The term ‘contra’ means opposite or against. In financial accounting, we encounter the term ‘contra’ in: Contra accounts Contra entries The meaning of contra in the above mention terms is also the same as their general meaning. Contra accounts mean the account which is opposite of the account it corRead more

The term ‘contra’ means opposite or against. In financial accounting, we encounter the term ‘contra’ in:

- Contra accounts

- Contra entries

The meaning of contra in the above mention terms is also the same as their general meaning. Contra accounts mean the account which is opposite of the account it corresponds to.

Contra entries are entries of the debit and credit aspects related to the same parent account. Let’s discuss them in detail.

Contra accounts

Any account which is created with the purpose of reducing or offsetting the balance of another account is known as a contra account.

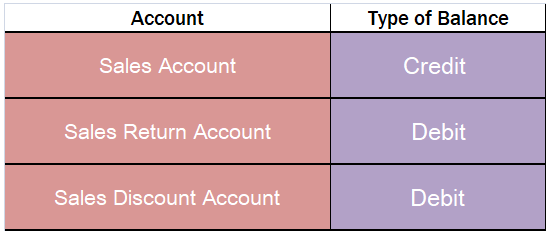

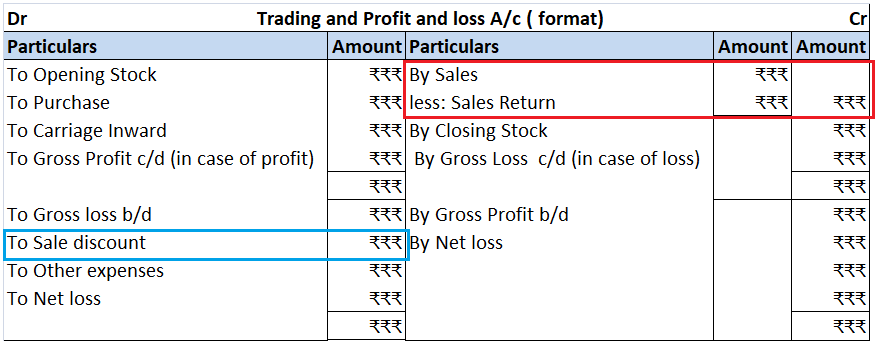

A contra account is just the opposite of the account to which it relates. The most common examples are the sales discount account and sales return account which is the contra account of the sales account. They are just the opposite of the sales accounts.

Contra Entries

Contra entries refer to the entries which show the movement of the amount within the same parent account. Here, the debit and credit entry is posted on the debit and credit side respectively of a single parent account. Mainly, contra entries are the entries involving cash and bank accounts.

The following transactions are recorded as contra entries:

- Cash to Bank transactions: Deposit of cash into the bank account by the entity.

- Bank to Cash transactions: Withdrawal of cash from the bank.

- Cash to cash transactions: Transfer of cash to the petty cash account.

- Bank to Bank transactions: Transfer of amounts from one bank account to other bank accounts of the same entity.

Contra entries are marked by the letter ‘C’ beside the postings in the ledger. Deposit of cash in to bank will be posted in cashbook as below:

Firstly, let’s understand the meaning of both terms. Revenue receipts: The term 'revenue' suggests these are the amounts received by a business due to its operating activities. These receipts arise in a recurring manner in a business. Such receipts don’t affect the balance sheet. They are shown inRead more

Firstly, let’s understand the meaning of both terms.

Revenue receipts: The term ‘revenue‘ suggests these are the amounts received by a business due to its operating activities. These receipts arise in a recurring manner in a business. Such receipts don’t affect the balance sheet. They are shown in the statement of profit or loss. Such receipts are essential for the survival of the business.

Examples of revenue receipts are as follows:

Capital receipts: The term ‘capital’ that such receipts are do not arise due to operating activities, hence not shown in the Profit and loss statement. These are the money received by a business when they sell any asset or undertake any liability. These receipts do not arise in a recurring manner in a business. They don’t affect the profit or loss of the business. They are not essential for the survival of the business.

Examples of capital receipts are as follows:

I have given a table below for more understanding:

See less