The correct option is (b) and (d) As the internal analysis is done for the internal assessment of the firm, only those persons can carry out the assessment who has access to the internal accounting records of a business firm. As the owners or managers are the members of the top-level management execRead more

The correct option is (b) and (d)

As the internal analysis is done for the internal assessment of the firm, only those persons can carry out the assessment who has access to the internal accounting records of a business firm. As the owners or managers are the members of the top-level management executives they can carry out the work of internal analysis. Also, the government agencies can carry out internal analysis as they have been given the statutory powers of doing such works.

To make it clear, let me explain a little about internal analysis-

To determine the profitability of various activities and operations or to know the performance of the business concern, the top-level executives along with the management accountant carry out an internal assessment of the financial statements within the concern, this process is known as internal analysis.

See less

What is net credit sales? Net credit sales are those revenues by a business entity, less all sales returns and allowances. Immediate payment in cash is not included in net credit sales. Formula The formula for net credit sales is as follows: Net credit sales = Sales on credit - Sales returns - SalRead more

What is net credit sales?

Net credit sales are those revenues by a business entity, less all sales returns and allowances. Immediate payment in cash is not included in net credit sales.

Formula

The formula for net credit sales is as follows:

Net credit sales = Sales on credit – Sales returns – Sales allowances

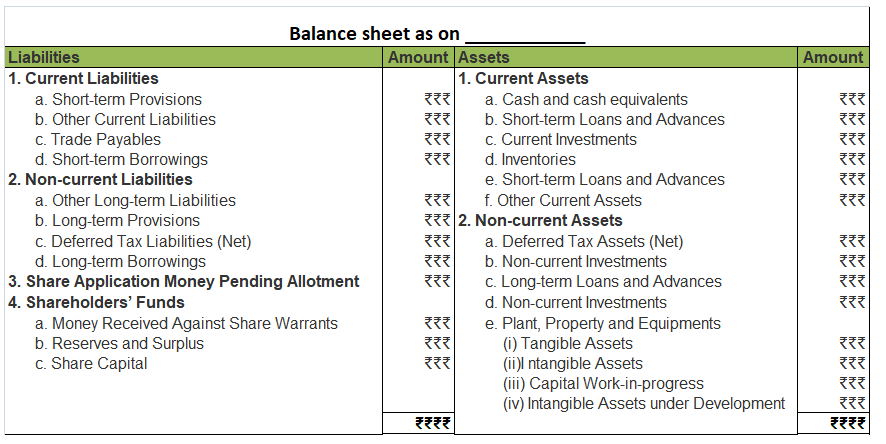

In the balance sheet, you can find credit sales in the “short-term assets “section. It can be calculated from account receivables, bills receivables, and debtors of the balance sheet.

Credit sales = closing debtors + receipts – opening debtors

Steps to calculate net credit sales

Terms relevant to understand before calculation

Sales return: A sales return is when a customer or client returns or sends a product back to the seller. And this can happen due to various reasons, including:

Sales allowance: A sales allowance is a discount that a seller offers a buyer as an alternative to the buyer for returning the product.

Because of a problem or issue with the buyer’s order or we can say that he is not satisfied with the product.

Cash sales: Cash sales are sales in which the payment is done at once or I can say that buyer has obligation to make payment to the seller.

Cash sales are considered to include bills, checks, credit cards, and money orders as forms of payment.

Example

Now after understanding the terms used in the formula let me explain to you with an example which is as follows:-

Why do we need net credit sales?

- Net credit sale is also used to calculate other financial analysis items like days sales outstanding.

See less