Sundry debtor refers to either a person or an entity that owes money to the business. If someone buys some goods/services from the business and the payment is yet to be received, a group of such individuals or entities is called sundry debtors. Sundry debtors are also referred to as trade receivableRead more

Sundry debtor refers to either a person or an entity that owes money to the business. If someone buys some goods/services from the business and the payment is yet to be received, a group of such individuals or entities is called sundry debtors. Sundry debtors are also referred to as trade receivables or account receivables.

The term ‘Sundry’ means various or several, referring to a collection of miscellaneous items combined under one head. Sundry debtors typically arise from core business activities such as sales of goods or services. The business treats them as an asset.

Example

Suppose you run a business, ABC Ltd. Mr. Y bought goods from you on credit. Therefore, Mr. Y will be recorded as Debtor (current asset) in your books of accounts. Similarly, a collection of such debtors is viewed as sundry debtors from the business’ point of view.

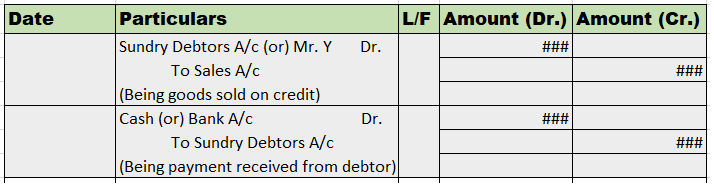

Journal Entry

Rules

As per the golden rules of accounting, we ‘debit the receiver and credit the receiver’. That’s how in this journal entry we’ll be debiting the sundry debtor’s account. Also, ‘debit what comes in and credit what goes out.’ That’s why sales a/c is credited and cash a/c is debited.

As per the modern rules of accounting, ‘debit the increase in asset and credit the decrease in asset’. That’s why we debit sundry debtors and cash a/c. And credit sales a/c when goods are sold and inventory decreases.

Why debtor is an asset?

As we know, a debtor refers to a person or entity who owes money to the business which means, the money is to be received by them in the future, making them an asset. On the other hand, creditors are a liability to the firm as we owe them money and it is to be paid by us in the near future, making it an obligation for the firm.

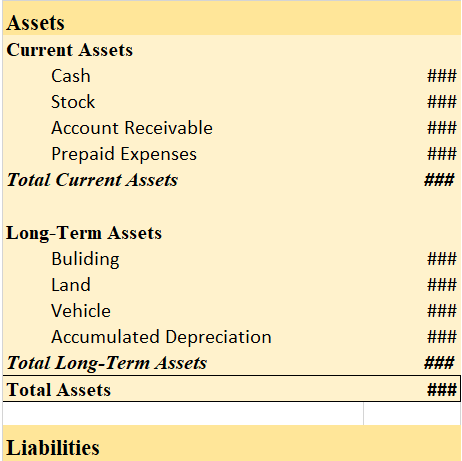

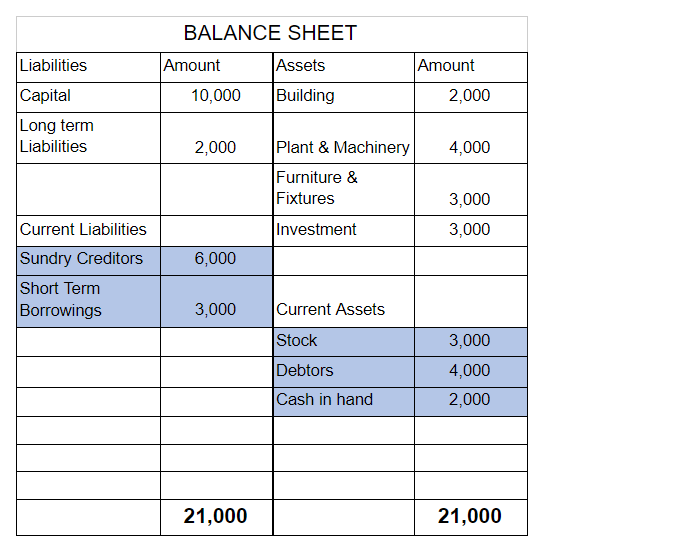

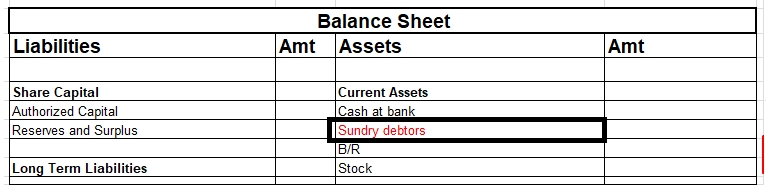

Sundry Debtors in Balance Sheet

Sundry debtors are shown under the current asset heading on the balance sheet. They are often referred to as account receivables.

Balance Sheet (for the year ending….)

Brands can be considered as an Intangible asset as they are a long-term investment done by the company and it gives benefit to an entity in future periods. Like any other intangible asset, brands require long-term investment and will pay over time. Like any other asset, these brands can be bought anRead more

Brands can be considered as an Intangible asset as they are a long-term investment done by the company and it gives benefit to an entity in future periods.

Like any other intangible asset, brands require long-term investment and will pay over time. Like any other asset, these brands can be bought and sold. Brands are best used when they serve the vision and mission of the company.

So, we can definitely consider an organization brand as an intangible as it is expected to increase sales volume in the future period.

Further, we can understand both terms to get a deep understanding-

BRAND

Brand means a product, or service which has a unique identification and can be distinct from other products in the market. Branding is a process by which expenditure is incurred by an entity to create awareness towards the product in the customer’s eyes.

For example- Maggie, Coca-Cola, BMW

Brands can be created through these elements-

INTANGIBLE ASSETS

Intangible asset are assets that can’t be seen or touched but the benefit of it occur in future periods for the entity. Even though intangible assets have no physical form but their benefits will accrue in future years. Businesses commonly hold intangible assets. Intangible assets can be further bifurcated in

Definite– Intangible assets that stay and give benefit for a limited or specific period of time covered under this

For example- An agreement is entered with an entity to patent a product for 5 years so this will stay for a definite period only

Indefinite– Intangible assets that stay and give benefit for an unlimited period of time covered under this

For example- A brand which is made by an entity will stay for an indefinite period

Intangible assets can be in various forms these are the following –

Trademark– A trademark is a sign, design, and expression that distinguish the company’s product or services from other company. Trademark is considered an Intellectual Property Right.

Goodwill– Goodwill refers to the value of the company that the company gets from its brand, customer base, and brand Reputation associated with its intellectual property.

Patents– A patent refers to a right reserved for a product exclusively by a person or entity. Under this the right of such making of the product gets reserved by the company and other person or entity can’t make this product.

Copyright– Copyright refers to an intellectual property right that protects the work of the original owner from being copied by some other person.

Brand– Brand means a product, or service that has a unique identification and can be distinct from other products in market

So, we can definitely consider that brand is a subpart of an intangible asset and can be considered as an intangible asset as it also can’t be touched or seen. Still, its benefit will accrue till future time. These both help an entity to grow its business till the future

See less