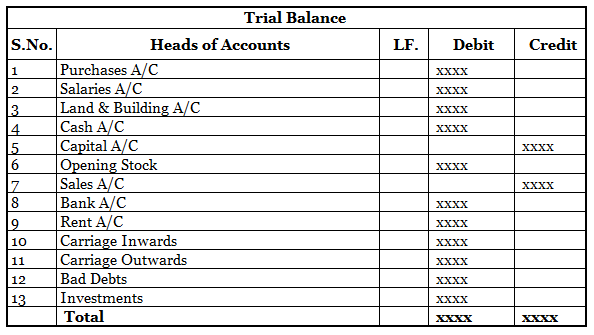

The difference between a ledger & a trial balance is as follows: Basis Ledger Trial Balance Meaning Ledger is a book/register in which all the accounts are put together. A Trial Balance is a statement showing the debit and credit balance of all the accounts to ascertain the arithmetical accuracyRead more

The difference between a ledger & a trial balance is as follows:

| Basis | Ledger | Trial Balance |

| Meaning | Ledger is a book/register in which all the accounts are put together. | A Trial Balance is a statement showing the debit and credit balance of all the accounts to ascertain the arithmetical accuracy of the books of accounts. |

| Basis of preparation | Journal is the basis for recording transactions in the ledger. | The closing balances of different accounts in the ledger are the basis for preparing the trial balance. |

| Objective | It is prepared to see the net effect of various transactions affecting a particular account. | It is prepared to check the arithmetical accuracy of the books of accounts. |

| Format | A ledger has four identical columns on the debit and credit sides: 1. Date, 2. Particulars, 3. Journal Folio, 4. Amount. | A Trial Balance has five columns: 1. S.No, 2. Name of Accounts, 3. Ledger Folio, 4. Debit Balance, 5. Credit Balance. |

| Stage of Recording | A ledger is prepared after recording the transactions in the journal. | A trial balance is prepared after posting the transactions in the ledger. |

The term ‘contra’ means 'opposite'. Therefore, a contra revenue account is an account that is opposite of the revenue accounts of a business i.e. sales account. It has the opposite balance of the revenue account i.e. debit balance. The purpose of the contra revenue account is to ascertain the actuaRead more

The term ‘contra’ means ‘opposite’. Therefore, a contra revenue account is an account that is opposite of the revenue accounts of a business i.e. sales account. It has the opposite balance of the revenue account i.e. debit balance.

The purpose of the contra revenue account is to ascertain the actual amount of sales and record the items which have reduced the sales.

These are the contra revenue accounts commonly seen in businesses:

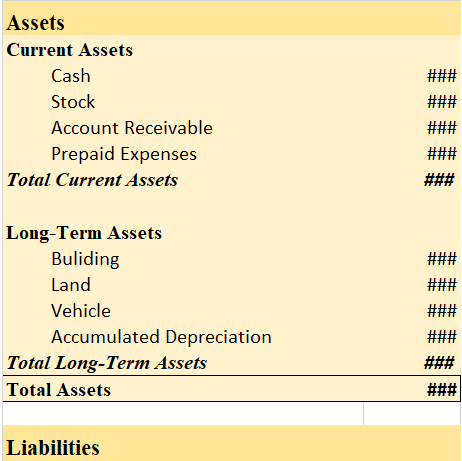

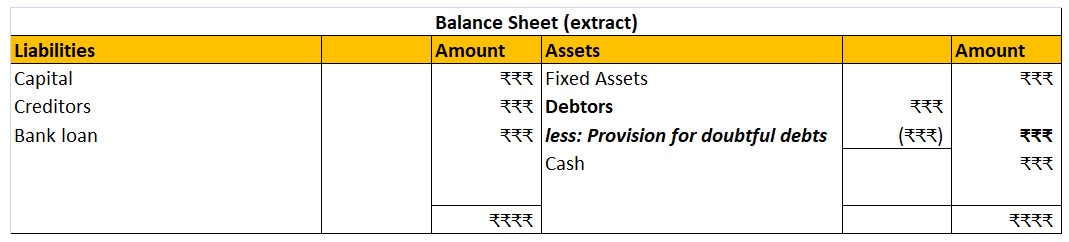

The total sales return is deducted from the sales in the balance sheet. Though being opposite of the sales account, the sale return account is not an expense account. It is considered an indirect loss as it reduces sales.

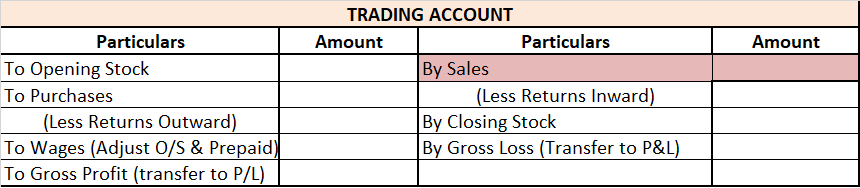

Sales discount is an expense hence it is debited to the profit and loss account.

Sales returns and sales discounts are shown in the trading and profit and loss account in the following manner:

See less