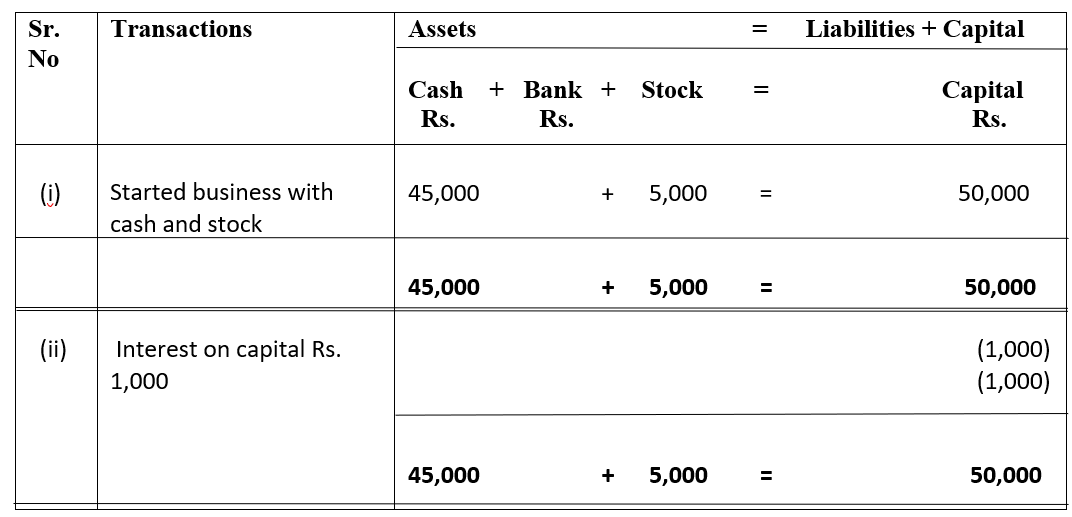

The term set off in English means to offset something against something else. It thereby refers to reducing the value of an item. In accounting terms, when a debtor can reduce the amount owed to a creditor by cancelling the amount owed by the creditor to the debtor, it is termed as set off. It is coRead more

The term set off in English means to offset something against something else. It thereby refers to reducing the value of an item. In accounting terms, when a debtor can reduce the amount owed to a creditor by cancelling the amount owed by the creditor to the debtor, it is termed as set off.

It is commonly used by banks where they seize the amount in a customer’s account to set off the amount of loan unpaid by the customer.

Types

There are various types of set-offs as given below:

- Transaction set-off – This is where a debtor can simply reduce the amount he is owed from the amount he owes to the creditor.

- Contractual set-off – Sometimes, a debtor agrees to not set off any amount and hence he would have to pay the entire amount to the creditor even if the creditor owed some amount to the debtor.

- Insolvency set-off – These rules are mandatory and have to be followed under the Insolvency rules 2016.

- Bankers set-off – Here, the bank sets off the amount of a customer with another account of the customer.

Example

Let’s say Divya owes Rs 20,000 to Sherin for the purchase of goods. But, Sherin owed Rs 6,000 to Divya already for use of her Machinery. Therefore, the amount of 6,000 can be set off against the 20,000 owed to Sherin and hence Divya would effectively owe Sherin Rs 14,000.

This helps in reducing the number of transactions and unnecessary flow of cash.

See less

Brief Introduction The stock of finished goods left unsold at the end of the year is known as closing stock. As closing stock represent an asset i.e. the unsold finished goods, it has a debit balance. Closing stock appears on the credit side of the trading account and on the asset side of the balanRead more

Brief Introduction

The stock of finished goods left unsold at the end of the year is known as closing stock. As closing stock represent an asset i.e. the unsold finished goods, it has a debit balance.

Closing stock appears on the credit side of the trading account and on the asset side of the balance sheet. But, if closing stock is adjusted against purchase i.e. deducted from purchase account balance, then it doesn’t appear in the trading account.

It is always shown on the asset of the balance irrespective of its treatment as discussed above because it is an asset.

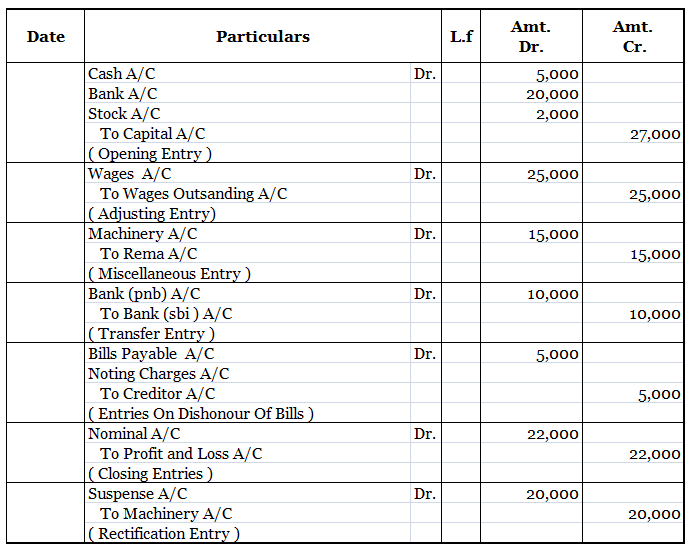

Though no ledger is maintained for closing stock in financial accounts of a business, the journal entry for the closing stock is passed and is as below:

Closing stock A/c Dr Amt

To Trading A/c Amt

(When the closing stock appears in trading a/c)

OR

Closing stock A/c Dr Amt

To Purchase A/c Amt

(When closing stock is adjusted against purchase A/c and not shown in trading a/c)

Generally, the closing stock is shown separately in the trial balance because it is already part of the purchase account balance.

Closing stock is ascertained at the end of the financial year and it has great importance as it directly affects the gross profit or loss of a business. Closing stock at end of a year becomes the opening stock of the next financial year.

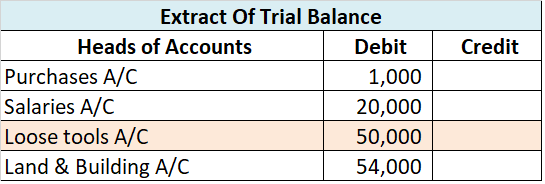

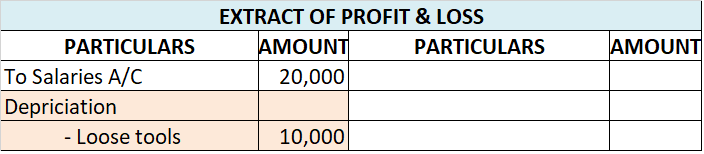

Numerical Example

ABC trading reported the following particulars at the end of the financial year 20X2-20X3:

We will draw the trading and P/L account and balance sheet of ABC Trading using the above information.

As the closing stock is not given, we will calculate the closing stock as a balancing figure.

It can be also calculated using this formula:

Closing stock = Opening stock + Purchase + Gross Profit – Sales

See less