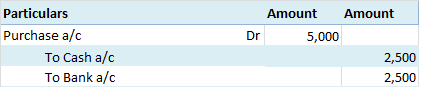

When in a single transaction two or more accounts are involved, such kinds of transactions are termed as Compound entries. Example 1, Johnson Co. purchased goods worth 5,000, and half of the amount was paid in cash and the other half by cheque. So here three accounts are involved: Purchase account-Read more

When in a single transaction two or more accounts are involved, such kinds of transactions are termed as Compound entries.

Example 1, Johnson Co. purchased goods worth 5,000, and half of the amount was paid in cash and the other half by cheque.

So here three accounts are involved:

Purchase account- That is to be debited.

Cash account- That is to be credited.

Bank account- That is to be credited.

Journal entry:

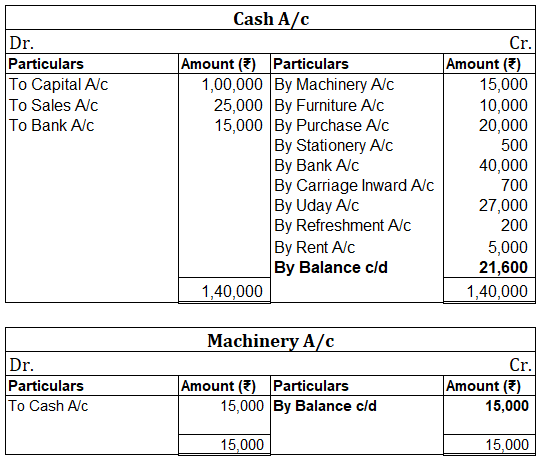

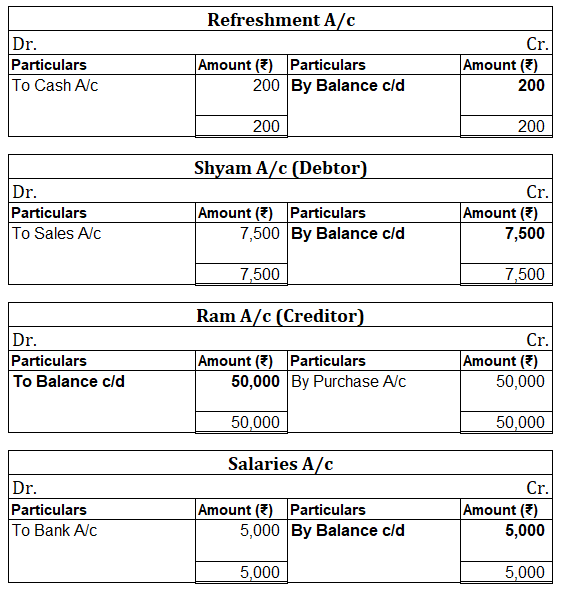

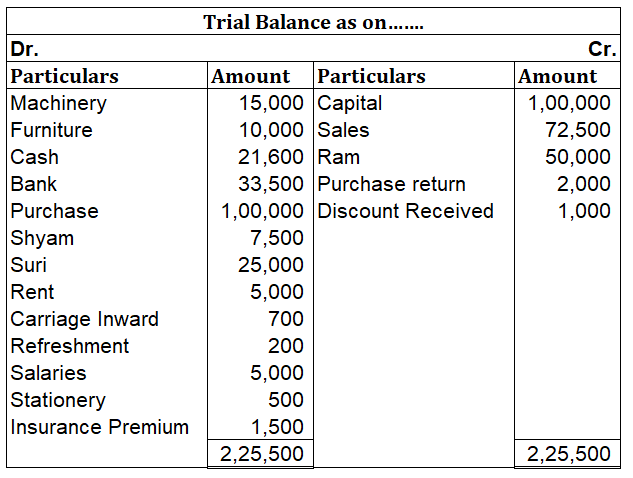

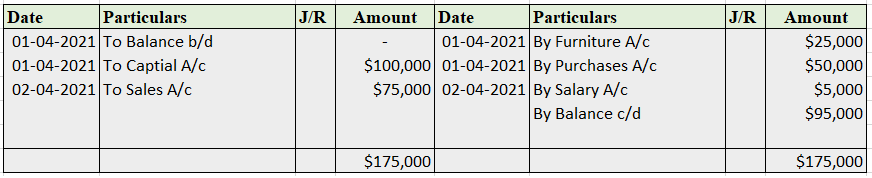

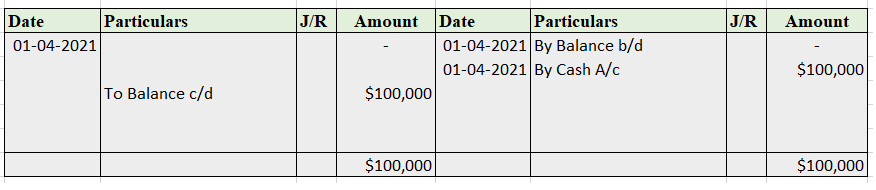

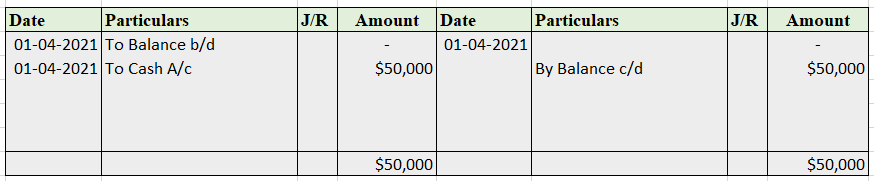

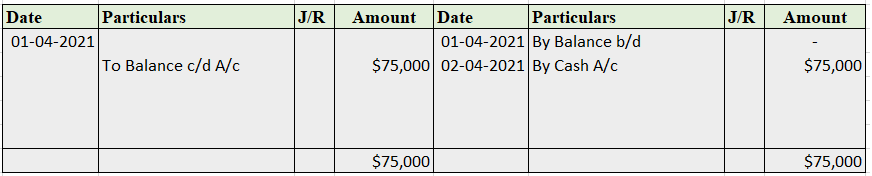

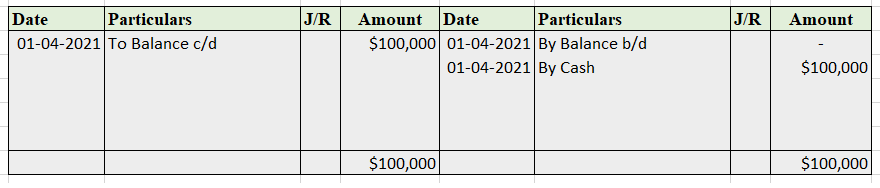

Now posting the above journal entry in a ledger account.

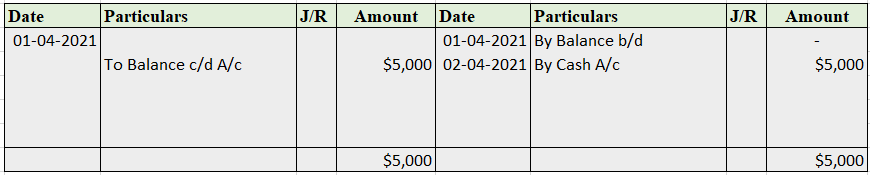

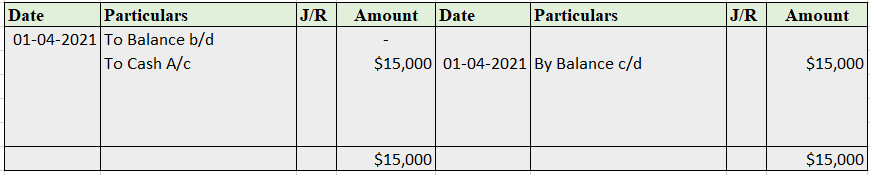

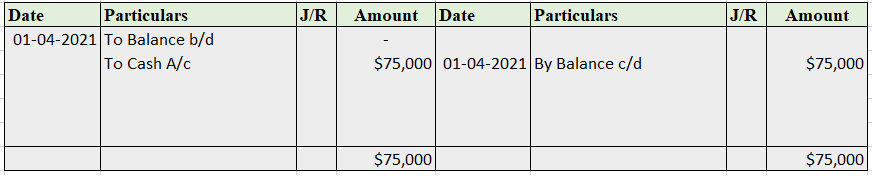

In the Journal, the Purchase account has been debited. So in the ledger, the purchase account will also be debited. Since the purchase account is debited in the ledger, the corresponding two credit accounts of this entry i.e. the cash and the bank will be written on the debit side in the particulars column. So while posting, the amount to be considered would be the amount individually paid in cash and bank as shown in the journal entry.

Cash a/c is credited with the purchase account. In the ledger, purchase a/c will be posted on the credit side. So while posting, the amount to be considered would be the amount individually paid in cash.

Bank a/c is credited with the purchase account. In the ledger, purchase a/c will be posted on the credit side. So while posting, the amount to be considered would be the amount individually paid in Bank a/c.

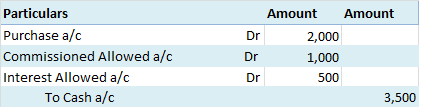

Example 2, Johnson Co purchased goods and made payment in cash 2,000. Along with it, it also paid commission and interest of 1,000 and 500 respectively.

So here four accounts are involved:

Purchase account- That is to be debited.

The commission allowed account- That is to be debited.

Interest allowed account- That is to be debited.

Cash account- That is to be credited.

Journal Entry:

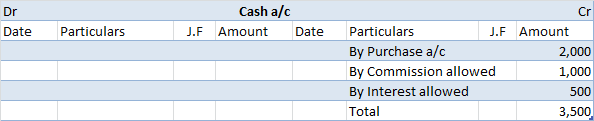

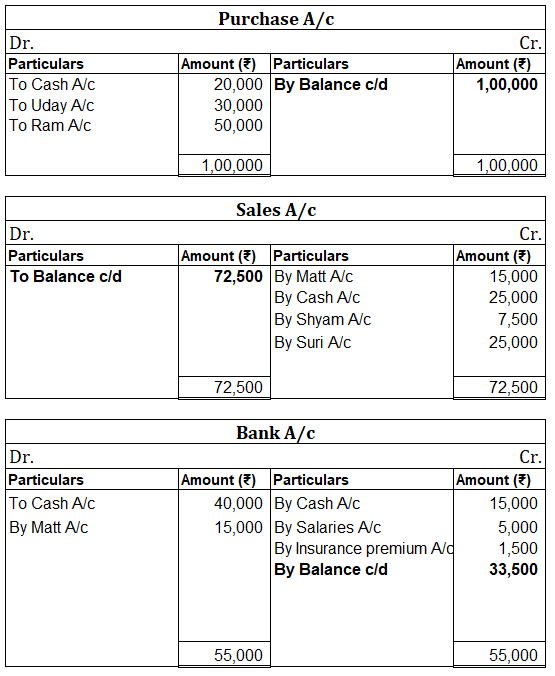

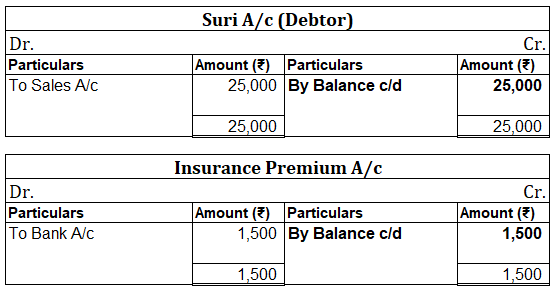

Now posting the above journal entry in a ledger account.

In the journal entry, the cash account has been credited. So in the ledger, the cash account will also be credited. Since the cash account is credited in the ledger, the corresponding three accounts will also be credited in the particulars column. As in the journal entry the three debit accounts viz. Purchase, the commission allowed, and interest allowed, the amounts written against them shall be entered in the respective accounts in the amount column on the credit side of the cash account.

Purchase a/c is debited with a cash account. In the ledger, Cash a/c will be posted on the debit side. So while posting, the amount to be considered would be the amount individually paid in the Purchase account.

The commission allowed a/c is debited with a cash account. In the ledger, cash a/c will be posted on the debit side. So while posting, the amount to be considered would be the amount individually paid in Commission allowed a/c.

Interest allowed a/c is debited with a cash account. In the ledger, cash a/c will be posted on the debit side. So while posting, the amount to be considered would be the amount individually paid in Interest allowed a/c.

See less

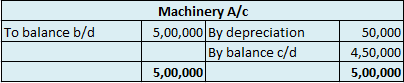

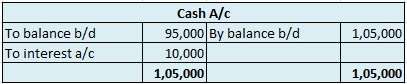

Debit balance means excess of credit side over debit side. For Example- At the beginning of the year the debit balance of trade receivables is 3,000 and there is a decrease(credit) of trade receivables of 1,000 during the year and an increase(debit) of trade receivables of 4,000 then at the end therRead more

Debit balance means excess of credit side over debit side.

For Example- At the beginning of the year the debit balance of trade receivables is 3,000 and there is a decrease(credit) of trade receivables of 1,000 during the year and an increase(debit) of trade receivables of 4,000 then at the end there will be a debit balance of 6,000 of trade receivables at the end

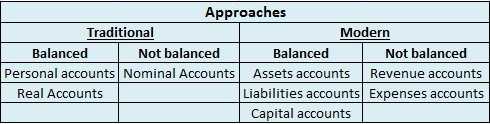

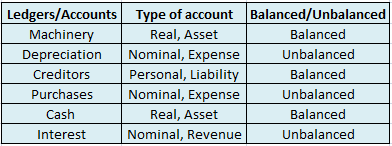

A Debit balance basically signifies all expenses and losses and all positive balances of assets. The debit balance increases when any asset increases and decreases when any asset decreases.

Assets

All the assets that appear in the balance sheet always have a debit balance. The debit balance under it will increase as it debits. Some of these assets can be illustrated below -:

Expenses and Losses

All expenses that appear on the debit side of the P&L account have a debit balance in their accounts.

For eg-: A rent of 10,000 is given to the landlord under which the work has been done by the entity.

For eg-: A depreciation of 10% is there on an asset of 12,000 will result in a debit balance under depreciation in the P&L Account.

Some of the following expenses can be illustrated below

So after seeing all the above points we can conclude that the debit balance includes all the expenses that are in the P&L account and all the assets that are there in the Balance sheet. So its balance increases when there is an increase in its account.

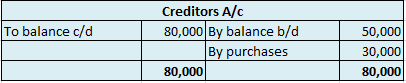

CREDIT BALANCE

Credit balance means excess of credit side over debit side.

For example, At the beginning of the year, the credit balance of trade payable is 3,000 and there is a debit of trade payable of 1,000 during the year and an increase(credit) of trade payable of 4,000 then at end there will be a credit balance of 6,000 for trade payable at the end

.A Credit balance signifies all income and gains and all liabilities and capital that is there in business.

Liabilities

Income and Gains

See less