The profits earned by a company are distributed to its shareholders monthly, quarterly, half-yearly, or yearly in the form of dividends. The dividend payable by the company is transferred to the Dividend Account and is then claimed by the shareholders. If the dividend is not claimed by the members aRead more

The profits earned by a company are distributed to its shareholders monthly, quarterly, half-yearly, or yearly in the form of dividends. The dividend payable by the company is transferred to the Dividend Account and is then claimed by the shareholders.

If the dividend is not claimed by the members after transferring it to the Dividend Account, it is called Unclaimed Dividend. Such a dividend is a liability for the company and it is shown under the head Current Liabilities.

The dividend is transferred from the Dividend Account to the Unclaimed Dividend Account if it is not claimed by the shareholders within 37 days of declaration of dividend.

For the Cash Flow Statement, unclaimed dividend comes under the head Financing Activities.

Items shown under the head Financing Activities are those that are used to finance the operations of the company. Since, money raised through the issue of shares finances the company, any item related to shareholding or dividend is shown under the head Financing Activities.

However, there are two approaches to deal with the treatment of Unclaimed Dividend:

First, since there is no inflow or outflow of cash, there is no need to show it in the cash flow statement.

Second, the unclaimed dividend is deducted from the Appropriations, that is, when Net Profit before Tax and Extraordinary Activities is calculated.

Then, it is added under the head Financing Activities because the amount of dividend that has to flow out of the company (that is Dividend Paid amount which has already been deducted from Financing Activities) remained in the company only since it has not been claimed by the members.

The second approach to the treatment of an Unclaimed Dividend is used when the company has not transferred the unclaimed dividend amount from the Dividend Account to a separate account.

See less

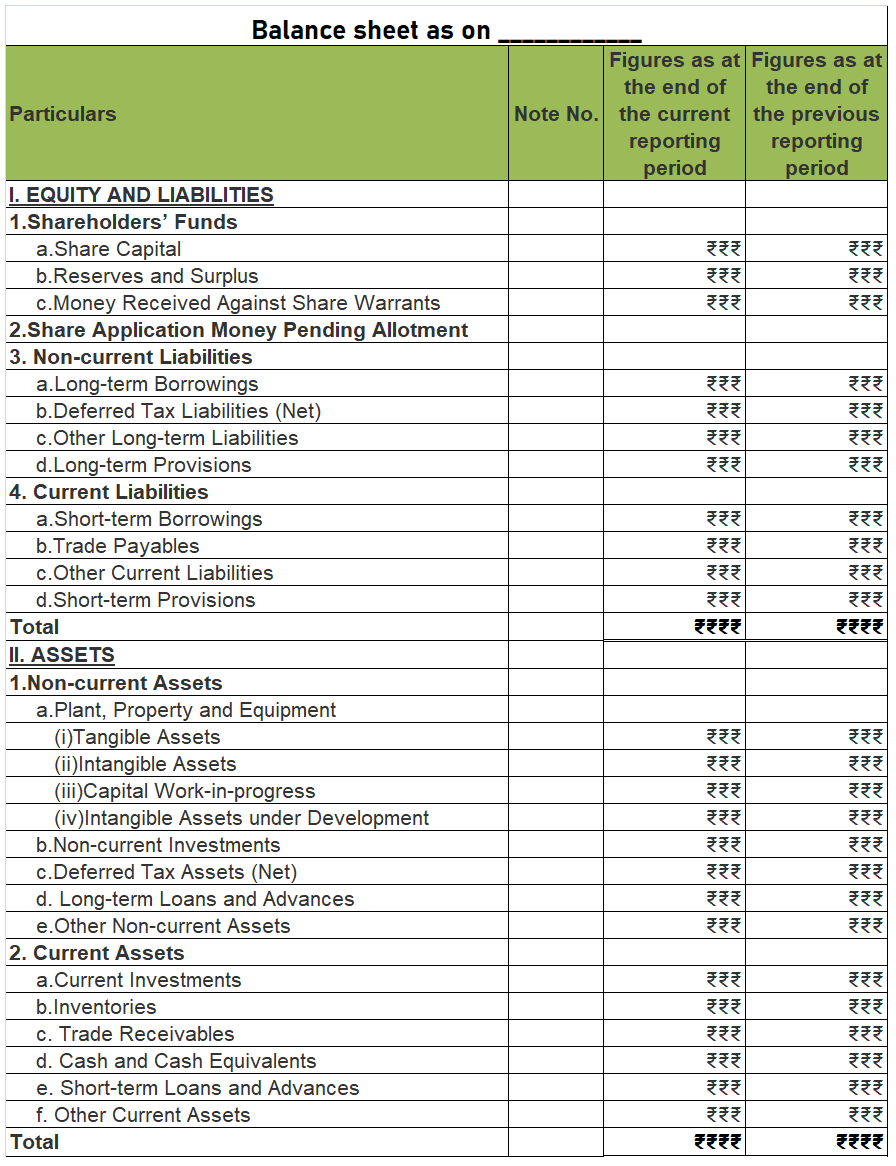

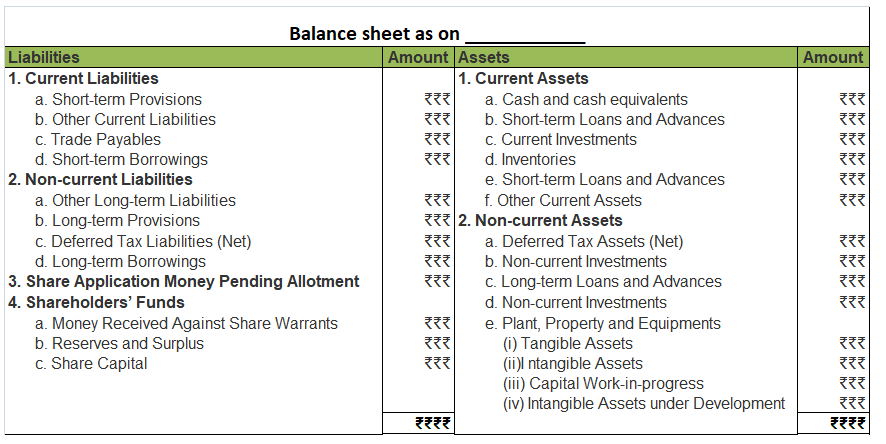

A balance sheet of a company is a financial statement that depicts the assets, liabilities and shareholders’ equity of the company at a point of time, usually at the end of the accounting year. A balance sheet of a company is reported in a vertical format which is different from that of a partnershiRead more

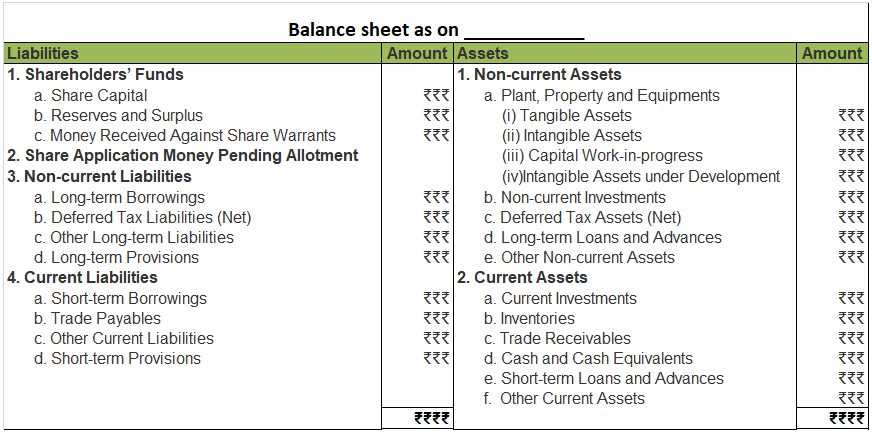

A balance sheet of a company is a financial statement that depicts the assets, liabilities and shareholders’ equity of the company at a point of time, usually at the end of the accounting year. A balance sheet of a company is reported in a vertical format which is different from that of a partnership where the horizontal format is used.

COMPONENTS OF A BALANCE SHEET

The three main components of a balance sheet are Assets, Liabilities and Shareholders’ equity.

FORMAT OF BALANCE SHEET

As per the Companies Act 2013, the following format should be used for preparing a balance sheet.

From the above Balance sheet, we should get:

Assets = Liabilities + Shareholders’ Equity

Relevant notes for each component should also be prepared when necessary.

See less