Current Assets & Examples Current Assets are those assets that are bought by the company for a short duration and are expected to be converted into cash, consumed, or written off within one accounting year. They are also called short-term assets. These short-term assets are typically called currRead more

Current Assets & Examples

Current Assets are those assets that are bought by the company for a short duration and are expected to be converted into cash, consumed, or written off within one accounting year. They are also called short-term assets.

These short-term assets are typically called current assets by the accountants and have no long-term future in the business. Current assets may be held by a company for a duration of a complete accounting year, 12 months, or maybe less. A major reason for the conversion of current assets into cash within a very short amount of time is to pay off the current liabilities.

Examples

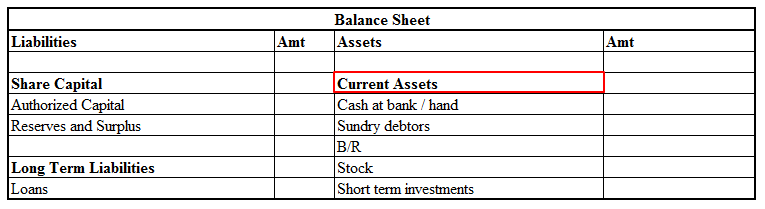

Some of the major examples of current assets are – cash in hand, cash at the bank, bills receivables, sundry debtors, prepaid expenses, stock or inventory, other liquid assets, etc.

- All of these assets are converted into cash within one accounting year.

- Liquid assets are a part of current assets. Although they are easier to be converted into cash than current assets.

- Current assets (along with current liabilities) help in the calculation of the current ratio. And they’re also referred to as circulating/floating assets.

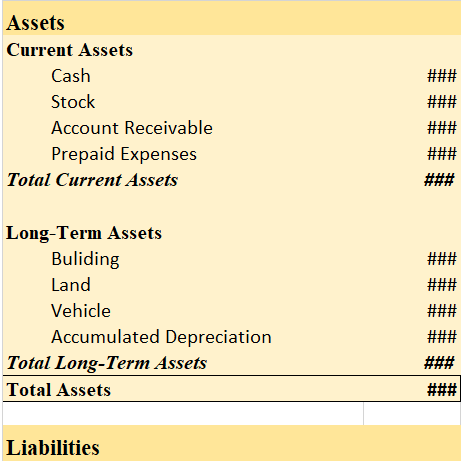

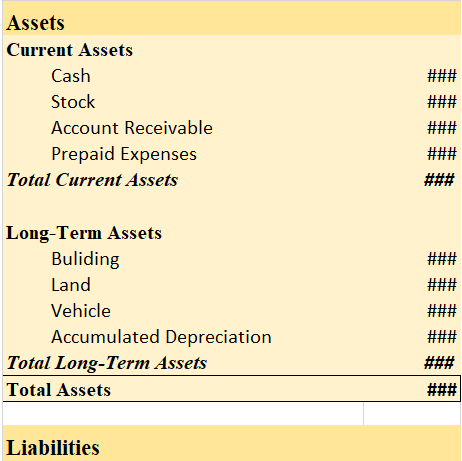

- Current assets are shown on the balance sheet (on the asset side) under the heading, current assets.

Current assets on the balance sheet

Balance Sheet (for the year…)

Accrual Accrual expense means the transaction that takes place in a particular period must be accounted for in that period only irrespective of the fact when such amount has been paid. An accrual of the expenditure which is not paid will be listed in the books of accounts. These accruals can be furtRead more

Accrual

Accrual expense means the transaction that takes place in a particular period must be accounted for in that period only irrespective of the fact when such amount has been paid.

An accrual of the expenditure which is not paid will be listed in the books of accounts. These accruals can be further divided into two parts

Accrual Expense-

Accrual Expense means any transaction that takes place in a particular period but the amount for it will be paid on a later period.

For example- If rent of 10,000 for the month of March was paid in April month then this rent will be accounted for in the books in March

For example- Interest of 1,000 for the month of March of the loan amount of 10,000 paid in April then will be accounted for in the books in March

These are the following accrued expense

Accrual Revenue-

Accrual Revenue means any transaction that takes place in a particular period but the amount for it will be received in the later period.

For example- If interest of 10,000 on bonds for the period of March is received in April months then this amount will be accounted for in March. These are the following accrued revenue

For example- Rent of 10,000 for the month of March received in April month then this rent will be accounted for in the books in March

- Accrual Income- Acrrual expense means the amount for any income received on a later period than the period when it pertains to be received

- Accrual Rent– Accrual rent means the amount for using the land of the entity by the other party is received at a later period than the period when it is put into use.

- Accrued Interest– Accrued interest means the amount of interest received on a later period than the period when it pertains to receive

See less