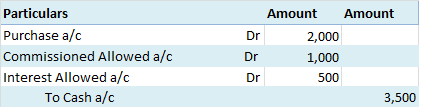

The journal entry for commission received is as presented below: Cash A/c / Bank A/c / A Personal A/c Dr. - ₹ To Commission received A/c - ₹ (Being ₹ commission received) The commission received means an amount received by a person or entity forRead more

The journal entry for commission received is as presented below:

Cash A/c / Bank A/c / A Personal A/c Dr. – ₹

To Commission received A/c – ₹

(Being ₹ commission received)

The commission received means an amount received by a person or entity for the provision of a service. For example, a firm sold goods worth ₹10,000 of a manufacturer and was paid an amount of ₹1000 in cash as commission. So, the entry in the books of accounts of the firm will be as follows:

Cash A/c Dr. ₹1000

To Commission received A/c ₹1000

Now, let’s understand the logic behind the journal entry through the modern rules of accounting.

Cash account, bank account and personal account are asset accounts. Hence, they are debited when assets are increased.

While the commission received account is an income account. Hence, when income increases, it is credited.

As per the traditional rules i.e. the golden rules of accounting, these are the explanations:

Commission can be received in cash or bank. Hence the Cash or Bank account is debited as they are real accounts.

“Debit what comes in, credit what goes out”

Also, when it is not received but accrued, then a personal account is debited (the person or entity who has received the service but has not paid for it yet). The following rule applies to the personal account.

“Debit the receiver, credit the giver”

Commission received is an income, thus it is a nominal account. It will be credited because of the following rule of nominal accounts:-

“Debit all expense and losses, credit all income and gains”

See less

Personal Accounts: The accounts of persons, firms, companies, etc. are personal accounts. There is a further classification to personal accounts- Accounts of Natural Persons: The transactions relating to individual human beings fall under this category. For Example, accounts of Joseph, Richard, MorrRead more

Personal Accounts: The accounts of persons, firms, companies, etc. are personal accounts. There is a further classification to personal accounts-

Note: When any Prefix or Suffix is used before/ after any nominal account head, such account is classified as Representative personal account under traditional approach.

For Example, Salary A/c is a nominal account whereas salary outstanding A/c is a personal account as the word outstanding is being used as a prefix to Salary A/c.

The Accounting rule for Personal Account is –

Debit the Receiver of the benefit.

Credit the Giver of the benefit.

Real Account: The transactions relating to tangible things i.e. the things that can be seen, touched and physically exchanged and the intangible things that cannot be seen, touched but the presence can be felt comes under this category. For Example, tangible things like Cash, goods, building, machinery, etc. and intangible things like goodwill, patent, trademarks, etc.

The Accounting rule for Real Account is –

Debit what comes in.

Credit what goes out.

Nominal Accounts: The transactions relating to losses, expenses, incomes and gains comes under this category. For Example, Rent paid, wages paid, commission received, interest paid/ received, etc.

The Accounting rule for Nominal Account is –

Debit Expenses and Losses.

Credit Gains and Incomes.

Some Common Examples under the three heads are

See less