Introduction The term 'gain ratio' is related to partnership accounting. Gain ratio refers to the ratio in which existing partners of a partnership firm, divide among themselves, the share of profit and loss of the outgoing partners. There is a method of calculating this gain ratio. The method alongRead more

Introduction

The term ‘gain ratio’ is related to partnership accounting. Gain ratio refers to the ratio in which existing partners of a partnership firm, divide among themselves, the share of profit and loss of the outgoing partners.

There is a method of calculating this gain ratio. The method along with the concept behind gain ration is discussed below.

Concept behind gain ratio

A partnership firm is a form of business organisation which is conducted and carried on by members known as partners. It requires at least two partners to start a firm and the maximum limit is 50.

The partners share the profit and loss of a business in a ratio known as Profit and loss sharing ratio.

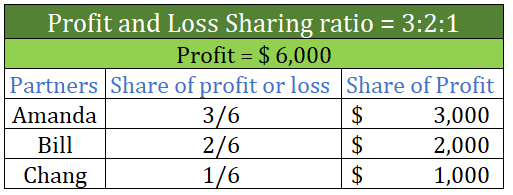

For example, Amanda, Bill and Chang are partners, having a P/L sharing ratio of 3:2:1 i.e. Amanda is getting 3/6, Bill is getting 2/6 of the same and Chang is getting ⅓ of the profit and loss

If the profit is $6,000 , then Amanda will get $3,000 (3/6 of $6,000) and Bill will get $2,000 (2/6 of $6,000) and Chang will get $1,000 (1/6 of $6,000).

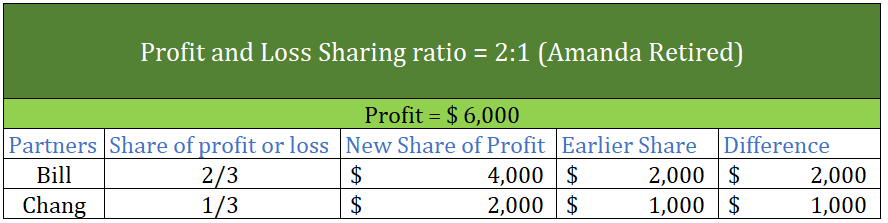

Now if Amanda retires from the firm, then naturally, Bill and Chang’s share of profit will increase.

The profit and loss sharing ratio will now be 2:1 (earlier it was 3:2:1) and the share of profit of Bill will be $4,000 and of Chang will be $2,000.

Calculation of gain ratio

The formula for calculating gain ratio = New ratio – Old Ratio

As per the above case:

- Gain ratio of Bill = 2/3 – 2/6 = 2/6

- Gain ratio of Chang = 1/3 – 1/6 = 1/6

Therefore the gain ratio in which Bill and Chang gained the share of profit of Amanda is 2/6 : 1/6 or simply 2:1

This is how we can calculate the gain ratio. But one thing to notice is that the gain ratio is equal to the P/L sharing ratio of the partnership between Bill and Chang.

Hence, whenever a partner retires and the existing partner keep the P/L sharing ratio unchanged among themselves then, the gain ratio will be equal to their P/L sharing ratio. In that case, there is no need to calculate the gain ratio from the formula given above.

But, when the remaining partners change the P/L sharing ratio among themselves after a partner retires, then the gain ratio is to be calculated using the formula given above.

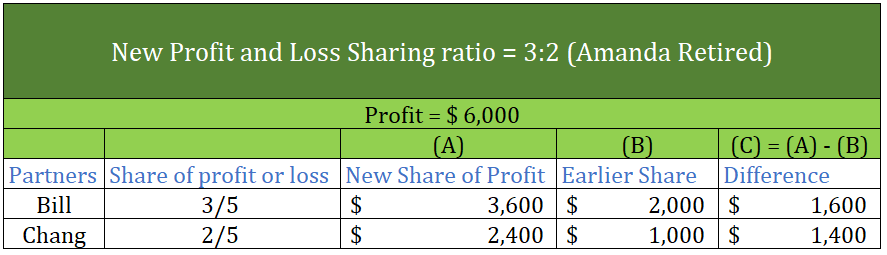

Suppose, upon retirement of Amanda, Bill and Chang change the P/L sharing between them to from 2:1 to 3:2

In that case,

- The gain ratio of Bill = 3/5 – 2/6 = 8/30

- The gain ratio of Chang = 2/5 – 1/6 = 7/30

Therefore the gain ratio in which Bill and Chang will gain the share of profit of Amanda is 8/30 : 7/30 or simply 8:7

When a firm grants an extra amount of reward to its employees based on their performance, it is termed a bonus. An accrued bonus is contingent on performance. Bonus accruals are recorded in the books so that inaccuracies can be avoided in the financial statements. Such bonuses may be given as a singRead more

When a firm grants an extra amount of reward to its employees based on their performance, it is termed a bonus. An accrued bonus is contingent on performance. Bonus accruals are recorded in the books so that inaccuracies can be avoided in the financial statements.

Such bonuses may be given as a single flare amount or as a percentage of their salaries. These bonuses can be given quarterly or annually or in any manner in which the firm decides.

If the bonus is accrued to its employees at 5% of their salary of Rs 30,000, then the accrual bonus can be shown in the journal as follows:

When it is time to pay such bonus amounts to its employees, then they can be journalised as:

In this case, the accrued bonus liability is eliminated and hence debited because according to the rule of accounting, “ Decrease in liability is debited” whereas cash account is credited since “the decrease in the asset is credited.”:

Failing to accrue these bonuses will lead to an overstatement of revenues in the financial statements and hence result in inaccurate data. If employees do not meet the required performance targets, then a bonus will not be given and hence the entries will be reversed.

See less