General reserve is the part of profits or money kept aside to meet future uncertainties and obligations of the entity. General reserve is created out of revenue profits for unspecified purposes and therefore is also a part of free reserves. General reserve forms a part of the Profit & Loss ApprRead more

General reserve is the part of profits or money kept aside to meet future uncertainties and obligations of the entity. General reserve is created out of revenue profits for unspecified purposes and therefore is also a part of free reserves.

General reserve forms a part of the Profit & Loss Appropriation account and is created to strengthen the financial position of the entity and serves as a sources of internal financing. It is upon the discretion of the management as to how much of a reserve is to be created. No reserve is created when the entity incurs losses.

General reserve is shown in the Reserves & Surplus head on the liability side of the balance sheet of the entity and carries a credit balance.

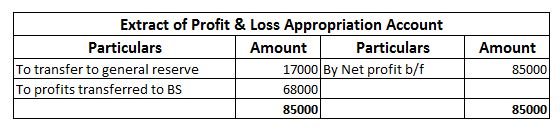

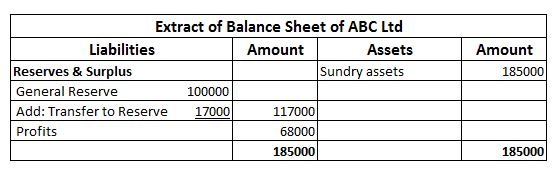

Suppose, an entity, ABC Ltd engaged in the business of electronics earns a profit of 85000 in the current financial year and has an existing general reserve amounting to 100000. The management decides to keep aside 20% of its profits as general reserve.

Then the amount to be transferred to general reserve will be = 85000*20% = 17000.

In the financial statements it will be shown as follows-

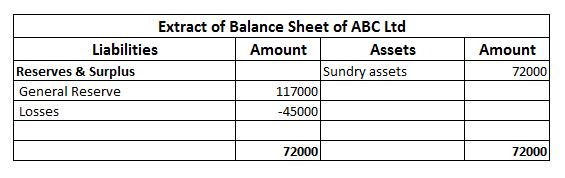

Now, in the next financial year, the entity incurs losses amounting to 45000. In this case, no amount shall be transferred to the general reserve of the entity and will be shown in the financial statement as follows-

The creation of general reserve can sometimes be deceiving since it does not show the clear picture of the entity and absorbs losses incurred.

See less

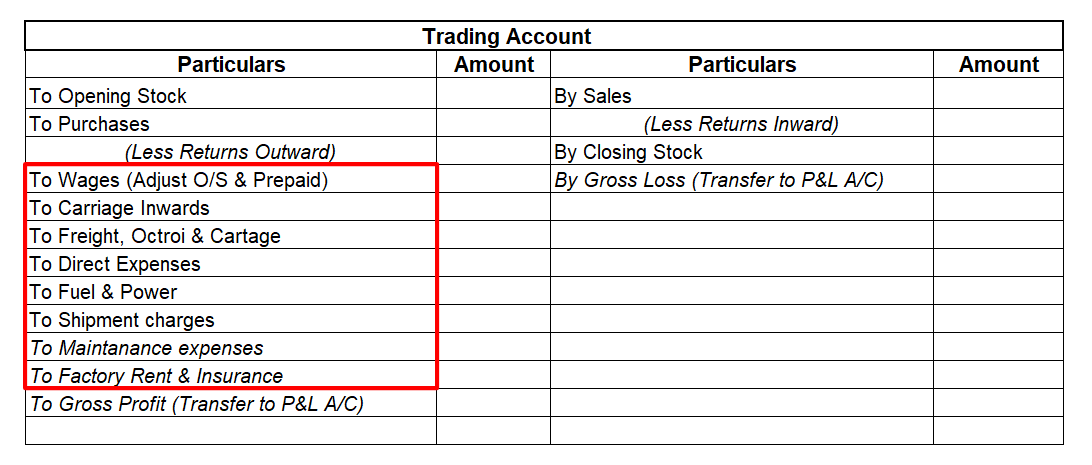

As per the Golden Rules As per the golden rules of accounting, a trading account is a nominal account. To ensure that financial statements accurately reflect a business's financial position and performance, the golden rules of accounting guide the preparation of financial statements. The point to noRead more

As per the Golden Rules

As per the golden rules of accounting, a trading account is a nominal account. To ensure that financial statements accurately reflect a business’s financial position and performance, the golden rules of accounting guide the preparation of financial statements.

The point to note is that it is almost impossible to apply the rules of debit and credit with certain accounts such as Trading A/c, Profit & Loss A/c, etc.

As per the Modern Rules

The purpose of a trading account is to record transactions related to the purchase and sale of goods for a business. In other words, it serves as a recording and reporting mechanism for business income and expenses.

An accounting period, like a month, quarter, or year, is the time when a trading account is prepared. It is used to calculate the business’s net profit or loss. Other financial statements, such as the balance sheet, are prepared using the information in a trading account.

In summary, a trading account is a type of income statement account that is used to track and report on the income and expenses from a business’s buying and selling activities

Rules of Debit and Credit

There are three main types of accounts according to the legacy rules of debit and credit: personal accounts, real accounts, and nominal accounts. A personal account is one that is related to an individual or entity owing the business money (e.g. a customer), or owing the business money (e.g. a supplier).

A real account is one that relates to assets such as cash, inventory, and property.

Nominal accounts are accounts that relate to income and expenses, such as a “trading account”.

To summarize, a trading account is a nominal account used to record and report the business’s income and expenses resulting from its buying and selling activities.

See less