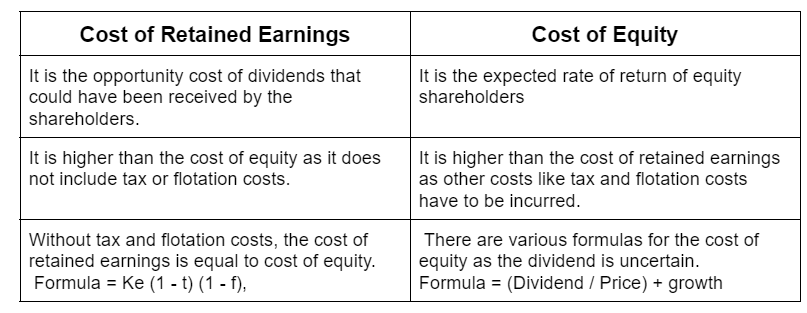

Retained earnings are kept with the company for growth instead of distributing dividends to the shareholders. Therefore the cost of retained earnings refers to its opportunity cost which is the cost of foregoing dividends by the shareholders. Therefore the cost of retained earnings is similar to theRead more

Retained earnings are kept with the company for growth instead of distributing dividends to the shareholders. Therefore the cost of retained earnings refers to its opportunity cost which is the cost of foregoing dividends by the shareholders.

Therefore the cost of retained earnings is similar to the cost of equity without tax and flotation cost. Hence, it can be calculated as

Kr = Ke (1 – t) (1 – f),

Kr = Cost of retained earnings

Ke = Cost of equity

t = tax rate

f = flotation cost

Here, flotation cost means the cost of issuing shares.

EXAMPLE

If cost of equity of a company was 10%, tax rate was 30% and flotation cost was 5%, then

cost of retained earnings = 10% x (1 – 0.30)(1 – 0.05) = 6.65%.

From the above example and formula, it is clear that the cost of retained earnings would always be less than or equal to the cost of equity since retained earnings do not involve flotation costs or tax.

A company usually acquires funds from various sources of finance rather than a single source. Therefore the cost of capital of the company will be the weighted average cost of capital (WACC) of each individual source of finance. The cost of retained earnings is thus an important factor in calculating the overall cost of capital.

Another important factor of WACC is the cost of equity. The cost of equity is sometimes interchanged with the cost of retained earnings. However, they are not the same.

See less

The commercial banks are required to keep a certain amount of their deposits with the central bank and the percentage of deposits that the banks are required to keep as reserves is called Cash Reserve Ratio. The banks have to keep the amount to maintain the Cash Reserve Ratio with the RBI. CRR meansRead more

The commercial banks are required to keep a certain amount of their deposits with the central bank and the percentage of deposits that the banks are required to keep as reserves is called Cash Reserve Ratio.

The banks have to keep the amount to maintain the Cash Reserve Ratio with the RBI.

CRR means that commercial banks cannot lend money in the market or make investments or earn any interest on the amount below what is required to be kept in CRR.

RBI mandates Cash Reserve Ratio so that a percentage of the bank’s deposit is kept safe with the RBI, hence, in an uncertain event bank can still fulfill its obligation against its customers.

CRR also helps RBI to control liquidity in the economy. When CRR is kept at a higher rate, the lower the liquidity in the economy, and similarly when CRR is kept at a lower rate, there is higher liquidity in the economy.

The Reserve Bank of India also regulates inflation through the Cash Reserve Ratio:

The formula for CRR is-

Reserves maintained with Central Banks / Bank Deposits * 100%

For example:

The current CRR is 3% which means that for every Rs 100 deposit in the commercial banks have to keep Rs 3 as a deposit with RBI.

See less