Financial Reporting is a common practice in accounting where the financial statements of the company are disclosed to present its financial information and performance over a particular period. It is important to know where a company’s money comes from and where it goes. Types of Financial StatementRead more

Financial Reporting is a common practice in accounting where the financial statements of the company are disclosed to present its financial information and performance over a particular period. It is important to know where a company’s money comes from and where it goes.

Types of Financial Statements

There are 4 important types of financial statements such as:

- Income Statement: This statement summarises a company’s revenue, expenses and profits. It is prepared to calculate the net profit of the company.

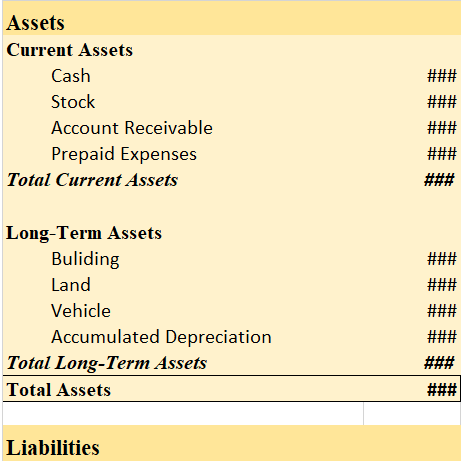

- Balance Sheet: It portrays the company’s assets and liabilities in a statement. This is used to understand the financial position of the company.

- Statement of Retained Earnings: This statement reveals a company’s changes in equity during an accounting period.

- Cash Flow Statement: It shows the amount of cash flowing in and out of the business. It is helpful in understanding the liquidity position of the business.

Importance of Financial Reporting

- Understanding these financial statements is helpful in making financial decisions. One can identify certain trends and hurdles while analyzing financial statements.

- It helps the top order management to keep a check on its outstanding debt and how to manage them effectively.

- Financial reports are also required to be prepared by law for tax purposes. Therefore these statements have to be prepared to calculate taxable income. It also ensures that the companies are compliant with the required laws and regulations.

- True and accurate financial reporting is also important for potential investors who need to understand the financial performance and position to come to a decision.

See less

The commercial banks are required to keep a certain amount of their deposits with the central bank and the percentage of deposits that the banks are required to keep as reserves is called Cash Reserve Ratio. The banks have to keep the amount to maintain the Cash Reserve Ratio with the RBI. CRR meansRead more

The commercial banks are required to keep a certain amount of their deposits with the central bank and the percentage of deposits that the banks are required to keep as reserves is called Cash Reserve Ratio.

The banks have to keep the amount to maintain the Cash Reserve Ratio with the RBI.

CRR means that commercial banks cannot lend money in the market or make investments or earn any interest on the amount below what is required to be kept in CRR.

RBI mandates Cash Reserve Ratio so that a percentage of the bank’s deposit is kept safe with the RBI, hence, in an uncertain event bank can still fulfill its obligation against its customers.

CRR also helps RBI to control liquidity in the economy. When CRR is kept at a higher rate, the lower the liquidity in the economy, and similarly when CRR is kept at a lower rate, there is higher liquidity in the economy.

The Reserve Bank of India also regulates inflation through the Cash Reserve Ratio:

The formula for CRR is-

Reserves maintained with Central Banks / Bank Deposits * 100%

For example:

The current CRR is 3% which means that for every Rs 100 deposit in the commercial banks have to keep Rs 3 as a deposit with RBI.

See less