Profit refers to the excess of total revenue over total expenses. According to the rule "Debit all expenses and losses, Credit all incomes and gains", expenses are recorded on the debit side while revenues are recorded on the credit side. There is profit when Total revenue > Total expenses, whichRead more

Profit refers to the excess of total revenue over total expenses. According to the rule “Debit all expenses and losses, Credit all incomes and gains”, expenses are recorded on the debit side while revenues are recorded on the credit side.

There is profit when Total revenue > Total expenses, which means the balance of the credit side > the balance of the debit side. Since, in accounting Dr. side is always equal to the credit side, a balancing figure (representing profit or loss) is shown on the shorter side, to make both sides equal.

When Credit side > Debit side, Profit(balancing figure) is shown on the Dr. side so that both sides are equal.

PROFIT

Profit refers to the excess of total revenue over the total expenses of the business for an accounting year. In simple words, it shows how much extra the firm earned after deducting all the expenses it incurred during the year.

Profit = Total Revenue – Total Expenses

Suppose, the firm earned a total revenue of $10,000 for the accounting year 2022-23. Also, it incurred total expenses of $6,000 during the year. So, Profit for the AY 2022-23 is $4,000.

ASCERTAINING PROFIT

To ascertain profit earned or loss incurred by the firm during an accounting year, it prepares two accounts.

- Trading A/c

- Profit and Loss A/c

Points to be noted:

- Both accounts are Nominal Account which follows the rule “Debit all expenses and losses, Credit all incomes and gains”

- The debit side records expenses while the Credit side records incomes.

- Both are balanced accounts, which means its Dr. side is always equal to its Cr. side.

- If they are not balanced, then a balancing figure is added to the shorter side which represents profit or the loss depending on which side is greater.

- If Dr. side > Cr. side, it means expenses are more than the incomes and thus, there is a loss.

- If Cr. side > Dr. side, it means there are more incomes than expenses and thus, there is Profit.

TRADING ACCOUNT

It is the first final account prepared for calculating gross profit or gross loss during the year because of the trading activities of the firm.

Trading activities are related to the buying and selling of goods. In between buying and selling a lot of activities are there like transportation, warehousing, loading, unloading, etc. All expenses that are directly related to buying and selling as well as manufacturing of goods are known as Direct expenses and are also recorded in the trading accounts.

Items included on the debit side:

- Opening stock

- Purchases

- Direct expenses like wages, import duty, royalty, manufacturing expenses, etc.

- Gross Profit

Items included on the credit side:

- Sales

- Closing stock

- Gross loss

Gross Profit is when Cr. side (incomes) > Dr. side (expenses). It is recorded on the debit side as a balancing figure.

PROFIT AND LOSS ACCOUNT

A businessman incurs a lot of expenses during the year which may be directly related or indirectly related to the business.

As the Trading account only considers direct expenses, the businessman prepares the P&L A/c which considers all the expenses incurred during a year to ascertain net profit or loss.

Items written on the Debit side

- Gross loss (transferred from the trading a/c)

- Office and administrative expenses (like employee’s salary, office rent, office lighting bills, legal charges, printing expenses, etc.)

- Selling and distribution expenses (like advertisement fees, commission, carriage outward, packaging charges, etc.

- Miscellaneous expenses (like interest on loan, interest on capital, repair, depreciation, etc.)

- Net Profit

Items written on the Credit side

- Gross Profit (transferred from trading a/c)

- Other incomes and gains (Like income from investments, interest received, rent received, etc.)

- Net loss

Net Profit is when the Cr. side (incomes)> Dr. side(expenses). It is recorded on the Debit side as a balancing figure.

See less

Definition Journal Entry is an entry made in the journal is called journal entry. And the process of recording a transaction in a journal is called journalizing. Broadly journal entries are of two types : 1. Simple entry 2. Compound entry Otherwise, they are categorized into seven types which are asRead more

Definition

Journal Entry is an entry made in the journal is called journal entry. And the process of recording a transaction in a journal is called journalizing.

Broadly journal entries are of two types :

1. Simple entry

2. Compound entry

Otherwise, they are categorized into seven types which are as follows :

1. Opening entries

2. Closing entries

3. Rectification entries

4. Transfer entries

5. Adjusting entries

6. Entries on dishonor of bills

7. Miscellaneous entries

Explanation

Now let me explain to you the above types of entries mentioned which are as follows ;

Simple entry

• Is a journal entry in which one account is debited and another account is credited with an equal amount.

• For example, the purchase of goods of Rs 5000 cash. It will affect two accounts,i.e., purchase A/C and cash A/C with the amount of Rs 5000.

Compound entry

• Is a journal entry in which one or more accounts are debited and/or one or more accounts credited or vice versa.

• For example the sale of goods to Sati for Rs 5000, Rs 2000 is received in cash, and the balance is to be received later.

• This transaction of the sale has an effect on three accounts i.e cash or bank A/C, Sati A/C, and sales A/C.

Opening entries

• Are defined as when books are started for the new year, the opening balance of assets and liabilities are journalized. For example bills payable, short-term loans, etc.

Closing entries

• At the end of the year, the profit and loss account has to be prepared. For this purpose, the nominal accounts are transferred to this account. This is done through journal entries called closing entries.

Rectification entries

• If an error has been committed, it is rectification through a journal entry.

Transfer entries

• If some amount is to be transferred from one account to another, the transfer will be made through a journal entry.

Adjusting entries

• At the end of the year, the number of expenses or income may have to be adjusted for amounts received in advance or for amounts not yet settled in cash.

• Such an adjustment is also made through journal entries. Usually, the entries pertain to the following :

Outstanding expenses,i.e., expenses incurred but not yet paid;

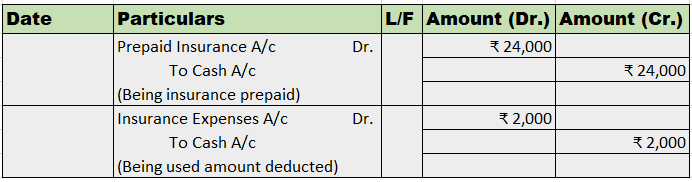

Prepared expenses,i.e., expenses paid in advance for some period in the future ;

Interest on capital is the interest proprietor’s investment in the business entity investment; and

Depreciation fall in the value of assets used on account of wear and tear. For all these, journal entries are necessary.

Entries on dishonor of bills

• If someone who accepts a promissory note ( or bill) is not able to pay in on the due date, a journal entry will be necessary to record the non–payment or dishonor.

Miscellaneous entries

The following entries will also require journalizing

• Credit purchase of things other than goods dealt in or materials required for the production of goods e.g. Credit purchase of furniture or machinery will be journalized.

• An allowance to be given to the customers or a charge to be made to them after the issue of the invoice.

• Receipt of promissory notes or issue to them if separate bills books have not been maintained.

• On an amount becoming irrecoverable, say, because, of the customer becoming insolvent.

• Effects of accidents such as loss of property by fire.

• Transfer of net profit to capital account.

Here are some examples of journal entries showing the above types :

See less