Depletion Amortization Depression

The term ‘contra’ means 'opposite'. Therefore, a contra revenue account is an account that is opposite of the revenue accounts of a business i.e. sales account. It has the opposite balance of the revenue account i.e. debit balance. The purpose of the contra revenue account is to ascertain the actuaRead more

The term ‘contra’ means ‘opposite’. Therefore, a contra revenue account is an account that is opposite of the revenue accounts of a business i.e. sales account. It has the opposite balance of the revenue account i.e. debit balance.

The purpose of the contra revenue account is to ascertain the actual amount of sales and record the items which have reduced the sales.

These are the contra revenue accounts commonly seen in businesses:

- Sales return account: This account records the amount of goods sold returned by customers. The journal entry for recording sale return is as follow:

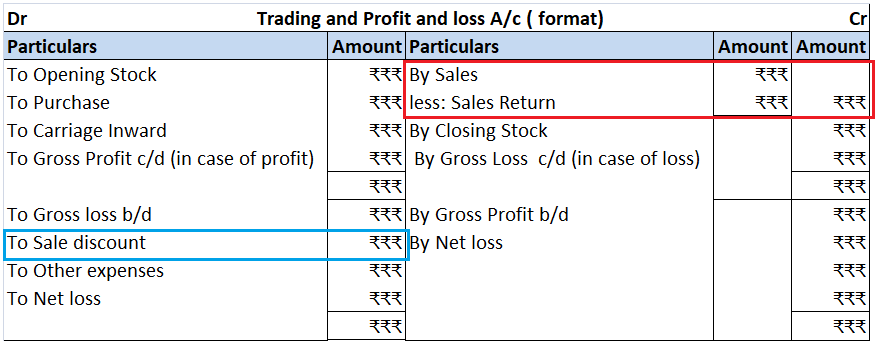

The total sales return is deducted from the sales in the balance sheet. Though being opposite of the sales account, the sale return account is not an expense account. It is considered an indirect loss as it reduces sales.

- Sale Discount account: This account records the amount of discount allowed to customers. The journal entry for recording sale discounts is as follows:

Sales discount is an expense hence it is debited to the profit and loss account.

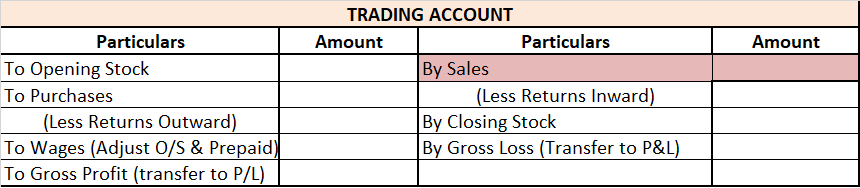

Sales returns and sales discounts are shown in the trading and profit and loss account in the following manner:

The correct option is 2. Amortization. Depreciation in spirit is similar to Amortization because both depreciation and amortization have the same characteristics except that depreciation is used for tangible assets and amortization for intangible assets. To make it clear, intangible assets are thoseRead more

The correct option is 2. Amortization.

Depreciation in spirit is similar to Amortization because both depreciation and amortization have the same characteristics except that depreciation is used for tangible assets and amortization for intangible assets.

To make it clear, intangible assets are those assets that cannot be touched i.e. they are not physically present. For example, goodwill, patent, trademark, etc. Hence, these assets are amortized over their useful life and not depreciated.

Example for Amortizing intangible assets: A manufacturing company buys a patent for Rs 80,000 for 8 years. Assuming that the residual value of the patent after 8 years to be zero.

The depreciation to be written off will be

Yearly Depreciation = Cost of the patent – Residual value / Expected life of the asset.

= 80,000 – 0 / 8

= Rs 10,000 every year.

Whereas, tangible assets are those assets that can be touched i.e. they are physically present. For example, building, plant & machinery, furniture, etc. Hence, these assets are depreciated over their useful life and not amortized.

Example of Depreciating tangible asset: A manufacturing company bought machinery for Rs 8,10,000 and its estimated life is 8 years, scrap value being Rs 10,000.

The depreciation to be written off will be

Yearly Depreciation = Cost of machinery – Scrap value / Expected life of the asset.

= 8,10,000 – 10,000 / 8

= 8,00,000 / 8

= Rs 1,00,000 every year.

See less