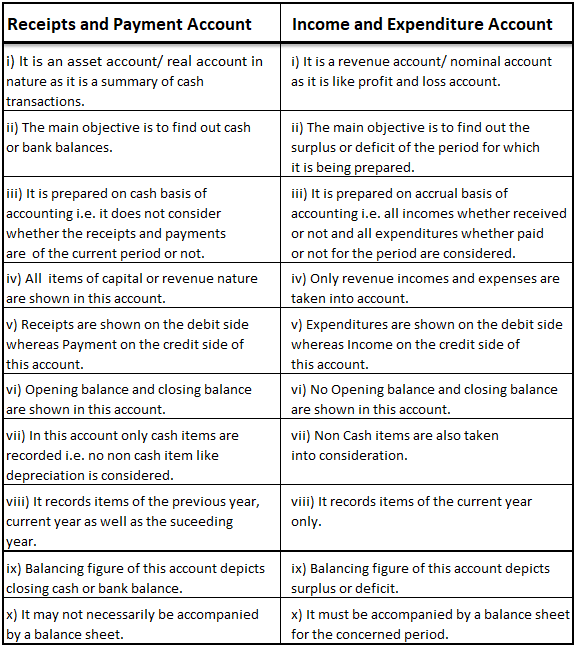

Receipts Amt Payments Amt To Balance b/d 85,000 By Doctors and Coaches Honorarium 25,000 To Subscription 68,500 By Medicines 15,500 To Entrance Fees 25,000 By Medical Equipment 30,000 To Life Membership Fees 30,000 By General Expenses 8,000 To Donations for tournament fund 20,000 By Furniture 20,000 To Sale of old Medical equipment (Book Value ...

In the books of Rural Literacy Society Income & Expenditure A/c for the year ended 31 March 2019 Expenditure Amt Amt Income Amt Amt To General Expenses 32,000 By Subscription (W.N.1) 2,72,000 To Newspapers 18,500 By Legacy 12,500 To Electricity 30,000 By Government Grant 1,20,000 To Rent 65,000Read more

In the books of Rural Literacy Society

Income & Expenditure A/c for the year ended 31 March 2019

| Expenditure | Amt | Amt | Income | Amt | Amt |

| To General Expenses | 32,000 | By Subscription (W.N.1) | 2,72,000 | ||

| To Newspapers | 18,500 | By Legacy | 12,500 | ||

| To Electricity | 30,000 | By Government Grant | 1,20,000 | ||

| To Rent | 65,000 | By Interest Received on Fixed Deposit | 9,000 | ||

| Less: Prepaid Rent (65,000/13) | -5,000 | 60,000 | (1,80,000*10%*6/12) | ||

| To Salary | 36,000 | ||||

| Add: Outstanding Salary | 6,000 | 42,000 | |||

| To Postage Charges | 3,000 | ||||

| To Loss on Sale of Furniture (W.N.2) | 13,000 | ||||

| To Surplus (excess of income over expenditure) | 2,15,000 | ||||

| 4,13,500 | 4,13,500 |

Balance Sheet as on 31 March 2019

| Liabilities | Amt | Amt | Assets | Amt | Amt |

| Capital Fund (W.N.3) | 3,85,500 | Fixed Deposit | 1,80,000 | ||

| Add: Surplus | 2,15,000 | ||||

| Advance Subscription | 5,000 | Books | 50,000 | ||

| Outstanding Salaries | 6,000 | Add: Purchased | 70,000 | 1,20,000 | |

| Furniture | 1,20,000 | ||||

| Add: Purchased | 1,05,000 | ||||

| Less: Sold | -50,000 | 1,75,000 | |||

| Outstanding Subscription | 15,000 | ||||

| Prepaid Rent | 5,000 | ||||

| Cash in Hand | 30,000 | ||||

| Cash at Bank | 82,000 | ||||

| Accrued Interest (W.N.4) | 4,500 | ||||

| 6,11,500 | 6,11,500 |

Working Notes:

W.N.1: Calculation of Subscription

| Subscription for 2018-19 | 2,65,000 |

| Add: Outstanding Subscription (31 March 2019) | 15,000 |

| Less: Outstanding Subscription (2017-18) | -8,000 |

| Total Subscription | 2,72,000 |

In the above calculation, for the year 2017-18 subscription amount was 12,000, and in the adjustment at the end of the year subscription was 20,000 so the difference of 8,000 is the amount of subscription that was outstanding.

W.N.2: Calculation of loss on sale of furniture

| Book Value of Furniture | 50,000 |

| Less: Sold | -37,000 |

| Loss on Sale of Furniture | 13,000 |

W.N.3: Calculation of Capital Fund

Balance Sheet as on 31 March 2018

| Liabilities | Amt | Assets | Amt |

| Capital Fund (Balancing Figure) | 3,85,500 | Books | 50,000 |

| Furniture | 1,20,000 | ||

| Outstanding Subscription | 20,000 | ||

| Cash in Hand | 40,000 | ||

| Cash at Bank | 1,55,500 | ||

| 3,85,500 | 3,85,500 |

W.N.4: Calculation of Accrued Interest

| Interest as of 30 September 2018 | 9,000 |

| Less: Interest as of 31 March 2019 | -4,500 |

| Accrued Interest | 4,500 |

In the books of Krish Fitness and Wellness Club Income & Expenditure A/c for the year ended 31 March 2020 Expenditure Amt Income Amt To Doctors and Coaches Honorarium 25,000 By Subscription (600*100) 60,000 To Medicines 15,500 By Entrance Fees 25,000 To General Expenses 8,000 By Miscellaneous ReRead more

In the books of Krish Fitness and Wellness Club

Income & Expenditure A/c for the year ended 31 March 2020

Working Notes:

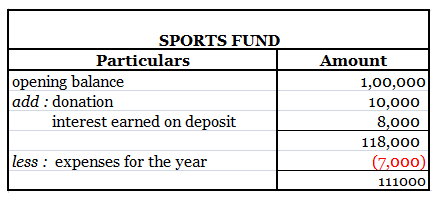

1.Calculation of Tournament Fund

2. Calculation of Loss on Sale of Medical Equipment