% discount to the customers who settle their debts within two weeks. Mr.B a customer purchased goods worth Rs.20,000.

According to modern rules, A Ltd will record this sale as:

| Particulars | Amt | Amt |

| Cash A/c Dr. | 8,000 | |

| Discount Allowed A/c Dr. | 2,000 | |

| To Mr.B’s A/c | 10,000 |

Mr.B will record this purchase as:

| Particulars | Amt | Amt |

| A Ltd A/c Dr. | 10,000 | |

| To Cash A/c | 8,000 | |

| To Discount Received A/c | 2,000 |

For a business, the discount received is an income, and the discount allowed is an expense. In the above example, A Ltd has granted a discount and B is the receiver of the discount. Hence, for A Ltd discount allowed is an expense and for B discount received is an income.

See less

The correct answer is Option C. The Profit and loss statement is also referred to as the statement of revenues and expenses. It is because the Profit and Loss statement reports all types of revenue that have been earned and all types of expenses that have been incurred during a particular period ofRead more

The correct answer is Option C.

The Profit and loss statement is also referred to as the statement of revenues and expenses. It is because the Profit and Loss statement reports all types of revenue that have been earned and all types of expenses that have been incurred during a particular period of time.

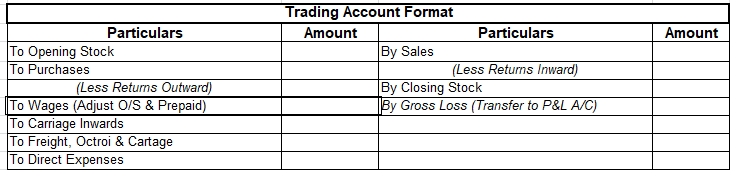

Option A Trading Account reports only the operating revenues and operating expenses.

Option B Trial Balance shows the balances of all the ledgers of a business and is prepared to check the arithmetical accuracy of the books of accounts.

Option D Balance sheet reports the balances of assets and liabilities of a business as at a particular date.

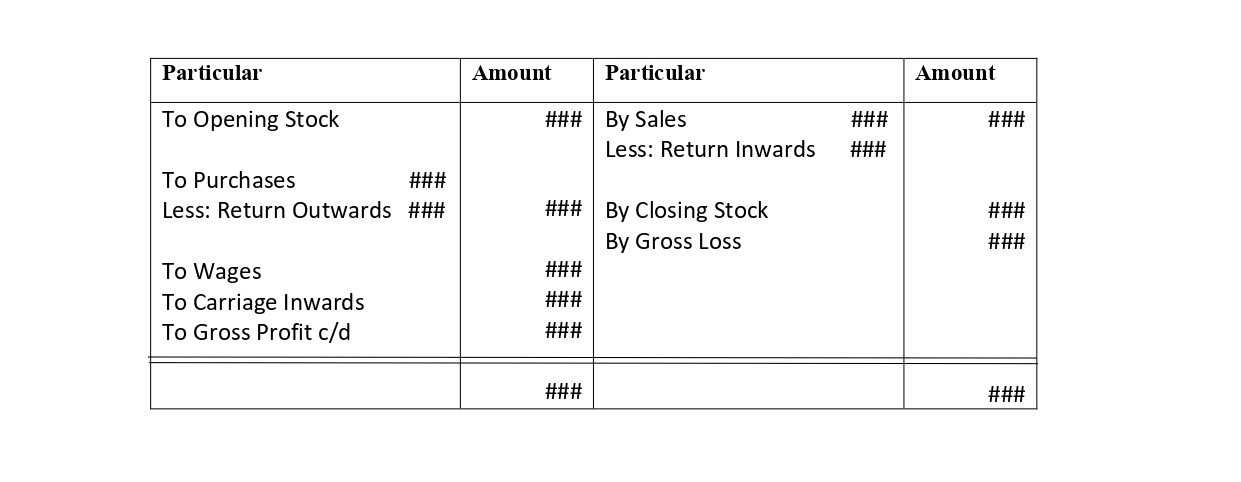

People often confuse the trading and the profit and loss statement to be the same. But they are different.

Trading Account is prepared with aim of arriving at operating profit or gross profit whereas the profit and loss statement is prepared to arrive at the net profit of a business and reports every revenue and expense whether operating or non operating in nature.

Operating revenue and operating expense are earned or incurred respectively are related to the chief business activities of a business.

Features of profit and loss statement:

- It is prepared to measure the net profit of a business hence its profitability.

- It is usually prepared for a period of one year but many companies do prepare quarterly statements to better judge their performance.

- It helps the management in decision making and the other stakeholders like shareholders, creditors to make informed decisions.

See less