Capital Work in Progress refers to the total cost incurred on a fixed asset that is still undergoing construction as on the balance sheet date. These costs are not allowed to be used as an operating asset until the asset is ready to use. Until the construction of the asset is completed, the costs arRead more

Capital Work in Progress refers to the total cost incurred on a fixed asset that is still undergoing construction as on the balance sheet date. These costs are not allowed to be used as an operating asset until the asset is ready to use. Until the construction of the asset is completed, the costs are recorded as capital work in progress.

Depreciation is the systematic allocation of the cost of an asset over its useful life. Depreciation is charged on an asset from the date it is ready to use. Since Capital Work in Progress is not yet ready to use, depreciation cannot be charged on it.

Example

If a company owns a Machinery worth Rs. 45,000 out of which Rs. 15,000 is part of capital work in progress, then depreciation on such machinery would be calculated only on the part of machinery that is ready to use that is Rs. 30,000 (45,000-15,000).

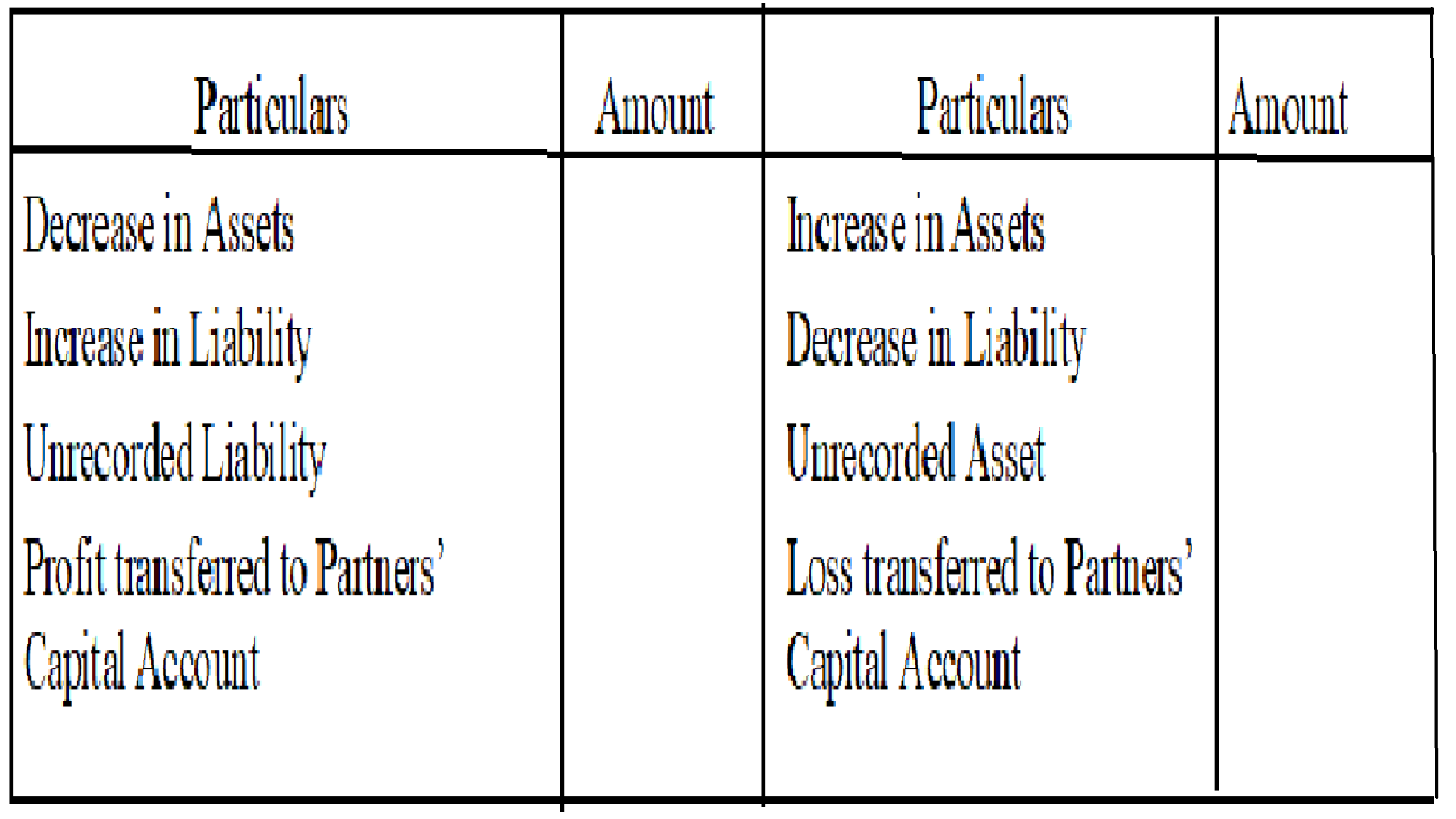

When an asset is undergoing construction, the journal entry for each expense would be recorded as

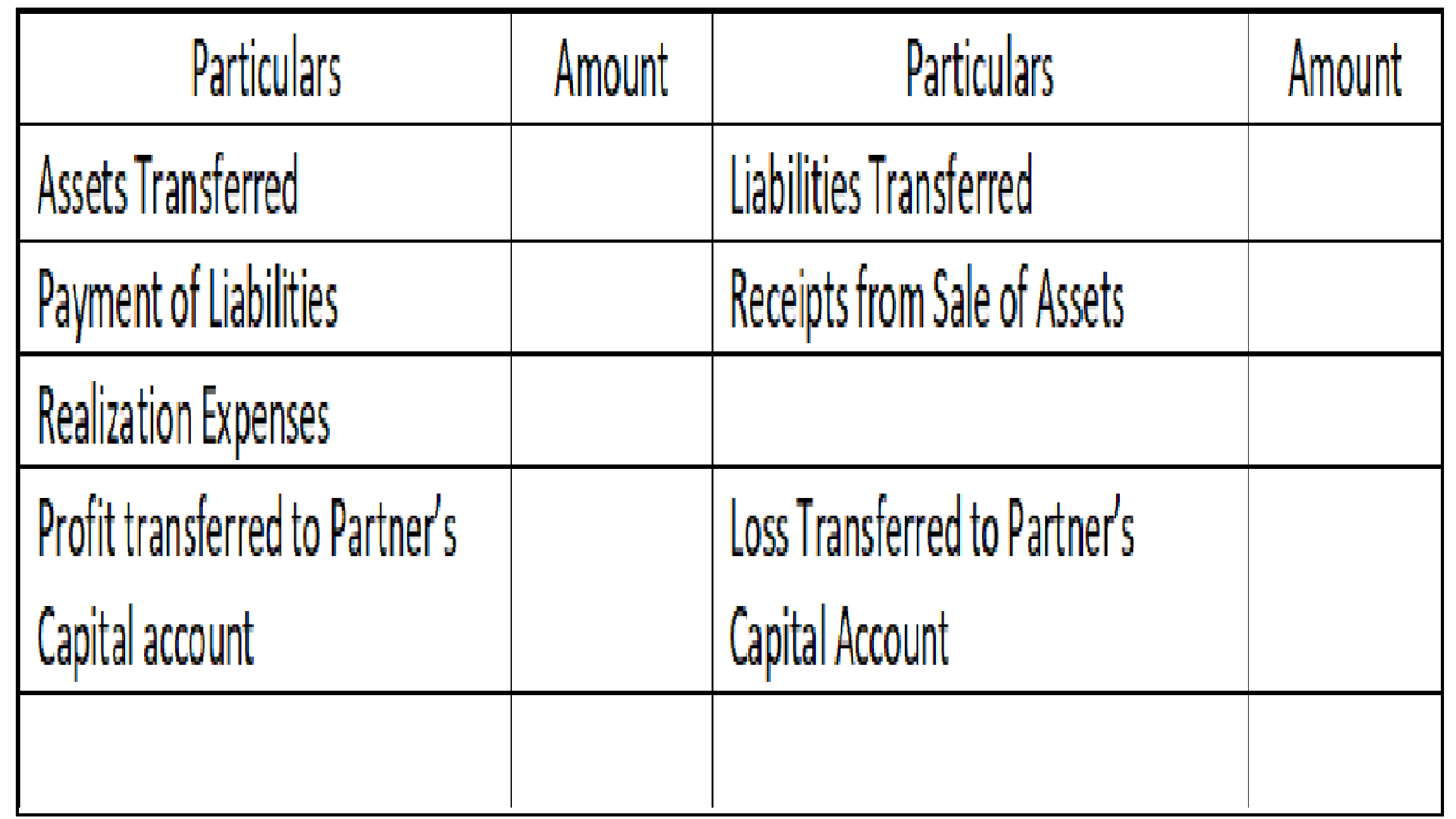

Further, when all construction of the above asset is completed, it is transferred to fixed asset account. This would be recorded as

After transfer to Fixed Asset account, depreciation can be calculated and shown as below

If the construction of an asset is complete but has not been put to use till now, depreciation is still calculated as it is ready for use. It can be done through various methods like straight-line method, written down value method etc.

See less

Revenue and income are two accounting terms that are often used interchangeably. However, it is important to understand that these two terms are different. Let us know the difference between the two through the discussion below: What is Revenue? Revenue is the total amount of a business's sales. ItRead more

Revenue and income are two accounting terms that are often used interchangeably. However, it is important to understand that these two terms are different. Let us know the difference between the two through the discussion below:

What is Revenue?

Revenue is the total amount of a business’s sales. It is the total amount earned by a business before deducting any expenses. Revenue is recognized in accounting as soon as a sale happens, even if the payment hasn’t been received yet.

For example, XYZ Ltd sold 100 pens at a selling price of 10 per pen. The total revenue of the business is hence 1,000.

What is Income?

Income is the amount earned by a business after deducting any direct or indirect expenses. It is the amount that is left after subtracting all expenses, taxes and other costs from Revenue.

Which is a broader term between the two?

Revenue is a broader term as it includes the total earnings a business generates before deducting any expenses. It includes all sales of goods or services during a specific period.

On the other hand, income is calculated after deducting certain expenses like taxes, interest, etc. This makes it more specific and refined than revenue.

Revenue provides a measure of a company’s ability to generate sales and income reflects the efficiency in managing costs and generating profits.

See less