Wages Outstanding Wages and Salaries Director’s Remuneration Advance Payment of Wages All of the Above

Meaning of Opening Stock Opening stock is the inventory or stock of goods that are available at the beginning of the new accounting year carried down from the previous year's closing stock which is recorded in the books of accounts. In simple words, Opening stock is the goods/quantity/products thatRead more

Meaning of Opening Stock

Opening stock is the inventory or stock of goods that are available at the beginning of the new accounting year carried down from the previous year’s closing stock which is recorded in the books of accounts.

- In simple words, Opening stock is the goods/quantity/products that are held by a business at the beginning of a new accounting period and it is the closing stock of the preceding year carried down.

- Similarly, the closing stock is the number of unsold goods that remain with the business at the end of an accounting year and is further carried down to the next year as Opening Stock.

Formula

There are 3 main formulas used for Opening Stock’s calculation. They are-

- For manufacturing companies

Opening Stock = Raw Material Cost + Work in Progress + Finished Goods Cost

- When only Sales, GP, COGS, and Closing Stock are given

Opening Stock = Sales – Gross Profit – Cost of Goods Sold + Closing Stock

- You can use this one when only limited information is provided

Opening Stock = COGS + Closing Inventory – Purchases

Types of Opening Stock

There are three types of Opening Stock or we may also say that Opening Stock consists of these 3 elements. They are-

- Raw Materials- These are the unprocessed goods held by a business that is yet to be converted into finished goods.

- Work in Progress- These include the goods that are in process but not converted into finished goods.

- Finished Goods- These are the goods/products that have completed the manufacturing process but have not yet been sold.

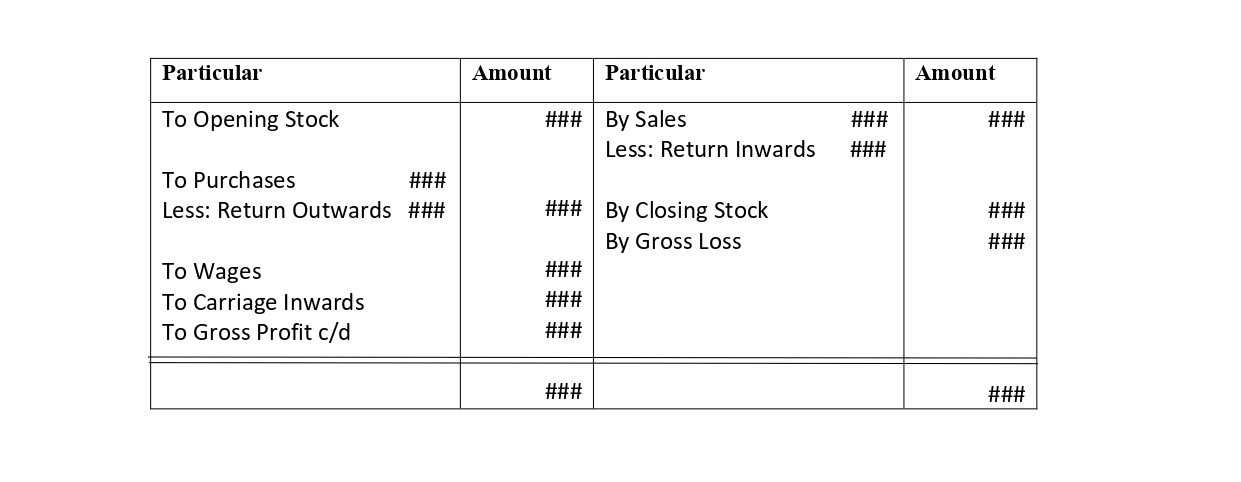

Opening Stock in Final Accounts

Opening stock is a part of the Trading Account while preparing the Final Accounts. And this is how it is posted in the Trading A/c.

Trading A/c (for the year ending…)

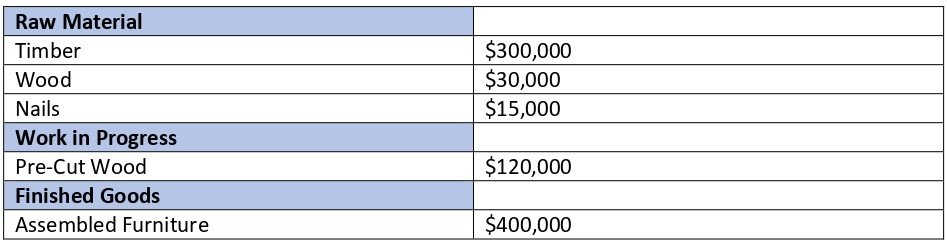

Example of Opening Stock

Example

IKEA, the biggest Furniture manufacturer collected this data on April 1, 2021,

Timber – $300,000

Wood – $30,000

Nails – $15,000

Pre-cut Wood – $120,000

Assembled Furniture – $400,000

Now, adding them (as said earlier, Opening stock is a combination of these three.)

Opening Stock (Raw Material + Work in Progress + Finished Goods) = $865,000

Therefore, that’s how one can calculate Opening Stock.

See less

The correct answer is option B. Wages and salaries are debited to the trading account. The trading account helps us to determine the Gross Profit Or Loss that a company earns or incurs by carrying on its core manufacturing or trading activities. Let us discuss the above items and their treatments inRead more

The correct answer is option B. Wages and salaries are debited to the trading account.

The trading account helps us to determine the Gross Profit Or Loss that a company earns or incurs by carrying on its core manufacturing or trading activities.

Let us discuss the above items and their treatments in the final accounts one at a time:

Wages Outstanding

Firstly, “wages outstanding” is not debited into the trading account. It is a liability that is shown in the balance sheet.

Outstanding wages imply remuneration due to be paid to the workers for the services they have already rendered to the business.

Since the company has already received the service, it becomes a legal obligation for it to pay the wages to the workers for those services. Hence, outstanding wages are a liability.

Wages and Salaries

Wages and Salaries are debited to the trading account.

Wages Vs Salaries

Let us understand the difference between wages and salaries. Wages are the regular payments that are made daily, weekly or fortnightly. Such payments are mostly made to factory workers.

Salaries, on the other hand, are assumed to imply the remuneration paid to office workers and sales staff.

Wages are debited to the trading account, while salaries are debited to the Profit and Loss account.

Director’s Remuneration

No, the director’s remuneration is not debited to the trading account. This is because director’s generation is a business expense. It is a kind of salary provided to the director for the services rendered by him to the company.

Directors’ remuneration refers to compensation the company gives to its directors for the services rendered. It is debited to the Profit and Loss Account.

Advance Payment of Wages

No, advance payment of wages is not debited to a trading account. It is shown by reducing it to wages. Advance payment of wages implying paying remuneration to the workers before the commencement of the period for which the wages relate to.

However, one must note that if both wages and prepaid wages appear within the trial balance, then only the figure written against wages would appear in the trading account. There would be no treatment for prepaid wages.

Let us consider a scenario where wages of amount 5,000 is appearing inside trial balance. Outside the trial balance, the following information is provided

In the above case, the total wages to be debited to the trading account would be 5,000 + 1,000 – 2,000 = 4,000

Significance of the Final Accounts

See less