Bank statement and bank column of cash book Bank statement and cash column of cash book Bank column of cash book and cash column of cash book None of the above

Simply explaining the meaning of the useful life of an asset, it is nothing but the number of years the asset would remain in the business for purpose of revenue generation, making it more simple, the amount of time an asset is expected to be functional and fit for use. It is also called economic lRead more

Simply explaining the meaning of the useful life of an asset, it is nothing but the number of years the asset would remain in the business for purpose of revenue generation, making it more simple, the amount of time an asset is expected to be functional and fit for use. It is also called economic life or service life

It is a useful concept in accounting as it is used to work out depreciation. By knowing this useful life of an asset an entity can easily analyze how to allot the initial cost of an asset across the relevant accounting period rather than doing it unfairly manner.

How do we calculate the useful life of an asset?

The useful life of an asset is not an accounting policy, but an accounting estimate. calculating useful life is not an exact phenomenon but an estimate that is done because it directly impacts how much an asset is to expense every year.

Factors affecting “how long an asset is expected to be useful” depends on some stated points as below:

- Usage, the more the assets are used, the more quickly it will deteriorate.

- Whether the asset is new at the time of purchase or reused model.

- Change in technology.

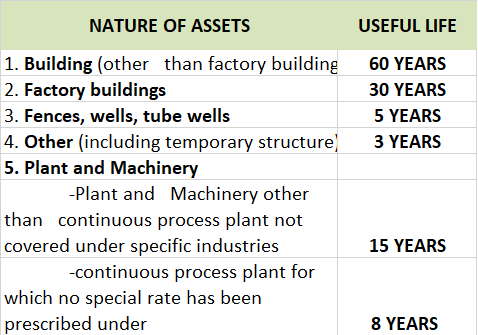

As per the companies act 2013, some of the useful life of assets are stated below

To know more about the different categories of assets you can follow the given link useful life of assets.

POINT TO BE NOTED:- There lies a huge difference in the useful life v/s the physical life of an asset. It is very important to note that amount of time an asset is used in a business is not always be same as an asset’s entire life span.

See less

The correct answer is the 1. Bank statement and bank column of the cash book, because it will help the business to verify whether amounts entered and entries recorded are correct or not. It will also help in verifying the balances of bank statements and cash books whether they tally or not. What isRead more

The correct answer is the 1. Bank statement and bank column of the cash book, because it will help the business to verify whether amounts entered and entries recorded are correct or not. It will also help in verifying the balances of bank statements and cash books whether they tally or not.

What is Reconciliation?

Reconciliation is an accounting procedure that compares two sets of records to check figures are correct and in agreement. Reconciliation can also be used for personal purposes.

What is a Bank Reconciliation Statement?

A statement showing causes of disagreement between the balance of bank statement and bank column of the cash book at the end of a specific period is called a Bank Reconciliation Statement.

Steps in preparation of Bank Reconciliation Statement

Step 1: Comparing items appearing on the debit and credit sides of the bank statement and bank column of the cash book.

Step 2: Make a list of missed entries.

Step 3: Analyse the causes of differences.

Step 4: Select the date for the preparation of the Bank Reconciliation Statement.

Step 5: Choose the starting point i.e balance as per cash book or balance as per bank statement.

Step 6: Adjust the starting point by adding or subtracting the missed entries.

Step 7: Bank Statement must match with the cash book.

To prepare a bank reconciliation statement a business will need a bank statement from its bank and cash book which it prepares to record entries.

See less