A cash flow statement is a statement showing the inflow and outflow of cash and cash equivalents during a financial year. Cash Flow Statements along with Income statements and Balance Sheet are the most important financial statements for a company. The Cash Flow Statement provides a picture to the sRead more

A cash flow statement is a statement showing the inflow and outflow of cash and cash equivalents during a financial year. Cash Flow Statements along with Income statements and Balance Sheet are the most important financial statements for a company.

The Cash Flow Statement provides a picture to the shareholders, government, and the public of how the company manages its obligations and fund its operations. It is a crucial measure to determine the financial health of a company.

The Cash Flow Statement is created from the Income Statement and the Balance Sheet. While Income Statement shows money engaged in various transactions during the year, the Balance Sheet presents information about the opening and closing balances.

The primary objective of a Cash Flow Statement is to present a record of inflow and outflow of cash, cash equivalents, and marketable securities through various activities of a company.

Various activities in a company can be broadly classified into three parts or heads:

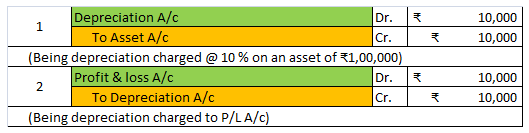

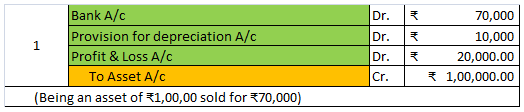

- Cash Flow from Operating Activities: it represents how money from regular business activities is derived and spent. It includes Net Profit from Income Statement after adjusting for tax and extra-ordinary activities. Items included in Operating Activities are adjustments in Working Capital. If current liabilities are paid or current assets are bought it means outflow of cash, hence it is deducted and if liabilities are increased or assets are sold it means the inflow of cash, hence it is added. Operating Activities take into account taxation, dividend, depreciation, and other adjustments.

- Cash Flow from Investing Activities: it represents aggregate inflow or outflow of cash due to various investments activities that the company was engaged in. Purchase and sale of non-current assets like fixed assets and long-term investments are considered under this head. If there is an investment made, it means outflow of cash, hence it is deducted and if there is an investment sold it means the inflow of cash, and hence it is added.

- Cash Flow from Financing Activities: it represents the activities that are used to finance a company’s operations, like, issue of cash or debentures, paying dividends and interest, long-term borrowing taken by a company, etc. If these are paid, it means outflow of cash and is hence deducted and if they are acquired, it means the inflow of cash and hence ae added.

Cash Flow Statements also present a picture of the liquidity of the company and are therefore used by the management of a company to take decisions with the help of the right information.

Cash Flow Statements are a great source of comparison between a company’s last year’s performance to its current year or with other companies in the same industry and hence, helps shareholders and potential investors to make the right decisions.

It also helps to differentiate between non-cash and cash items; incomes and expenditures are divided into separate heads.

See less

No, the building is not a current asset. Explanation Current assets are those in a business that is reasonably expected to be sold, consumed, cashed, or exhausted within one year of accounting through normal day-to-day business operations. Examples: Cash and cash equivalent, stock, liquid assets, etRead more

No, the building is not a current asset.

Explanation

Current assets are those in a business that is reasonably expected to be sold, consumed, cashed, or exhausted within one year of accounting through normal day-to-day business operations.

Examples: Cash and cash equivalent, stock, liquid assets, etc.

The building is expected to have a valuable life for more than a year and is bought for a longer term by a company. The building is a fixed asset/non-current asset, those assets which are bought by the company for a long term and aren’t supposed to be consumed within just one accounting year.

In order to understand it more clearly, let’s see the two types of assets in the classification of the assets on the basis of convertibility:

In the classification of the assets on the basis of their convertibility, they are classified either as current assets or fixed assets. Also referred to as current assets/ non-current assets or short-term/ long-term assets.

Building in the balance sheet

Let us take a look at the balance sheet’s asset side and see where building and current assets are shown

Balance Sheet (for the year ending…)

As we can see, the building is shown on the long-term assets side and not in the current assets.

Therefore, the building is not a current asset.

See less