A. Events B. Transactions C. Journals D. None of These

Accumulated profit is the amount of profit left after the payment of dividends to the shareholders. It is also known as retained earnings. It is the profit that is not distributed as dividends to shareholders, hence called retained earnings. This accumulated profit is an important source of internalRead more

Accumulated profit is the amount of profit left after the payment of dividends to the shareholders. It is also known as retained earnings. It is the profit that is not distributed as dividends to shareholders, hence called retained earnings. This accumulated profit is an important source of internal finance for a company. Accumulated profit or retained earnings can be ascertained using the following formula:

Accumulated profit = Opening balance of accumulated profit + Net Profit/Loss (loss being in the negative figure) – Dividend paid

Accumulated profit can be put to the following uses:

- To reinvest into the business in form of capital assets or working capital.

- To repay the debt of the company.

- To pay dividends in future.

- To set off the net loss made by the company.

Accumulated profit and reserves are often considered the same. But in substance, they are not. The reserves are actually part of the accumulated profit, but the converse is not true. They are created by transferring amounts from the accumulated profit. While reserves are created for purpose of strengthening the financial foundation of a firm, the accumulated profit’s main purpose is to make reinvest in the business to increase its growth.

The amount of accumulated profits depends upon the retention ratio and dividend payout ratio of a company. The retention ratio is the opposite of the dividend payout ratio.

The formula of dividend pay-out ratio = Dividend payable/Net Income

And retention ratio = 1 – (Dividend payable/Net Income)

If the retention ratio is more than the dividend payout ratio, the accumulated profit remains positive.

See less

The correct option is Option C: Journal Entries. Journal entries are the primary entries in the books of accounts and they are passed when any transaction or event takes place. Every journal entry has a dual effect i.e. two or more accounts are affected. For example, When cash is introduced in the bRead more

The correct option is Option C: Journal Entries.

Journal entries are the primary entries in the books of accounts and they are passed when any transaction or event takes place. Every journal entry has a dual effect i.e. two or more accounts are affected.

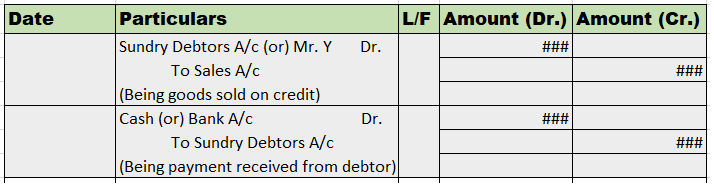

For example, When cash is introduced in the business, the journal entry passed is:

Cash A/c Dr. ₹10,000

To Capital A/c ₹10,000

The accounts affected here are Cash A/c and Capital A/c.

Cash A/c gets debited by ₹10,000,

and Capital A/c get credited by ₹10,000.

All the processes of accounting are conducted in an ordered manner known as the accounting cycle.

The first step in an accounting cycle is to identify the transactions and events which are monetary in nature.

The second step is to record the identified transactions in form of journal entries.

And the third step is to make postings in the general ledger accounts as per the journal entries.

Hence, the preparation of the ledger is the third step in the accounting cycle and is prepared from the journal entries.

See less