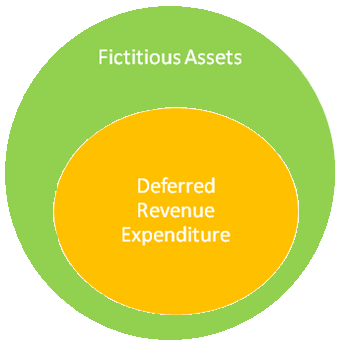

In the books of Krish Fitness and Wellness Club Income & Expenditure A/c for the year ended 31 March 2020 Expenditure Amt Income Amt To Doctors and Coaches Honorarium 25,000 By Subscription (600*100) 60,000 To Medicines 15,500 By Entrance Fees 25,000 To General Expenses 8,000 By Miscellaneous ReRead more

In the books of Krish Fitness and Wellness Club

Income & Expenditure A/c for the year ended 31 March 2020

| Expenditure | Amt | Income | Amt |

| To Doctors and Coaches Honorarium | 25,000 | By Subscription (600*100) | 60,000 |

| To Medicines | 15,500 | By Entrance Fees | 25,000 |

| To General Expenses | 8,000 | By Miscellaneous Receipts | 15,000 |

| To Newspaper | 8,000 | By Deficit (excess of expenditure over income) | 21,500 |

| To Rent, Rates and Taxes | 5,000 | ||

| To Tournament Expenses (W.N.1) | 25,000 | ||

| To Loss on Sale of Medical Equipment (W.N.2) | 10,000 | ||

| To Depreciation on Medical Equipment | 25,000 | ||

| 1,21,500 | 1,21,500 |

Working Notes:

1.Calculation of Tournament Fund

| Tournament Fund as of 1 April 2019 | 15,000 |

| Add: Donations to Tournament Fund | 20,000 |

| Less: Tournament Expenses | -60,000 |

| Tournament Expenses | -25,000 |

2. Calculation of Loss on Sale of Medical Equipment

| Book Value of Medical Equipment | 15,000 |

| Less: Sold | -5,000 |

| Loss on Sale of Medical Equipment | 10,000 |

Interest on Investment is to be shown on the Credit side of a Trial Balance. Interest on investment refers to the income received on investment in securities. These securities can be shares, debentures etc. of another company. When one invests in securities, they are expected to receive a return onRead more

Interest on Investment is to be shown on the Credit side of a Trial Balance.

Interest on investment refers to the income received on investment in securities. These securities can be shares, debentures etc. of another company. When one invests in securities, they are expected to receive a return on investment (ROI).

Since interest on investment is an income, it is shown on the credit side of the Trial Balance. This is based on the accounting rule that all increase in incomes are credited and all increase in expenses are debited. A Trial Balance is a worksheet where the balances of all assets, expenses and drawings are shown on the debit side while the balances of all liabilities, incomes and capital are shown on the credit side.

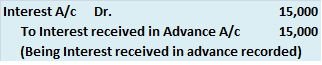

For example, if Jack bought Corporate Bonds of Amazon, worth $50,000 with a 10% interest on investment, then the accounting treatment for interest on investment would be

Cash/Bank A/C Dr 5,000

To Interest on Investment in Corporate Bonds (Amazon) 5,000

As per the above entry, since interest on investment is credited, it will show a credit balance and hence be shown on the credit side of the Trial Balance. Interest on investment account is not to be confused with an Investment account. Investment is an asset whereas interest on investment is an income.

See less