A bills receivable book is a subsidiary book that shows the details of various bills receivables drawn on customers. It shows the amount, due date, date when the bill was drawn, name of the acceptor, and various other details pertaining to each bill. A bills payable book is a subsidiary book that shRead more

A bills receivable book is a subsidiary book that shows the details of various bills receivables drawn on customers. It shows the amount, due date, date when the bill was drawn, name of the acceptor, and various other details pertaining to each bill.

A bills payable book is a subsidiary book that shows the details of various bills that suppliers have drawn on the business. It shows the amount, due date, date when the bill was drawn, name of the drawer and various other details pertaining to each bill.

The total of both these books is ultimately transferred to the general ledger. From there, it is used in drafting the balance sheet.

Importance of bills receivable and bills payable books

Bills receivable books help us know the amount that each customer is liable to pay us on specific dates while bills payable books help us know the amounts that we have to pay our various suppliers on certain dates.

Together these books help us handle our cash flows in an efficient manner.

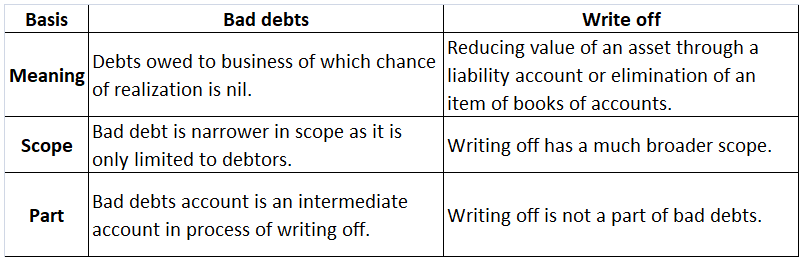

We can evaluate our credit cycle. Bills receivable books help us avoid bad debts while bills payable books help us to avoid defaults.

Difference between bills receivable and bills payable

These are the primary differences between bills payable and bills receivable:

- Bills receivable represent the amounts that the business is to receive from customers while bills payable represent the amounts that the business has to pay to suppliers.

- Bills receivable are recorded as an asset in the balance sheet while bills payable are recorded as a liability.

- Bills receivable are drawn by the business on the customers while the bills payable are drawn by the suppliers on the business.

- Bills receivable are the outcome of credit sales while bills payable are the outcome of credit purchases.

- Bills receivable result in an inflow of cash while bills payable result in an outflow of cash.

- The dishonor of a bill receivable is recorded as an increase in the debtors of the business. Default on payment of bills payable may occur either because the business has become bankrupt or the business may record an increase in creditors.

We can conclude that both bills receivable and bills payable books are subsidiary books. Bills receivable shows the details of every bill that the business has drawn on each credit customer. Bills payable show the details of every bill that each credit supplier has drawn on the business.

See less

To begin with, let me first give you a small explanation of what Contingent assets are A contingent asset is a potential asset or economic benefit that does not exist currently but may arise in the near future. Such an asset arises from an uncertain and unpredictable event. To make it clear with anRead more

To begin with, let me first give you a small explanation of what Contingent assets are

A contingent asset is a potential asset or economic benefit that does not exist currently but may arise in the near future. Such an asset arises from an uncertain and unpredictable event.

To make it clear with an example: String Co. filed a lawsuit against a competitor company Weave Tech Co. for infringing on company ABC’s patent. Even if it is probable (but not certain) that Strings Co. will win the lawsuit, it is a contingent asset.

As such, it will not be recorded in Strings Co. general ledger accounts until the lawsuit is settled.

At most the Strings Co. can do is, prepare a note disclosing the fact that it has filed the lawsuit the outcome of which is uncertain.

Disclosing Contingent Assets

For Example, The court orders for reimbursement to Strings Co. say 1,00,000 for the damages, but it has not yet received the money. Although it is virtually certain that the company will receive the money in the near future, it will be treated as an asset and can be disclosed in the balance sheet on the assets side.

For Example, Strings Co. filed a lawsuit against a competitor company Weave Tech for infringing on Strings Co. patent. Even if it is probable (but not certain) that Strings Co. will win the lawsuit, it is a contingent asset.

As such, it will not be recorded in Strings company’s general ledger until the lawsuit is settled.

At most the Strings Co. can do is, prepare a note disclosing the fact that it has filed the lawsuit the outcome of which is uncertain.

In this case, the disclosure of it is not permitted.

See less