Yes, a creditor is a liability. Creditors are treated as current liability. A creditor is a person who provides money or goods to a business and agrees to receive repayment of the loan or the payment of goods at a later date. The loan may be extended with or without interest. Creditors may be secureRead more

Yes, a creditor is a liability. Creditors are treated as current liability.

A creditor is a person who provides money or goods to a business and agrees to receive repayment of the loan or the payment of goods at a later date. The loan may be extended with or without interest.

Creditors may be secured creditors or unsecured creditors. In the case of secured creditors, some collateral is usually pledged to them. In the case of a default, they can sell or otherwise dispose of the collateral in any manner to recover the money due to them.

In the case of unsecured creditors, no collateral is pledged against the amount due to them. In the case of a default, they can approach a Court to enforce repayment but cannot sell any asset of the company by themselves.

Why are Creditors treated as a liability?

An asset is something from which the business is deriving or is likely to derive economic benefit in the future. The business has legal ownership of that asset which is legally enforceable in a court of law. For example, Plant and Machinery, accrued interest, building, etc

A liability is a legal obligation of the business. It may be in the form of outstanding payments or loans or the owner’s share of the company that the company has to pay them as and when demanded.

As the company has a legal obligation to pay money to the creditor, they are treated as a liability. Most creditors are to be repaid within 1 year and are hence classified as current assets.

Treatment and Importance of Creditors

Creditors are mostly treated as current liabilities. They are shown under the head “current liabilities” of the balance sheet of a company.

The significance/importance of creditors is as follows:

- The amount due to creditors affects the current and acid test ratio of a company significantly.

- It affects the short-term cash requirements of a company.

- It affects the credit policy of the company. A company can extend longer credit periods to customers if it can avail longer credit periods from its suppliers.

- Having too many creditors or a large amount due to creditors can affect investor sentiment negatively regarding the business.

We can conclude that the creditor being a person to whom the business is legally liable to pay a certain sum of money after a certain period of time has to be classified as a liability.

Creditors play a major role in determining the success of a business. They act as a major constituent of the supply cycle of the business and affect the cash flows of the business. They are shown under the head “current liabilities” of the balance sheet of a company.

See less

Debts are of two types one is Good Debt, and another one is Bad debt. Bad Debts The amount which is not recoverable from the debtors is called Bad debt. It is an uncollectable amount from the organization's customers due to the customer's inability to pay the amount of money taken on credit. Read more

Debts are of two types one is Good Debt, and another one is Bad debt.

Bad Debts

The amount which is not recoverable from the debtors is called Bad debt. It is an uncollectable amount from the organization’s customers due to the customer’s inability to pay the amount of money taken on credit.

Example 1

Mr A borrowed $100 from Mr B for his college fee and agrees to pay in 2 months. After the time period is complete Mr A failed to repay the borrowed amount. This is a Bad Debt for Mr B.

Example 2

XYZ Co. had made a credit sale of $50,000. A debtor who has to pay $1000 has been bankrupted. XYZ co. cannot recover the amount from the Debtor, so it records the irrecoverable amount as a bad debt.

Journal Entry

In this entry, “Bad debts are written off of Rs. 2000.”

Bad debt is the amount not recoverable from debtors, which is a loss for the organization.

Modern Rule

The Modern rules of accounting for Expenses are “Debit the increase in expenses and Credit the decrease in expenses.”

Golden Rule

The Golden rules of accounting for expenses and losses are “Debit all expenses and losses, Credit all incomes and gains.”

Bad Debts A/c Dr. 2,000

To Debtor’s A/c 2000

Bad debt is treated as a loss for the organization. As per the rule, this should be debited to the profit and loss account.

Profit and Loss A/c Dr. – 2000

To Bad Debts A/c – 2000

Instead of passing two separate entries for writing off, we can combine the entries and pass one entry.

Profit and Loss A/c Dr. 2000

To Debtor’s A/c 2000

Recovery of Bad debts

Recovery of Bad debt is the amount received for a debt that was written off in the past. It was considered uncollectable.

When we write off bad debt, it is recorded as a loss, but the recovery of bad debts is treated as an income for the business.

It is treated as an income and the recovery of bad debt is shown on the credit side of the Income statement.

Journal Entry for Recovery of Bad debts

Bank/Cash A/c Dr. – Amount

To Bad Debts Recovered A/c – Amount

Rules applied in the Journal entry are as per the Golden rules of accounting,

“Cash/Bank A/C” is a real account therefore debit what comes in and credit what goes out.

“Bad Debts Recovered A/C” is a nominal account therefore debit all expenses and losses, and credit all incomes and gains.

Treatment of “Bad Debt written off of Rs.2ooo.”

In Trial Balance: No effect

In Income Statement: It is shown on the debit side as Rs.2000 (loss)

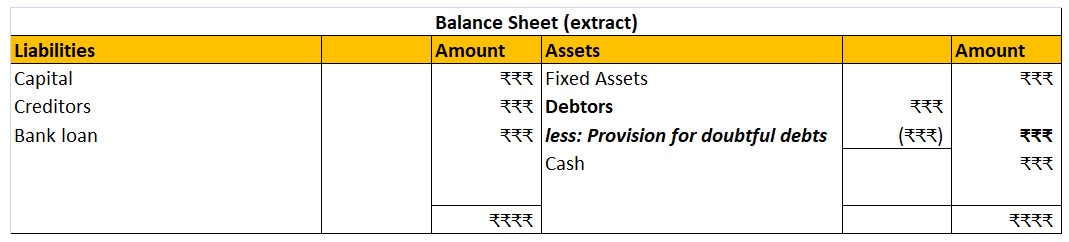

In Balance Sheet: Rs.2000 shall be deducted from the sundry debtor account.

See less