The answer is B. False. Before jumping on the solution to know why goodwill is not fictitious, we need to know what are fictitious assets? Fictitious assets are false assets or not true assets. These are not assets but expenses & losses that are not written off from the profit & loss accountRead more

The answer is B. False. Before jumping on the solution to know why goodwill is not fictitious, we need to know what are fictitious assets?

Fictitious assets are false assets or not true assets. These are not assets but expenses & losses that are not written off from the profit & loss account but shown in the balance sheet as assets under the head miscellaneous expenditure. For example preliminary expenses, loss on issue of debentures, etc.

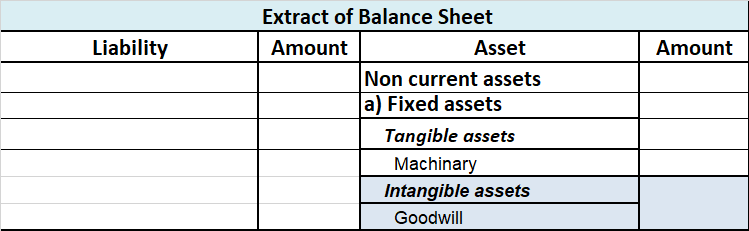

Goodwill is not a fictitious asset but an intangible asset which means it has no actual physical appearance and cannot be touched and felt like other assets like buildings and machinery. It is nothing but a firm’s reputation which can be sold just like other assets help the business grow and earn revenue. Goodwill is shown in the balance sheet as follows:

To begin with, let me first give you a small explanation of what Contingent assets are A contingent asset is a potential asset or economic benefit that does not exist currently but may arise in the near future. Such an asset arises from an uncertain and unpredictable event. To make it clear with anRead more

To begin with, let me first give you a small explanation of what Contingent assets are

A contingent asset is a potential asset or economic benefit that does not exist currently but may arise in the near future. Such an asset arises from an uncertain and unpredictable event.

To make it clear with an example: String Co. filed a lawsuit against a competitor company Weave Tech Co. for infringing on company ABC’s patent. Even if it is probable (but not certain) that Strings Co. will win the lawsuit, it is a contingent asset.

As such, it will not be recorded in Strings Co. general ledger accounts until the lawsuit is settled.

At most the Strings Co. can do is, prepare a note disclosing the fact that it has filed the lawsuit the outcome of which is uncertain.

Disclosing Contingent Assets

For Example, The court orders for reimbursement to Strings Co. say 1,00,000 for the damages, but it has not yet received the money. Although it is virtually certain that the company will receive the money in the near future, it will be treated as an asset and can be disclosed in the balance sheet on the assets side.

For Example, Strings Co. filed a lawsuit against a competitor company Weave Tech for infringing on Strings Co. patent. Even if it is probable (but not certain) that Strings Co. will win the lawsuit, it is a contingent asset.

As such, it will not be recorded in Strings company’s general ledger until the lawsuit is settled.

At most the Strings Co. can do is, prepare a note disclosing the fact that it has filed the lawsuit the outcome of which is uncertain.

In this case, the disclosure of it is not permitted.

See less