Yes, a creditor is a liability. Creditors are treated as current liability. A creditor is a person who provides money or goods to a business and agrees to receive repayment of the loan or the payment of goods at a later date. The loan may be extended with or without interest. Creditors may be secureRead more

Yes, a creditor is a liability. Creditors are treated as current liability.

A creditor is a person who provides money or goods to a business and agrees to receive repayment of the loan or the payment of goods at a later date. The loan may be extended with or without interest.

Creditors may be secured creditors or unsecured creditors. In the case of secured creditors, some collateral is usually pledged to them. In the case of a default, they can sell or otherwise dispose of the collateral in any manner to recover the money due to them.

In the case of unsecured creditors, no collateral is pledged against the amount due to them. In the case of a default, they can approach a Court to enforce repayment but cannot sell any asset of the company by themselves.

Why are Creditors treated as a liability?

An asset is something from which the business is deriving or is likely to derive economic benefit in the future. The business has legal ownership of that asset which is legally enforceable in a court of law. For example, Plant and Machinery, accrued interest, building, etc

A liability is a legal obligation of the business. It may be in the form of outstanding payments or loans or the owner’s share of the company that the company has to pay them as and when demanded.

As the company has a legal obligation to pay money to the creditor, they are treated as a liability. Most creditors are to be repaid within 1 year and are hence classified as current assets.

Treatment and Importance of Creditors

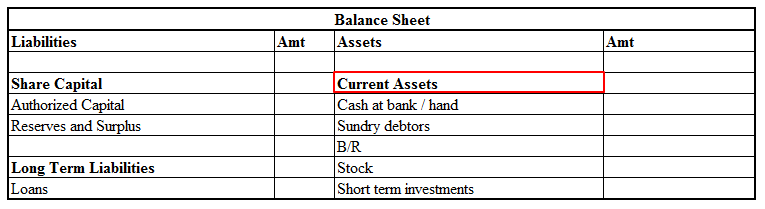

Creditors are mostly treated as current liabilities. They are shown under the head “current liabilities” of the balance sheet of a company.

The significance/importance of creditors is as follows:

- The amount due to creditors affects the current and acid test ratio of a company significantly.

- It affects the short-term cash requirements of a company.

- It affects the credit policy of the company. A company can extend longer credit periods to customers if it can avail longer credit periods from its suppliers.

- Having too many creditors or a large amount due to creditors can affect investor sentiment negatively regarding the business.

We can conclude that the creditor being a person to whom the business is legally liable to pay a certain sum of money after a certain period of time has to be classified as a liability.

Creditors play a major role in determining the success of a business. They act as a major constituent of the supply cycle of the business and affect the cash flows of the business. They are shown under the head “current liabilities” of the balance sheet of a company.

See less

Accrual Accrual expense means the transaction that takes place in a particular period must be accounted for in that period only irrespective of the fact when such amount has been paid. An accrual of the expenditure which is not paid will be listed in the books of accounts. These accruals can be furtRead more

Accrual

Accrual expense means the transaction that takes place in a particular period must be accounted for in that period only irrespective of the fact when such amount has been paid.

An accrual of the expenditure which is not paid will be listed in the books of accounts. These accruals can be further divided into two parts

Accrual Expense-

Accrual Expense means any transaction that takes place in a particular period but the amount for it will be paid on a later period.

For example- If rent of 10,000 for the month of March was paid in April month then this rent will be accounted for in the books in March

For example- Interest of 1,000 for the month of March of the loan amount of 10,000 paid in April then will be accounted for in the books in March

These are the following accrued expense

Accrual Revenue-

Accrual Revenue means any transaction that takes place in a particular period but the amount for it will be received in the later period.

For example- If interest of 10,000 on bonds for the period of March is received in April months then this amount will be accounted for in March. These are the following accrued revenue

For example- Rent of 10,000 for the month of March received in April month then this rent will be accounted for in the books in March

- Accrual Income- Acrrual expense means the amount for any income received on a later period than the period when it pertains to be received

- Accrual Rent– Accrual rent means the amount for using the land of the entity by the other party is received at a later period than the period when it is put into use.

- Accrued Interest– Accrued interest means the amount of interest received on a later period than the period when it pertains to receive

See less