(a) Potential investors (b) The owners or managers of the concern (c) Creditors and Lenders (d) Government

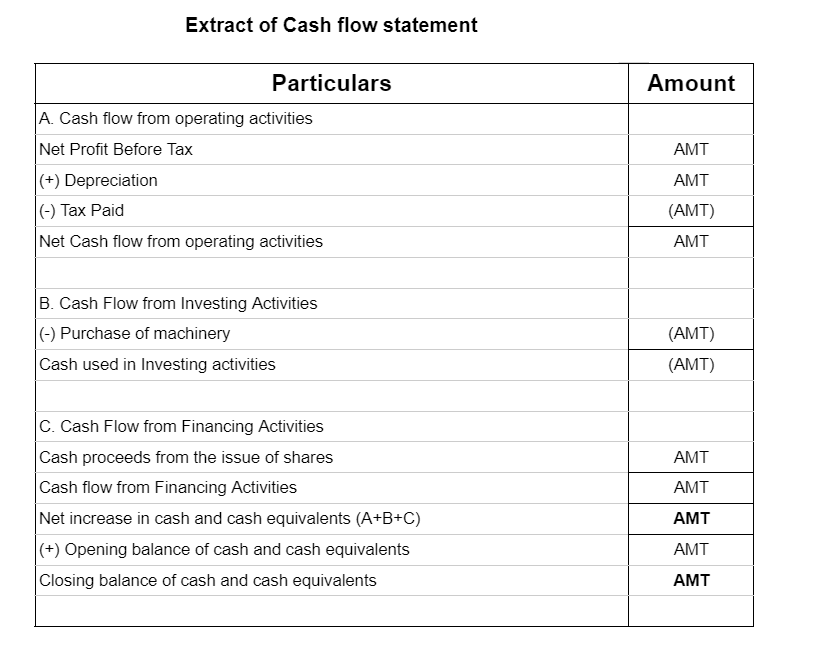

A cash flow statement presents the changes in the cash and cash equivalents of a business. It classifies the cash flow items into either operating, investing, or financing activities. Unlike a balance sheet that provides information about the company on a particular date, a cash flow statement proviRead more

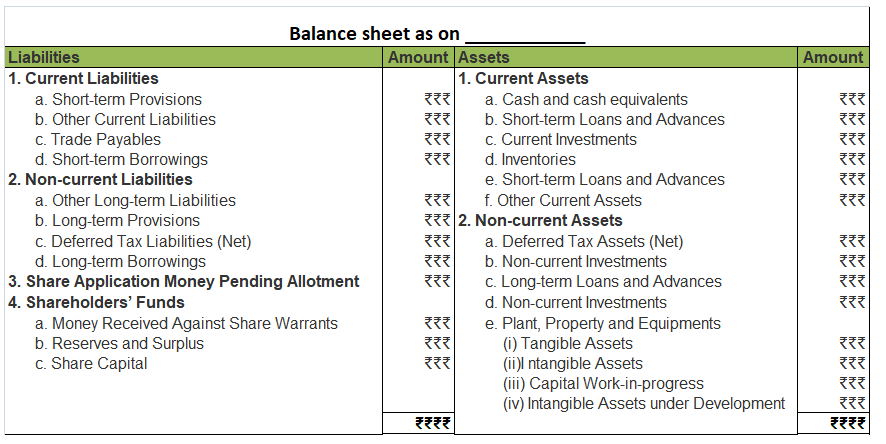

A cash flow statement presents the changes in the cash and cash equivalents of a business. It classifies the cash flow items into either operating, investing, or financing activities. Unlike a balance sheet that provides information about the company on a particular date, a cash flow statement provides information about the flow of cash over a period of time.

OBJECTIVE

Information obtained through cash flow statements is aimed to assess the ability of a business to generate cash and at the same time, maintain liquidity. Therefore, important economic decisions can be made by evaluating these cash flow statements.

Cash Flow statements are categorized into

- Operating Activities: These activities refer to the main activities of the business during an accounting period. They involve revenue-generating activities. As per the indirect method, profit before tax is taken as the starting point and all non-cash expenses are added while non-cash incomes are deducted. Whereas in direct method, cash receipts and cash expenses are added and subtracted respectively. Eg: sale of goods.

- Investing Activities: These activities involve the sale and purchase of non-current assets and investments. Eg: cash payment for machinery.

- Financing Activities: These activities result in a change in capital or borrowings. Eg: cash proceeds from the issue of equity shares.

Importance of Cash Flow

A cash flow statement gives us knowledge about the liquidity and solvency of the company. These are necessary for the survival and expansion of the company. It also helps in predicting future cash flows by using information from previous cash flows. It also helps in comparison between companies which shows the actual cash profits.

The correct option is (b) and (d) As the internal analysis is done for the internal assessment of the firm, only those persons can carry out the assessment who has access to the internal accounting records of a business firm. As the owners or managers are the members of the top-level management execRead more

The correct option is (b) and (d)

As the internal analysis is done for the internal assessment of the firm, only those persons can carry out the assessment who has access to the internal accounting records of a business firm. As the owners or managers are the members of the top-level management executives they can carry out the work of internal analysis. Also, the government agencies can carry out internal analysis as they have been given the statutory powers of doing such works.

To make it clear, let me explain a little about internal analysis-

To determine the profitability of various activities and operations or to know the performance of the business concern, the top-level executives along with the management accountant carry out an internal assessment of the financial statements within the concern, this process is known as internal analysis.

See less