To begin with, lets us understand what the Companies Act 2013 tells about calls-in-advance, so basically as per section 50 of the companies act 2013 "A company may if so authorized by its articles, accepts from any members the whole or part of amount remaining unpaid on any share held by him, even iRead more

To begin with, lets us understand what the Companies Act 2013 tells about calls-in-advance, so basically as per section 50 of the companies act 2013 “A company may if so authorized by its articles, accepts from any members the whole or part of amount remaining unpaid on any share held by him, even if no amount has been called up”.

To be more precise whenever excess money is received by the company than, what has been called up is known as calls-in-advance.

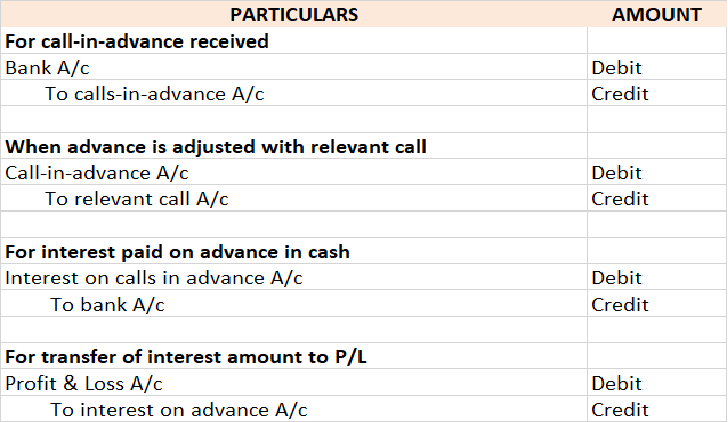

Accounting Treatment

Well, it is to be noted that calls-in-advance is never a part of share capital. A company when authorized by its article can accept those advance amounts and directly credit the amount received to the calls-in-advance account.

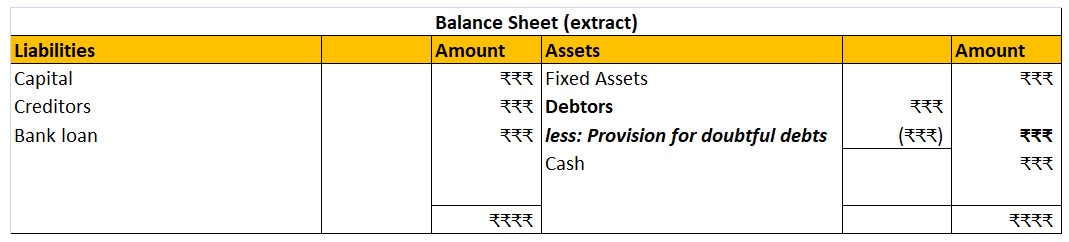

As these advance amounts are a liability for the company these are shown under the head current liability of the balance sheet until calls are made and are paid to the shareholders.

Since this is the liability of the company, it is liable to pay the interest amount on such call money from the date of receipt until the payment is done to the shareholders. The rate of interest is mentioned in the articles of association. If the article is silent regarding the rate on which interest is paid then it is assumed to be @6%.

Accounting Entry

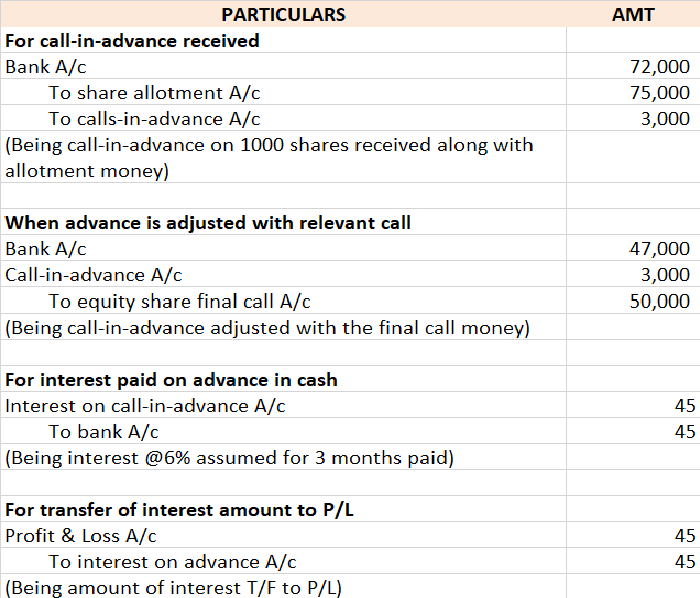

Bonnie let us understand the entries with help of an example

ADIDAS LTD issued 25,000 equity shares of Rs 10 each payable as follows:

ON APPLICATION Rs 5

ON ALLOTMENT Rs 3

ON FINAL CALL Rs 2

Application on 30,000 shares was received. excess money received on the application was refunded immediately. Mr. X who was allotted 1,000 shares paid the call money at the time of allotment and all amounts were duly received assume interest rate @6% for 3 months, so the relevant accounting entry goes as follows:

Important Points to be noted under calls-in-advance as per the companies act 2013

- The shareholder is not entitled to any voting rights on money paid until the said money is called for.

- No dividends are payable on advance money.

- Board may pay interest on advance not exceeding 12%.

- The shareholders are entitled to claim the interest amount as mentioned in the article, if there are no profits, then it must be paid out of capital because shareholders become the creditors of the company.

Yes, Goodwill is a fixed asset because it adds to the value of the business over a long period. Goodwill can never be calculated for a short period. GOODWILL Basically, goodwill is a premium or you can say an additional price you are paying because of the reputation of a firm or a person. YouRead more

Yes, Goodwill is a fixed asset because it adds to the value of the business over a long period. Goodwill can never be calculated for a short period.

GOODWILL

Basically, goodwill is a premium or you can say an additional price you are paying because of the reputation of a firm or a person.

You may have seen some famous shop in your locality which usually charges a higher price as compared to the other local shops selling the same product.

You may have also noticed that bigger brands like Bata, Titan, Zara, etc. charge higher prices for their products as compared to the same products available in the local market and people are even willing to pay for them. Ever wondered why?

This is because of the goodwill created by them over the years by providing quality products and services, good employee relationships, a strong customer base, social service, a brand name and so on. Customers trust them and for this trust, they are even willing to pay higher prices.

Goodwill is the quantitative value (i.e. in monetary terms) of the reputation of the firm in the market.

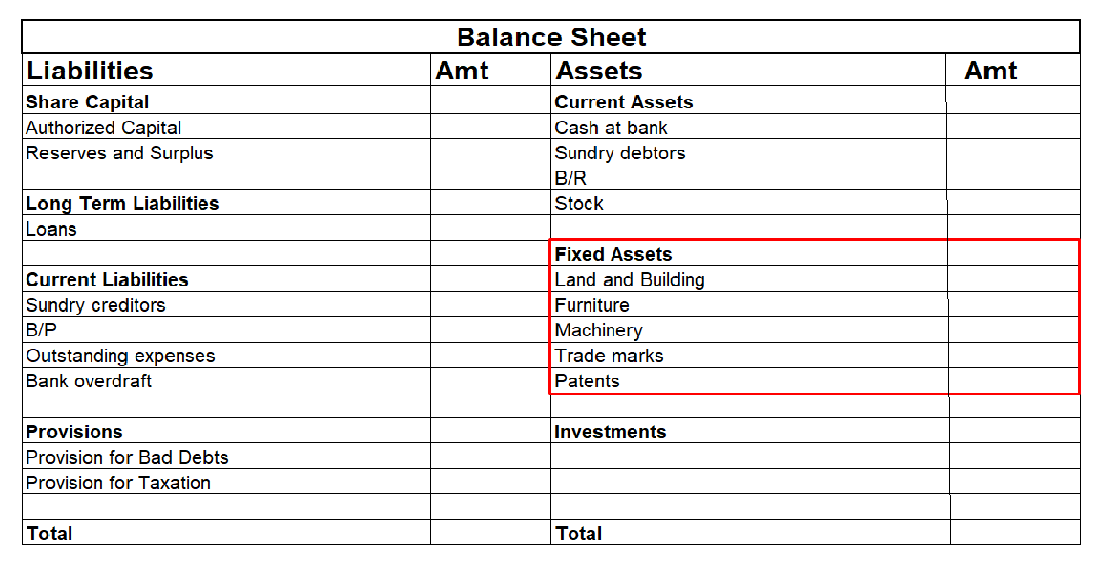

FIXED ASSETS

An asset is any possession or property of the business that enables the firm to get cash or any benefit in the future.

Fixed Assets are assets which are purchased for long-term use. They are for continued use in the business for producing goods or services and are not meant for resale. For example- Plant, machinery, building, goodwill, patents etc.

Fixed assets can be tangible or intangible.

Tangible assets are those assets which can be seen and touched and have physical existence like Plant and machinery, building, stock, furniture etc.

Intangible assets are those assets which cannot be seen or touched i.e. they don’t have any physical existence like goodwill, patent, trademark, prepaid expenses etc. Even though they can’t be seen or touched by they have value and are not fictitious assets.

Goodwill as a Fixed Asset

Goodwill is an intangible asset as it cannot be seen or touched but has value and adds value to the business over a long period. Thus, goodwill is a fixed asset.

It is shown in the balance sheet as a Fixed asset under the head Intangible asset.

Goodwill can be

Self-generated goodwill is created over a period due to the good reputation of the business. It is the difference between the value of the firm and the fair value of the net tangible assets of the firm.

Goodwill = Value of the firm – Fair value of net tangible assets

Here, F.V of net tangible assets = Fair value of tangible assets- Fair value of tangible liabilities

Purchased goodwill arises when one business purchases another business. It is the difference between the price paid for the purchased firm and the sum of the fair market value of the assets received and liabilities to be paid by them on behalf of the purchased firm.

Goodwill = Purchase price – (F.V of assets received + F.V of liabilities to be paid)

Only purchased goodwill is recorded in the books of accounts because it is difficult to correctly calculate the value of self-generated goodwill as the future is uncertain, also its valuation depends on the judgement of the person calculating it, which defers from person to person. Since there is no fixed standard to calculate self-generated goodwill only purchased goodwill is recorded as the price paid for it at the time of acquiring another business.

Suppose Firm A acquired Firm B.

Purchase price= $100,000

Assets received=$60,000

Liabilities (to be paid by Firm A on behalf of Firm B) = $10,000

Goodwill = $100,000 – ($60,000 + $10,000) = $30,000

This, goodwill of $30,000 will be recorded under the head Fixed Asset, subhead Intangible Assets in the balance sheet of Firm A (that is in the balance sheet of the acquiring firm)

See less