Before answering your question directly, let’s first understand the two terms, ‘Rent Outstanding’ and ‘Accounting Equation’. Accounting Equation Accounting Equation depicts the relationship between the following items of a business: Assets, Liabilities and Owner’s Equity ( Capital ) It is a simple fRead more

Before answering your question directly, let’s first understand the two terms, ‘Rent Outstanding’ and ‘Accounting Equation’.

Accounting Equation

Accounting Equation depicts the relationship between the following items of a business:

- Assets,

- Liabilities and

- Owner’s Equity ( Capital )

It is a simple formula that implies that the total assets of a business are always equal to the sum of its liabilities and Owner’s Equity (Capital).

ASSETS = LIABILITIES + CAPITAL OR A = L + E

It is also known as the balance sheet equation.

This equation always holds good due to the double-entry system of accounting i.e. every event has a dual effect on items of the balance sheet.

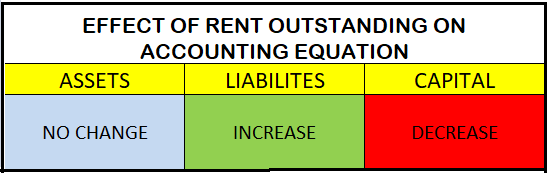

Outstanding Rent

We know rent is an expense for a business and rent outstanding means that rent is due, not paid which implies it is a liability which the business has to settle.

Hence Rent Outstanding is subtracted from the capital balance and added to liabilities.

Let’s take an example to see how rent outstanding affects the accounting equation. Suppose a business has the following figures:

Assets – Rs: 3,00,000

Capital – Rs: 2,00,000

Liabilities – Rs: 1,00,000

Assets = Liabilities + Capital

3,00,000 = 1,00,000 + 2,00,000

Now if Rent outstanding of Rs: 20,000 arises, this will happen:-

Assets – Rs: 3,00,000

Capital – Rs: 2,00,000 – Rs: 20,000 = Rs: 2,80,000

Liabilities – Rs: 1,00,000 + Rs: 20,000 = Rs: 1,20,000

Assets = Liabilities + Capital

3,00,000 = 1,20,000 + 2,80,000.

Hence, when rent outstanding arises, it increases the liability and decreases the Capital by the same amount. Therefore both the sides tally and the accounting equations holds good.

Rent Outstanding is shown on the liabilities side of the balance sheet. Also, the rent outstanding of the current year is shown in the debit side profit and loss account and we know the balance of the P/L account if profit, is added to Capital and in case of loss it is subtracted from Capital. Hence, the rent outstanding is subtracted from the capital.

I hope my answer was useful to you.

See less

Negative working capital means the excess of current liabilities over current assets in an enterprise. Let’s understand what working capital is to get more clarity about negative working capital. Meaning of Working Capital Working Capital refers to the difference between current assets and current lRead more

Negative working capital means the excess of current liabilities over current assets in an enterprise.

Let’s understand what working capital is to get more clarity about negative working capital.

Meaning of Working Capital

Working Capital refers to the difference between current assets and current liabilities of a business.

Working Capital = Current Assets – Current Liabilities

It is the capital that an enterprise employs to run its daily operations. It indicates the short term liquidity or the capacity to pay off the current liabilities and pay for the daily operations.

Items under Current Assets and Current Liabilities

It is important to know about the items under current assets and current liabilities to understand the significance of working capital.

Current assets include cash and bank balance, accounts receivables, inventories, short term investments, prepaid expenses etc.

Current liabilities include accounts payable, short term loans, bank overdraft, interest on short term investment, outstanding salaries and wages etc.

Types of working capital

Since the working capital is just the difference between current assets and liabilities, the working capital can be one of the following:

Hence, negative working capital exists when current liabilities are more than current assets.

Implications of having negative working capital

Having negative working capital is not an ideal situation for an enterprise. Having negative working capital indicates that the enterprise is not in a position to pay off its current liabilities and there may be a cash crunch in the business.

An enterprise may have to finance its working capital requirements through long term finance sources if its working capital remains negative for quite a long time.

The ideal situation is to have current assets two times the current liabilities to maintain a good short term liquidity of the business i.e.

Current Assets = 2(Current Liabilities)

See less