Negative working capital means the excess of current liabilities over current assets in an enterprise. Let’s understand what working capital is to get more clarity about negative working capital. Meaning of Working Capital Working Capital refers to the difference between current assets and current lRead more

Negative working capital means the excess of current liabilities over current assets in an enterprise.

Let’s understand what working capital is to get more clarity about negative working capital.

Meaning of Working Capital

Working Capital refers to the difference between current assets and current liabilities of a business.

Working Capital = Current Assets – Current Liabilities

It is the capital that an enterprise employs to run its daily operations. It indicates the short term liquidity or the capacity to pay off the current liabilities and pay for the daily operations.

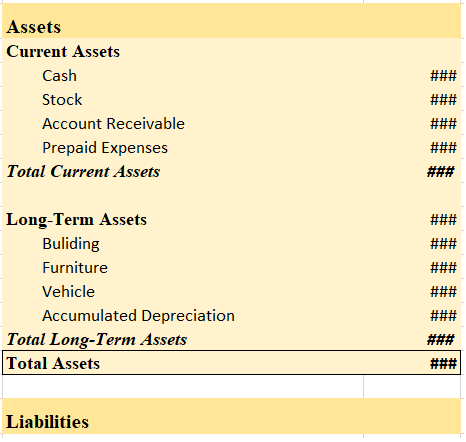

Items under Current Assets and Current Liabilities

It is important to know about the items under current assets and current liabilities to understand the significance of working capital.

Current assets include cash and bank balance, accounts receivables, inventories, short term investments, prepaid expenses etc.

Current liabilities include accounts payable, short term loans, bank overdraft, interest on short term investment, outstanding salaries and wages etc.

Types of working capital

Since the working capital is just the difference between current assets and liabilities, the working capital can be one of the following:

- Positive (Current assets > Current liabilities)

- Zero (Current assets = Current liabilities)

- Negative (Current assets < Current liabilities)

Hence, negative working capital exists when current liabilities are more than current assets.

Implications of having negative working capital

Having negative working capital is not an ideal situation for an enterprise. Having negative working capital indicates that the enterprise is not in a position to pay off its current liabilities and there may be a cash crunch in the business.

An enterprise may have to finance its working capital requirements through long term finance sources if its working capital remains negative for quite a long time.

The ideal situation is to have current assets two times the current liabilities to maintain a good short term liquidity of the business i.e.

Current Assets = 2(Current Liabilities)

See less

Any person, company, or organization that owes us money is a debtor. The amount that is owed to us is called debt. When you are unsure if a debtor is going to pay back the amount owed to you, then a provision for doubtful debts is created. Here, the debtor may or may not pay back the amount owed. WhRead more

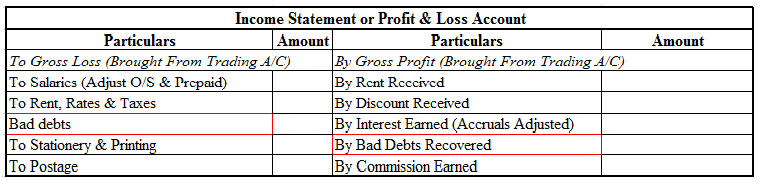

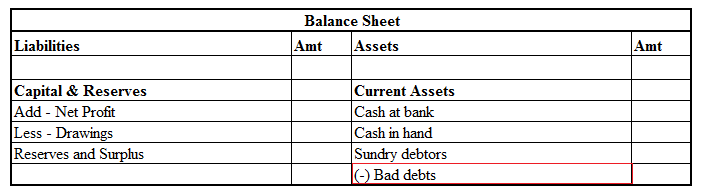

Any person, company, or organization that owes us money is a debtor. The amount that is owed to us is called debt. When you are unsure if a debtor is going to pay back the amount owed to you, then a provision for doubtful debts is created. Here, the debtor may or may not pay back the amount owed. When the debts owed to us is irrecoverable, it is termed as bad debts.

Provision for doubtful debts may become a bad debt at some point. Usually, companies keep a small portion of their debtors as a provision for doubtful debts in accordance with the prudence concept that tells us to account for all possible losses. Provision for doubtful debts is a liability whereas bad debts are recorded as an expense.

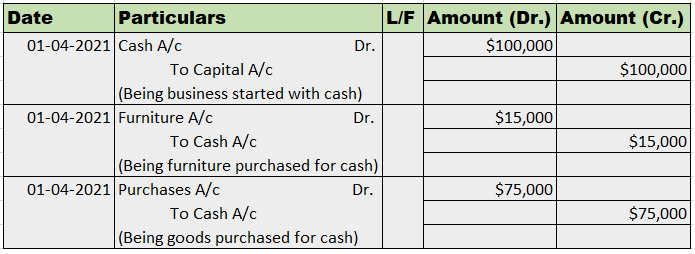

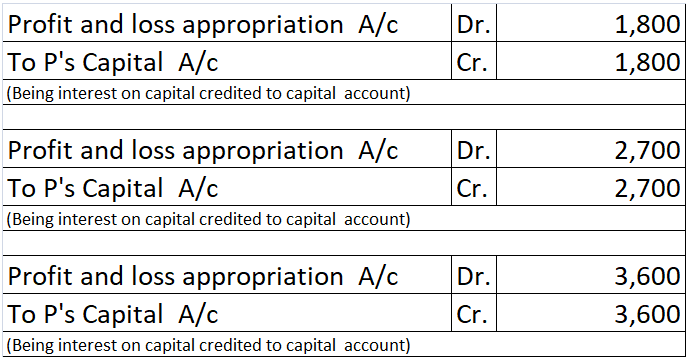

Journal entries for Doubtful debts and bad debts are as follows:

EXAMPLE

If the balance in the debtors’ account shows an amount of Rs 20,000 and 5% of debtors are treated as doubtful, then Rs 1,000 is recorded as a provision for doubtful debts. This amount is deducted from debtors in the balance sheet.

Now if Rs 400 was recorded as actual bad debts, then it is deducted from the provision for doubtful debts instead of debtors. Further another 400 is added back to provision for doubtful debts to maintain the percentage.

See less