Yes, Capital Work in Progress is Tangible Asset. To attain an understanding of the same, we first need to understand what are tangible assets. Assets that have a physical existence, that is they can be seen, touched are called Tangible Assets. Capital work in progress is the cost incurred on fixed aRead more

Yes, Capital Work in Progress is Tangible Asset.

To attain an understanding of the same, we first need to understand what are tangible assets. Assets that have a physical existence, that is they can be seen, touched are called Tangible Assets.

Capital work in progress is the cost incurred on fixed assets that are under construction as on the balance sheet date. Since the asset cannot be used for operation it cannot be classified as a Fixed Asset.

For example:

If an asset takes 1.5 years to be constructed as on 1.4.2020 then on the balance sheet date 31.3.2021, the cost incurred on the asset will be classified as Capital Work in Progress.

Common examples of Capital Work in Progress include immovable assets like Plant and Machinery, Buildings.

It is shown under the head Non-Current Assets in the balance sheet. Examples of cost included in Capital Work in Progress can be:

- Advance payment to the contractor

- Material used/purchased

- Cost of labor incurred, etc.

Since the assets under the head Capital Work in Progress are in the process of completion and not completed, hence they are not depreciable until completed. Once the asset is completed it is moved under the head Fixed Assets.

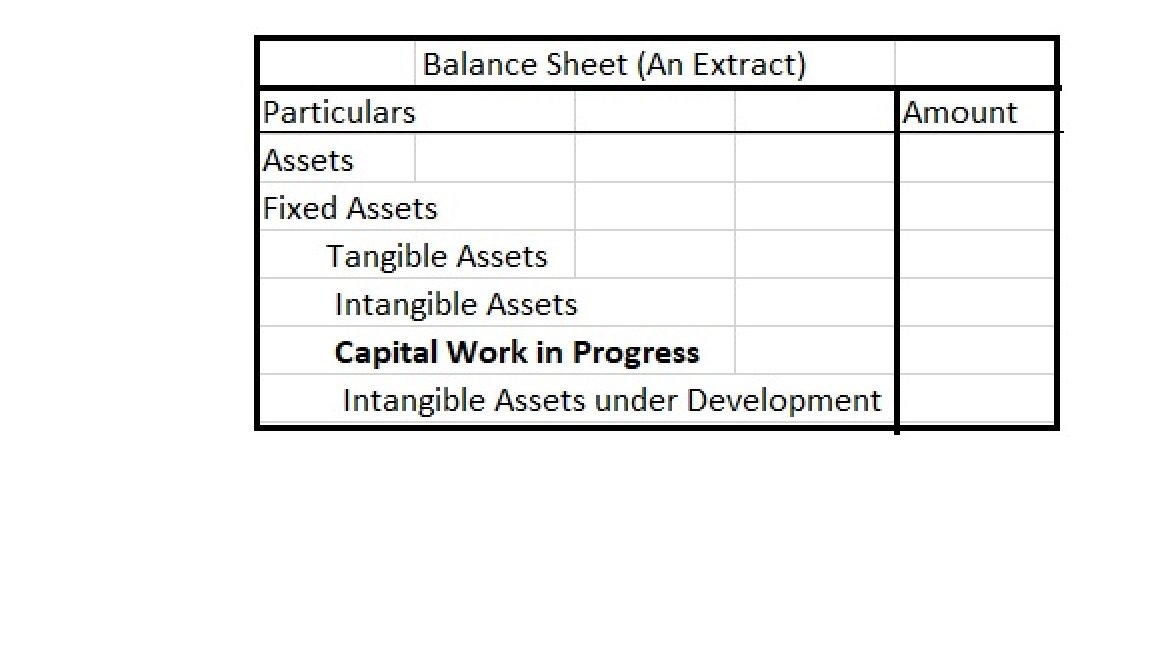

Capital Work in Progress is shown in the Balance Sheet as:

Accumulated profit is the amount of profit left after the payment of dividends to the shareholders. It is also known as retained earnings. It is the profit that is not distributed as dividends to shareholders, hence called retained earnings. This accumulated profit is an important source of internalRead more

Accumulated profit is the amount of profit left after the payment of dividends to the shareholders. It is also known as retained earnings. It is the profit that is not distributed as dividends to shareholders, hence called retained earnings. This accumulated profit is an important source of internal finance for a company. Accumulated profit or retained earnings can be ascertained using the following formula:

Accumulated profit = Opening balance of accumulated profit + Net Profit/Loss (loss being in the negative figure) – Dividend paid

Accumulated profit can be put to the following uses:

Accumulated profit and reserves are often considered the same. But in substance, they are not. The reserves are actually part of the accumulated profit, but the converse is not true. They are created by transferring amounts from the accumulated profit. While reserves are created for purpose of strengthening the financial foundation of a firm, the accumulated profit’s main purpose is to make reinvest in the business to increase its growth.

The amount of accumulated profits depends upon the retention ratio and dividend payout ratio of a company. The retention ratio is the opposite of the dividend payout ratio.

The formula of dividend pay-out ratio = Dividend payable/Net Income

And retention ratio = 1 – (Dividend payable/Net Income)

If the retention ratio is more than the dividend payout ratio, the accumulated profit remains positive.

See less