When a partnership firm consisting of some partners, decide to admit a new partner into their firm, they have to forego a part of their share for the new partner. Therefore, sacrificing Ratio is the proportion in which the existing partners of a company give up a part of their share to give to the nRead more

When a partnership firm consisting of some partners, decide to admit a new partner into their firm, they have to forego a part of their share for the new partner. Therefore, sacrificing Ratio is the proportion in which the existing partners of a company give up a part of their share to give to the new partner. The partners can choose to forego their shares equally or in an agreed proportion.

Before admission of the new partner, the existing partners would be sharing their profits in the old ratio. Upon admission, the profit-sharing ratio would change to accommodate the new partner. This would give rise to the new ratio. Hence Sacrificing ratio can be calculated as:

Sacrificing Ratio = Old Ratio – New Ratio

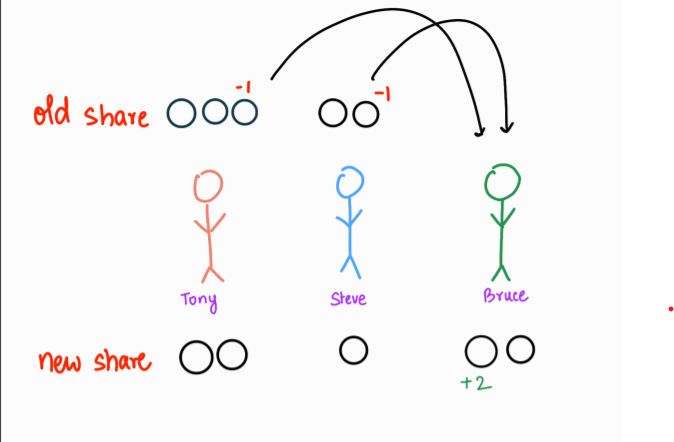

For example, Tony and Steve are partners in a firm, sharing profits in the ratio of 3:2. They decide to admit Bruce into the partnership such that the new profit-sharing ratio is 2:1:2. Now, to calculate the sacrificing ratio of Tony and Steve, we subtract their new share from their old share.

Tony’s Sacrifice = 3/5 – 2/5 = 1/5

Steve’s Sacrifice = 2/5 – 1/5 = 1/5

Therefore, the Sacrificing ratio of Tony and Steve is 1:1. This shows that Tony gave up 1/5th of his share while Steve also sacrificed 1/5th of his share.

Calculation of sacrificing ratio is important in a partnership as it helps in measuring that portion of the share of existing partners that have to be sacrificed. This ensures a smooth reconstitution of the partnership. Since the old partners are foregoing a part of their share in profits, the new partner has to bring in some amount as goodwill to compensate for their loss.

See less

Yes, Capital Work in Progress is Tangible Asset. To attain an understanding of the same, we first need to understand what are tangible assets. Assets that have a physical existence, that is they can be seen, touched are called Tangible Assets. Capital work in progress is the cost incurred on fixed aRead more

Yes, Capital Work in Progress is Tangible Asset.

To attain an understanding of the same, we first need to understand what are tangible assets. Assets that have a physical existence, that is they can be seen, touched are called Tangible Assets.

Capital work in progress is the cost incurred on fixed assets that are under construction as on the balance sheet date. Since the asset cannot be used for operation it cannot be classified as a Fixed Asset.

For example:

If an asset takes 1.5 years to be constructed as on 1.4.2020 then on the balance sheet date 31.3.2021, the cost incurred on the asset will be classified as Capital Work in Progress.

Common examples of Capital Work in Progress include immovable assets like Plant and Machinery, Buildings.

It is shown under the head Non-Current Assets in the balance sheet. Examples of cost included in Capital Work in Progress can be:

Since the assets under the head Capital Work in Progress are in the process of completion and not completed, hence they are not depreciable until completed. Once the asset is completed it is moved under the head Fixed Assets.

Capital Work in Progress is shown in the Balance Sheet as:

See less