A. Events B. Transactions C. Journals D. None of These

When a company issues shares to shareholders at a price over the face value (at a premium), that amount is termed as securities premium. This amount is transferred to what we call the securities premium reserve. The company is required to maintain a separate reserve for securities premium. UtilizatiRead more

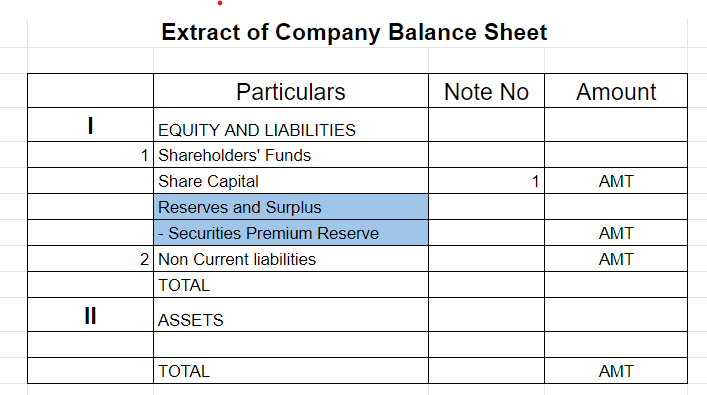

When a company issues shares to shareholders at a price over the face value (at a premium), that amount is termed as securities premium. This amount is transferred to what we call the securities premium reserve. The company is required to maintain a separate reserve for securities premium.

Utilization

Securities premium reserve can be used for the following reasons:

- Issue of fully paid Bonus share capital.

- To cover preliminary expenses of a company.

- For funding the buy-back of securities.

Since it is not a free reserve, it can only be used for a few specific purposes. The amount received as securities premium cannot be used to transfer dividends to shareholders

Treatment

When a company issues shares at a premium, the securities premium reserve account is credited along with share capital as an increase in capital is credited according to the modern rule of accounting.

For example,

Sonly Ltd. issues 1,000 shares of $10 face value at $15. Here, the amount of premium would be $5 (15 – 10) per share. Therefore, the journal entry would show:

Bank a/c (15 x 1,000) Dr 15,000

To Share Capital (10 x 10,000) 10,000

To Securities Premium Reserve a/c (5 x 10,000) 5,000

From the above example, we can see that the company receives $15,000, but transfers $10,000 to share capital and the excess $5,000 to securities premium reserve.

In the balance sheet, this securities premium reserve is shown under the title “Equity and Liabilities” under the head ‘‘Reserves and Surplus”.

The correct option is Option C: Journal Entries. Journal entries are the primary entries in the books of accounts and they are passed when any transaction or event takes place. Every journal entry has a dual effect i.e. two or more accounts are affected. For example, When cash is introduced in the bRead more

The correct option is Option C: Journal Entries.

Journal entries are the primary entries in the books of accounts and they are passed when any transaction or event takes place. Every journal entry has a dual effect i.e. two or more accounts are affected.

For example, When cash is introduced in the business, the journal entry passed is:

Cash A/c Dr. ₹10,000

To Capital A/c ₹10,000

The accounts affected here are Cash A/c and Capital A/c.

Cash A/c gets debited by ₹10,000,

and Capital A/c get credited by ₹10,000.

All the processes of accounting are conducted in an ordered manner known as the accounting cycle.

The first step in an accounting cycle is to identify the transactions and events which are monetary in nature.

The second step is to record the identified transactions in form of journal entries.

And the third step is to make postings in the general ledger accounts as per the journal entries.

Hence, the preparation of the ledger is the third step in the accounting cycle and is prepared from the journal entries.

See less