When the Accumulated depreciation account is not maintained, the journal entry for vehicle depreciation shall be Particulars Debit Credit Depreciation a/c Dr. (xxx) To Vehicle a/c (xxx) (Being DepreciationRead more

When the Accumulated depreciation account is not maintained, the journal entry for vehicle depreciation shall be

| Particulars | Debit | Credit |

| Depreciation a/c Dr. | (xxx) | |

| To Vehicle a/c | (xxx) | |

| (Being Depreciation charge on Vehicle made) |

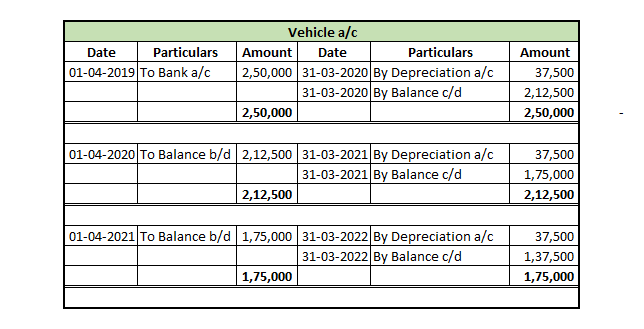

For example, let us assume that a vehicle (Bike) was purchased on 1st April 2019 with INR. 2,50,000, the rate of depreciation is 15% and also the Company follows the straight-line method of calculating depreciation.

Then the journal entries shall be,

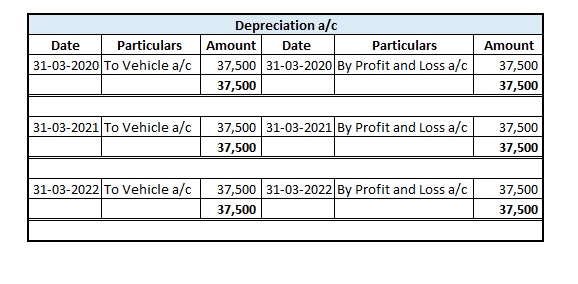

The depreciation charge for the 1st Year

| Date | Particulars | Debit | Credit |

| 31-03-2020 | Depreciation a/c Dr. | 37,500 | |

| To Vehicle a/c | 37,500 | ||

| (Being Depreciation made on Vehicle) |

The depreciation charge for the 2nd Year

| Date | Particulars | Debit | Credit |

| 31-03-2021 | Depreciation a/c Dr. | 37,500 | |

| To Vehicle a/c | 37,500 | ||

| (Being Depreciation made on Vehicle) |

The depreciation charge for the 3rd Year

| Date | Particulars | Debit | Credit |

| 31-03-2022 | Depreciation a/c Dr. | 37,500 | |

| To Vehicle a/c | 37,500 | ||

| (Being Depreciation made on Vehicle) |

The respective ledger accounts for all three years are given below:

When the Accumulated depreciation account is maintained, the journal entry for vehicle depreciation shall be

| Particulars | Debit | Credit |

| Depreciation a/c Dr. | (xxx) | |

| To Accumulated depreciation a/c | (xxx) | |

| (Being Depreciation charge on Vehicle made) |

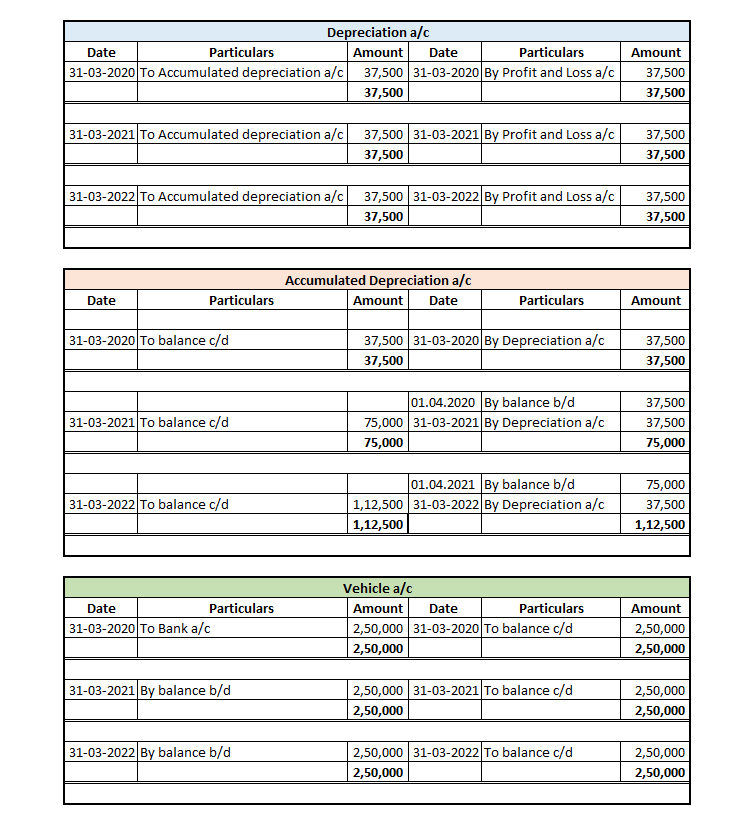

Taking the above said example,

The depreciation charge for the 1st Year

| Date | Particulars | Debit | Credit |

| 31-03-2020 | Depreciation a/c Dr. | 37,500 | |

| To accumulated depreciation a/c | 37,500 | ||

| (Being Depreciation made on Vehicle) |

The depreciation charge for the 2nd Year

| Date | Particulars | Debit | Credit |

| 31-03-2021 | Depreciation a/c Dr. | 37,500 | |

| To accumulated depreciation a/c | 37,500 | ||

| (Being Depreciation made on Vehicle) |

The depreciation charge for the 3rd Year

| Date | Particulars | Debit | Credit |

| 31-03-2021 | Depreciation a/c Dr. | 37,500 | |

| To accumulated depreciation a/c | 37,500 | ||

| (Being Depreciation made on Vehicle) |

The respective ledger accounts for all three years are given below:

See less

Meaning Capital assets mean the assets which are used in the business operations to generate revenue. The benefit from these assets is expected to flow to the enterprise beyond the time span of one year. Capital assets are commonly called fixed assets. Examples of capital assets are plant, machineryRead more

Meaning

Capital assets mean the assets which are used in the business operations to generate revenue. The benefit from these assets is expected to flow to the enterprise beyond the time span of one year. Capital assets are commonly called fixed assets.

Examples of capital assets are plant, machinery, land, building, vehicles etc.

To expense the capital assets for the economic benefits they provide, they are depreciated over their useful life on some equitable basis.

When capital assets are sold, the gain on sale is credited to the capital reserve account. On loss, it is simply debited to the profit and loss account. Capital assets are shown under the heading ‘Plant, Property and Equipment’ under the asset head of the balance sheet.

Assets that do not qualify as capital assets

The assets which provide economic benefits for less than a year do not qualify as capital assets. Such as inventories, accounts receivables etc. are not capital assets.

Also, those assets which are not intended to be held for more than 1 year are not capital assets even if such assets are capable of providing economic benefits for more than 1 year. Such assets will be considered current assets.

For example, if a plot of land is purchased by a business but the intention is to sell it after 2 months then such land will not be considered a capital asset.

See less