Sundry debtor refers to either a person or an entity that owes money to the business. If someone buys some goods/services from the business and the payment is yet to be received, a group of such individuals or entities is called sundry debtors. Sundry debtors are also referred to as trade receivableRead more

Sundry debtor refers to either a person or an entity that owes money to the business. If someone buys some goods/services from the business and the payment is yet to be received, a group of such individuals or entities is called sundry debtors. Sundry debtors are also referred to as trade receivables or account receivables.

The term ‘Sundry’ means various or several, referring to a collection of miscellaneous items combined under one head. Sundry debtors typically arise from core business activities such as sales of goods or services. The business treats them as an asset.

Example

Suppose you run a business, ABC Ltd. Mr. Y bought goods from you on credit. Therefore, Mr. Y will be recorded as Debtor (current asset) in your books of accounts. Similarly, a collection of such debtors is viewed as sundry debtors from the business’ point of view.

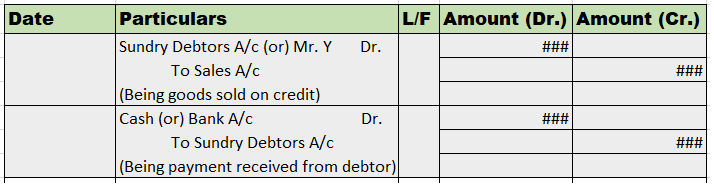

Journal Entry

Rules

As per the golden rules of accounting, we ‘debit the receiver and credit the receiver’. That’s how in this journal entry we’ll be debiting the sundry debtor’s account. Also, ‘debit what comes in and credit what goes out.’ That’s why sales a/c is credited and cash a/c is debited.

As per the modern rules of accounting, ‘debit the increase in asset and credit the decrease in asset’. That’s why we debit sundry debtors and cash a/c. And credit sales a/c when goods are sold and inventory decreases.

Why debtor is an asset?

As we know, a debtor refers to a person or entity who owes money to the business which means, the money is to be received by them in the future, making them an asset. On the other hand, creditors are a liability to the firm as we owe them money and it is to be paid by us in the near future, making it an obligation for the firm.

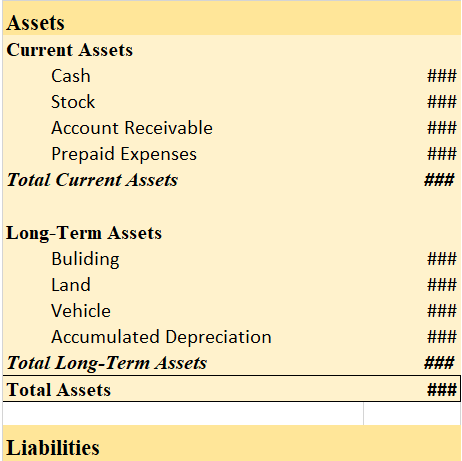

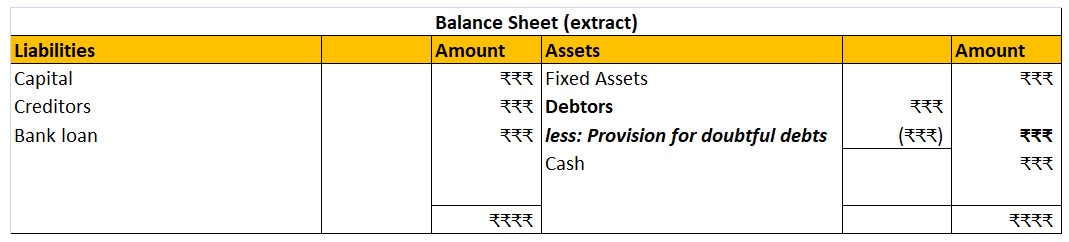

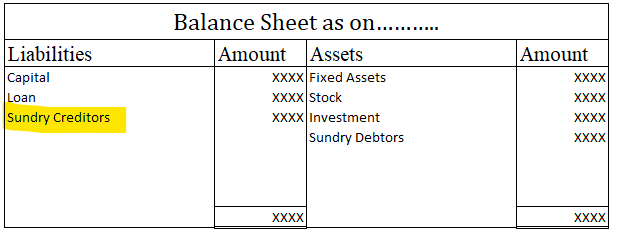

Sundry Debtors in Balance Sheet

Sundry debtors are shown under the current asset heading on the balance sheet. They are often referred to as account receivables.

Balance Sheet (for the year ending….)

Goodwill In Accounting Aspect, Goodwill refers to an Intangible asset that facilitates a company in making higher profits and is a result of a business’s consistent efforts over the past years which can be the business's prestige, reputation, good name, customer trust, quality service, etc. GoodwillRead more

Goodwill

In Accounting Aspect, Goodwill refers to an Intangible asset that facilitates a company in making higher profits and is a result of a business’s consistent efforts over the past years which can be the business’s prestige, reputation, good name, customer trust, quality service, etc.

Goodwill has no separate existence although the concept of goodwill comes when a company acquires another company with a willingness to pay a higher price over the fair market value of the company’s net asset in simple words the goodwill can be only realized while at the time of sale of a business.

The formula for Goodwill

Types of Goodwill

there are two types of goodwill.

1. Inherent Goodwill/Self-generated goodwill

Inherent goodwill is the internally generated goodwill that was created or generated by the business itself. it is generally generated from the good reputation of the business.

Inherent Goodwill or Self-generated goodwill is generally not shown in the books or never recognized in the books of Accounts and no journal entry for the inherent goodwill is passed.

2. Purchased Goodwill/Acquired Goodwill

At the time of acquisition of a business by another business, any amount paid over and above the net assets simply refers to the amount of Purchased Goodwill or Acquired goodwill.

A Journal entry is passed in the case of the Purchase of goodwill.

Type of Account

generally, Goodwill is considered and recorded as an Intangible asset(long-term asset) due to its physical absence like other long-term assets.

Modern rule of accounting:

as per the Modern rule of accounting, all Assets or all possessions of a business are comes under the head Asset accounts.

as Goodwill is treated as an Intangible asset it is an Asset Account.

Journal entry for purchase of goodwill as per Modern rule

Goodwill A/c Dr. – Amt

To Cash/Bank A/c – Amt

(The modern approach of accounting for the Asset account is: “Debit the increase in asset and Credit the decrease in the asset“)

The golden rule of accounting

As per the golden rule of accounting, all assets or possessions of a business other than those which are related to any person (debtor’s account) are considered Real accounts.

Such accounts don’t close by the year-end and are carried forward.

As Goodwill is an Intangible asset it is treated as a Real account as per the golden rule of accounting.

Journal entry for purchase of goodwill as per Golden rule

Goodwill A/c Dr. – Amt

To Cash/Bank A/c – Amt

(The golden rule of accounting for the Real account is: “Debit what comes in and Credit what Goes out“)

See less