Journal Entry for Interest on Drawings is- Particulars Amount Amount Drawings A/c Dr $$$ To Interest on Drawings A/c $$$ So as per the modern approach: From the point of view of business, Interest on Drawings is an Income. When there is an inRead more

Journal Entry for Interest on Drawings is-

| Particulars | Amount | Amount |

| Drawings A/c Dr | $$$ | |

| To Interest on Drawings A/c | $$$ |

So as per the modern approach: From the point of view of business, Interest on Drawings is an Income.

- When there is an increase in the Income, it is credited.

- When there is a decrease in the Income, it is debited.

From the point of view of the proprietor, Interest on Drawings is a Liability.

So as per the modern approach:

- When there is an increase in the Liability, it is credited.

- When there is a decrease in the Liability, it is debited.

So as per the modern approach, Interest on Drawings is credited because with Interest the income increases for the business. Whereas, the amount of such interest is a loss from the point of view of the owner/ Proprietor, as such the amount of drawings is increased by the amount of interest and hence the Drawings account is debited.

For Example, Harry charged interest on drawings on Rs 10,000 @ 12% for one year.

Explanation:

Step 1: To identify the account heads.

In this transaction, two accounts are involved, i.e. Drawings A/c and Interest on Drawings A/c.

Step 2: To Classify the account heads.

According to the modern approach: From the point of view of business, Interest on Drawings is a Revenue A/c and Drawings A/c is an Expense A/c.

Step 3: Application of Rules for Debit and Credit:

According to the modern approach: As Revenue increases because of interest on drawings received by the business, Interest on Drawings A/c will be Credited. (Rule – increase in Revenue is credited).

Drawings A/c is an expense account for the business and as expense increases, Drawings A/c will be debited. (Rule – increase in the expenses is debited).

So from the above explanation, the Journal Entry will be-

| Particulars | Amount | Amount |

| Drawings A/c Dr | 1,200 | |

| To Interest on Drawings A/c | 1,200 |

See less

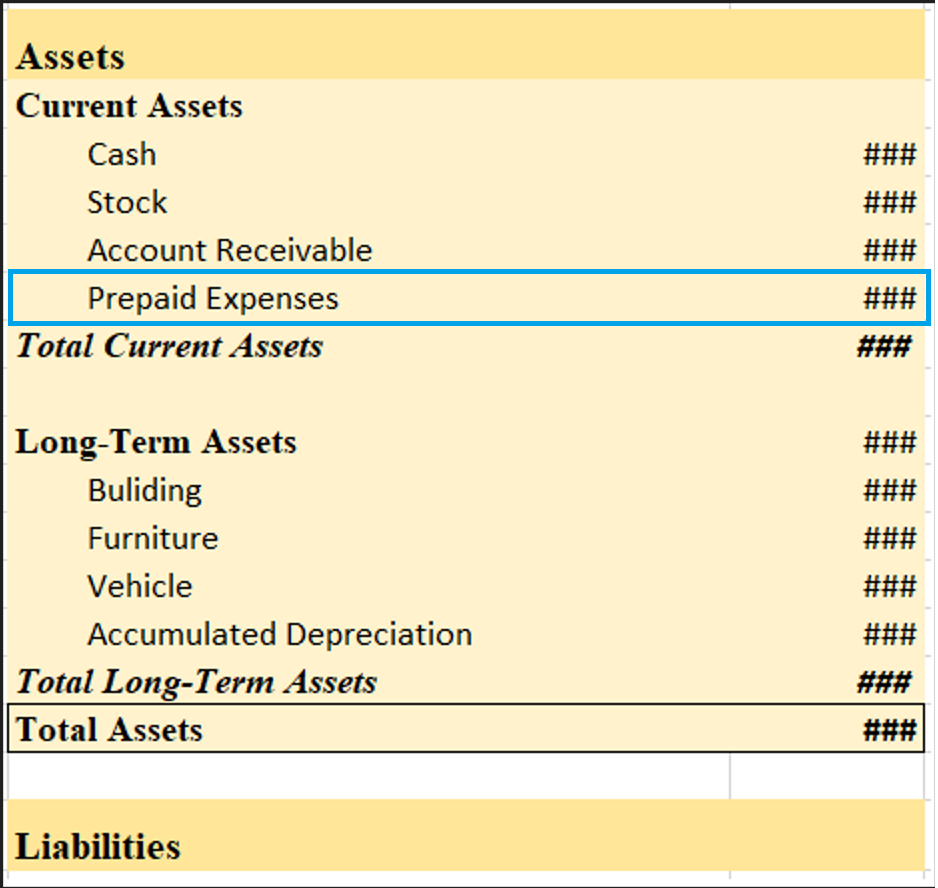

Land in the balance sheet The land is an asset and hence it is shown on the asset side of the balance sheet. On the asset side of the balance sheet, the land is stated under the heading long-term assets. Balance Sheet (for the year…) Explanation The land is a fixed asset and is supposed not to be caRead more

Land in the balance sheet

The land is an asset and hence it is shown on the asset side of the balance sheet.

On the asset side of the balance sheet, the land is stated under the heading long-term assets.

Balance Sheet (for the year…)

Explanation

The land is a fixed asset and is supposed not to be cashed, consumed, last, sold, or written off within one accounting year and is purchased for long-term use. The fixed assets are also called non-current assets and the reason behind it is that current assets are easily converted into cash within one year and they are not.

Why is it shown on the asset side?

The land is an asset, although it is not depreciable it is still considered to be an asset because just like other assets the business spends its own money to acquire it, and it gives them a long-term benefit while reselling it.

Therefore, the land is shown on the asset side under the fixed asset heading.

See less