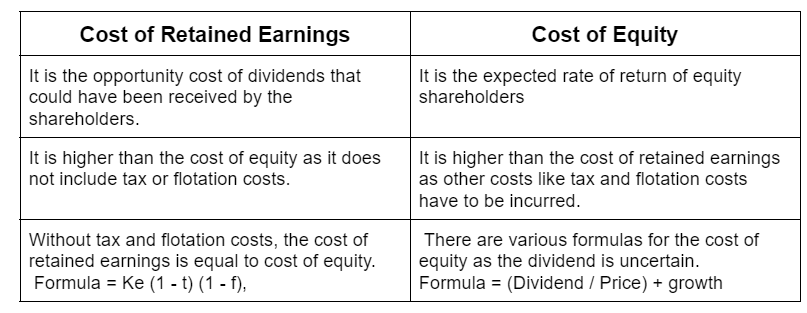

Shareholder's Equity Meaning - Shareholder's Equity is the amount invested into the Company. It represents the Net worth of the Company. It is also where the owners have the claim on the Assets after the Debts are settled. It Calculation of Shareholder's Equity Method 1 Shareholder's Equity = TotalRead more

Shareholder’s Equity

Meaning – Shareholder’s Equity is the amount invested into the Company. It represents the Net worth of the Company. It is also where the owners have the claim on the Assets after the Debts are settled. It

Calculation of Shareholder’s Equity

Method 1

Shareholder’s Equity = Total Assets – Total Liabilities

Method 2

Shareholder’s Equity = Share Capital + Retained Earnings – Treasury Stock/Treasury Shares

Components of the Shareholder’s Equity

From the above Method 1, it can be understood that shareholder’s equity comprises of

Net Assets = Current Assets + Non-current Assets, reduced by

Net liabilities = Current liabilities + Long-term liabilities

where Long-term liabilities = Long-term debts + Deferred long-term liabilities + Other liabilities

Also from the method 2,

Share Capital = Outstanding shares + Additional Paid-up share capital

Retained Earnings are the sum of the company’s earnings after paying the dividends

Treasury stocks = Shares repurchased by the company

Example of Shareholder’s Equity

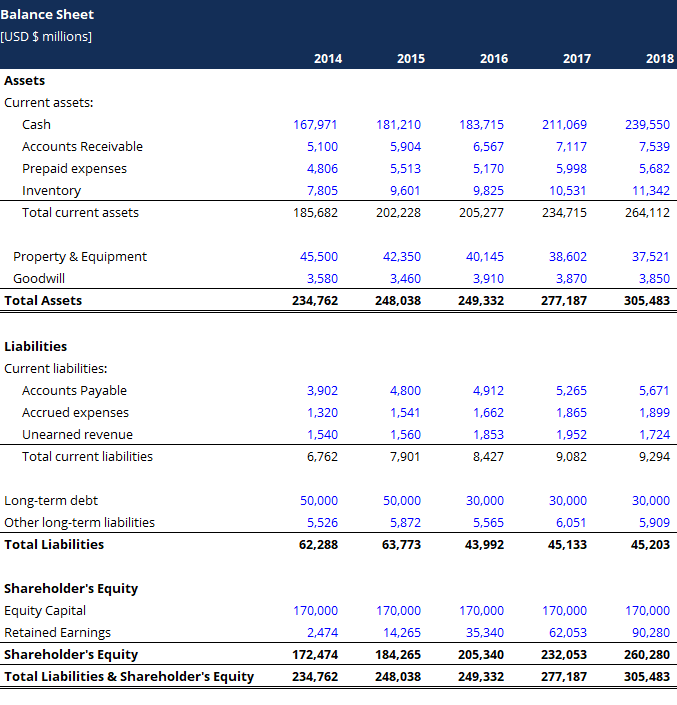

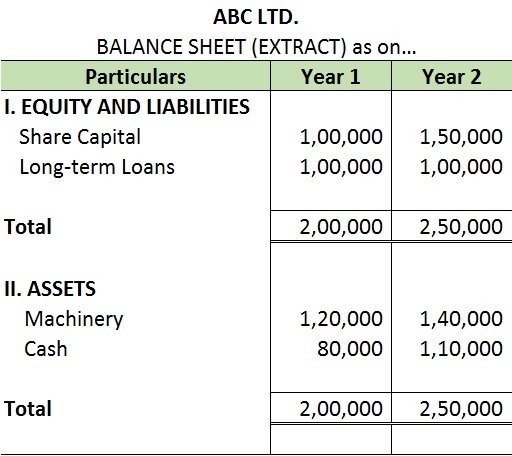

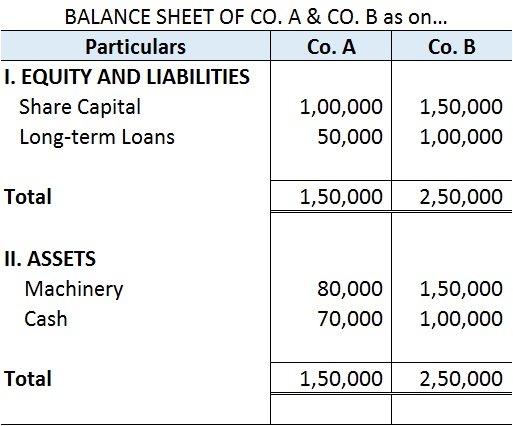

The shareholder’s Equity is represented in the Balance Sheet as below;

See less

The commercial banks are required to keep a certain amount of their deposits with the central bank and the percentage of deposits that the banks are required to keep as reserves is called Cash Reserve Ratio. The banks have to keep the amount to maintain the Cash Reserve Ratio with the RBI. CRR meansRead more

The commercial banks are required to keep a certain amount of their deposits with the central bank and the percentage of deposits that the banks are required to keep as reserves is called Cash Reserve Ratio.

The banks have to keep the amount to maintain the Cash Reserve Ratio with the RBI.

CRR means that commercial banks cannot lend money in the market or make investments or earn any interest on the amount below what is required to be kept in CRR.

RBI mandates Cash Reserve Ratio so that a percentage of the bank’s deposit is kept safe with the RBI, hence, in an uncertain event bank can still fulfill its obligation against its customers.

CRR also helps RBI to control liquidity in the economy. When CRR is kept at a higher rate, the lower the liquidity in the economy, and similarly when CRR is kept at a lower rate, there is higher liquidity in the economy.

The Reserve Bank of India also regulates inflation through the Cash Reserve Ratio:

The formula for CRR is-

Reserves maintained with Central Banks / Bank Deposits * 100%

For example:

The current CRR is 3% which means that for every Rs 100 deposit in the commercial banks have to keep Rs 3 as a deposit with RBI.

See less